Monday, September 15, 2014

House Prices in Austria

“Neither the non-financial corporate sector nor the household sector is overleveraged, but housing prices warrant monitoring,” according to the IMF’s annual economic report on Austria. The reports says that “Housing price increases have been strong in recent years but purchases have been to a large extent cash-financed and the strongest growth has been predominantly limited to Vienna and some tourist hotspots.”

“Neither the non-financial corporate sector nor the household sector is overleveraged, but housing prices warrant monitoring,” according to the IMF’s annual economic report on Austria. The reports says that “Housing price increases have been strong in recent years but purchases have been to a large extent cash-financed and the strongest growth has been predominantly limited to Vienna and some tourist hotspots.”

Posted by at 2:32 PM

Labels: Global Housing Watch

Wednesday, September 3, 2014

House Prices in Switzerland

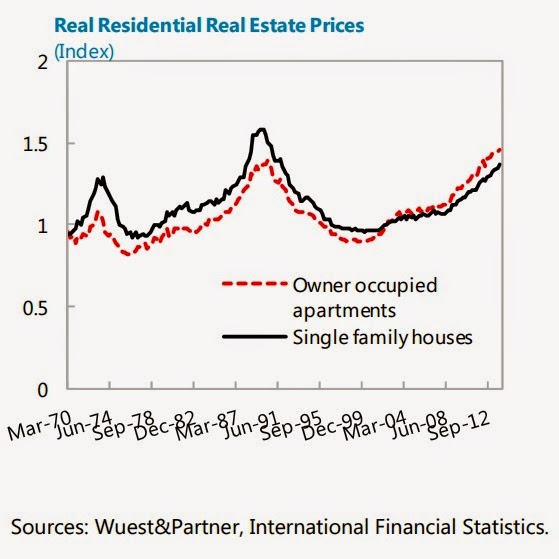

“Residential real estate prices have been on an upward trend since the late 1990s, and increases have been especially strong for owner occupied apartments. Through end-2013 prices for owner occupied apartments had increased by 77 percent in the last ten years, while prices for single family homes increased by 49 percent during the same period (…). Also in real terms have prices increased significantly. Compared to the CPI, owner occupied prices are at an all time high, almost 5 percent above the previous peak in the early 1990s before the sharp downward adjustment. Single family home prices are still about 14 percent below the peak, but above the peak in the 1970s and high in a historical perspective,” according to the IMF’s technical note on Switzerland.

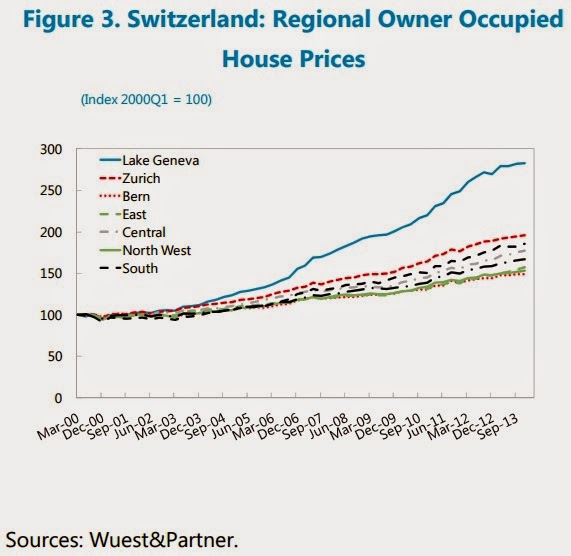

More specifically, the note says that “Real estate price increases have been more dramatic in some regions. In particular at Lake Geneva, where prices for owner occupied apartments during the last ten years had increased by 152 percent through the third quarter of 2013 (…). Single family homes prices had increased by 91 percent during the same period. The price increases also started from already high levels.”

