Thursday, March 13, 2014

Lipton Releases IMF Paper on Fiscal Policy and Inequality

IMF First Deputy Managing Director David Lipton released a new paper on fiscal policy and inequality, adding to the stock of IMF work on this issue. Here are links and a cheat sheet to the key papers:

1) Painful Medicine: This (non-wonkish) paper documented that fiscal consolidations not only lower aggregate incomes but have distributional consequences—wage incomes fall more than profits; and the long-term unemployed are affected more than short-term unemployed.

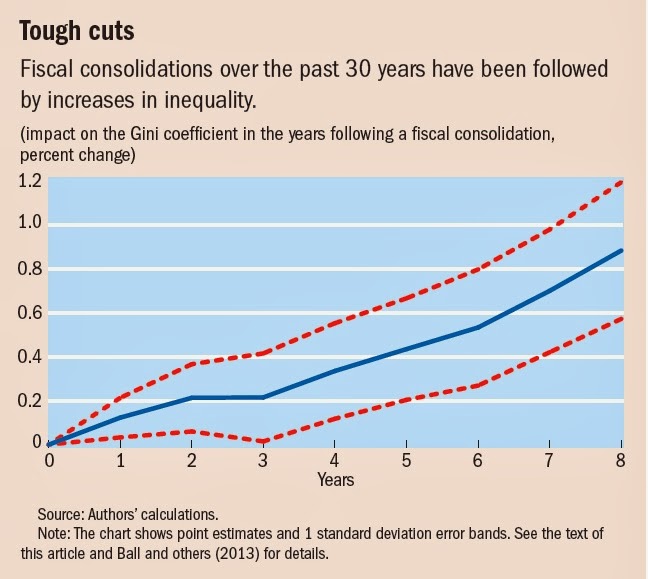

2) The Distributional Effects of Fiscal Consolidation: A wonkish version of the “Painful Medicine” article, with the additional result that, between 1978 and 2009, fiscal consolidations in advanced economies increased the Gini measure on income inequality.

3) Distributional Consequences of Fiscal Consolidation and the Role of Fiscal Policy: In addition to confirming the results in the previous papers, this paper brings in evidence from emerging markets. It also discusses how policies can be designed to mitigate the impacts of fiscal policy on inequality.

4) Who Let the Gini Out? A (non-wonkish) summary of some of the previous papers.

5) Fiscal Policy and Inequality: A key finding of the paper is that fiscal consolidations during the Great Recession did not lead to increases in inequality.

IMF First Deputy Managing Director David Lipton released a new paper on fiscal policy and inequality, adding to the stock of IMF work on this issue. Here are links and a cheat sheet to the key papers:

1) Painful Medicine: This (non-wonkish) paper documented that fiscal consolidations not only lower aggregate incomes but have distributional consequences—wage incomes fall more than profits; and the long-term unemployed are affected more than short-term unemployed.

Posted by at 5:49 PM

Labels: Inclusive Growth

Wednesday, March 12, 2014

House Prices in Belgium