In terms of valuation measures, the note says that “Comparing residential real estate prices to rents and income shows substantially increased ratios. Compared to rents, prices of owner occupied apartments have increased by about 25 percent in the last 10 years, which is significant (…). The ratio is nevertheless well below the historical high, though above the historical average. For single family home, the price to rent ratio is just above the long-run average. Turning to real estate prices compared to GDP per capita, the picture is fairly similar, and the ratio for owner occupied apartments prices is around 10 percent above the long-run average, while single family homes are a little below.”

“Residential real estate prices have been on an upward trend since the late 1990s, and increases have been especially strong for owner occupied apartments. Through end-2013 prices for owner occupied apartments had increased by 77 percent in the last ten years, while prices for single family homes increased by 49 percent during the same period (…). Also in real terms have prices increased significantly. Compared to the CPI, owner occupied prices are at an all time high,

Posted by at 5:20 PM

Labels: Global Housing Watch

Tuesday, September 2, 2014

House Prices in Czech Republic

“(…) while real estate prices are in a modest recovery trend,” says the IMF’s annual economic report on Czech Republic.

“(…) while real estate prices are in a modest recovery trend,” says the IMF’s annual economic report on Czech Republic.

Posted by at 8:19 PM

Labels: Global Housing Watch

House Prices in Slovak Republic

“Strong household credit growth reflects substantial home refinancing and some equity withdrawals. While borrowing can help support a recovery in domestic demand, competition among banks has made high LTVs more common (e.g., through higher LTV mortgages or topping up regular mortgages with housing loans). Although real estate prices remain subdued and household debt is not high, this practice could lead to overborrowing by consumers. Adoption of a regulation on LTV or debt-to-income ratios could help prevent an excessive build-up of risks for borrowers and banks,” according to latest IMF economic report on Slovak Republic.

“Strong household credit growth reflects substantial home refinancing and some equity withdrawals. While borrowing can help support a recovery in domestic demand, competition among banks has made high LTVs more common (e.g., through higher LTV mortgages or topping up regular mortgages with housing loans). Although real estate prices remain subdued and household debt is not high, this practice could lead to overborrowing by consumers. Adoption of a regulation on LTV or debt-to-income ratios could help prevent an excessive build-up of risks for borrowers and banks,”

Posted by at 8:11 PM

Labels: Global Housing Watch

Sunday, August 31, 2014

House Prices in Sweden

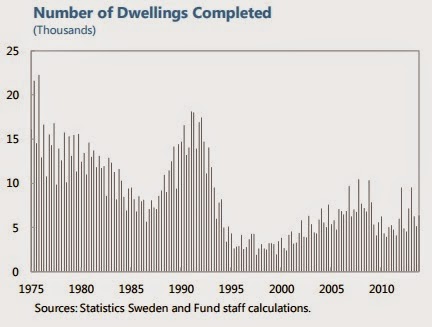

“A longer-term solution to rising house prices and mortgage levels will require alleviating housing supply constraints. Insufficient housing supply growth is a fundamental factor behind the rise in residential property prices, especially in metropolitan areas, where ongoing urbanization and immigration trends boost demand. This has resulted in higher housing prices, driving up the size of mortgages. While some steps have been taken, containing house price pressures will require a continuing effort to expand the stock of affordable housing and further reforms to zoning, permitting, and the rent-setting process. Public infrastructure investments, coordinated with municipalities, would also make private housing investments more attractive,” according to the IMF’s latest economic report on Sweden.

“A longer-term solution to rising house prices and mortgage levels will require alleviating housing supply constraints. Insufficient housing supply growth is a fundamental factor behind the rise in residential property prices, especially in metropolitan areas, where ongoing urbanization and immigration trends boost demand. This has resulted in higher housing prices, driving up the size of mortgages. While some steps have been taken, containing house price pressures will require a continuing effort to expand the stock of affordable housing and further reforms to zoning,

Posted by at 1:55 PM

Labels: Global Housing Watch

Subscribe to: Posts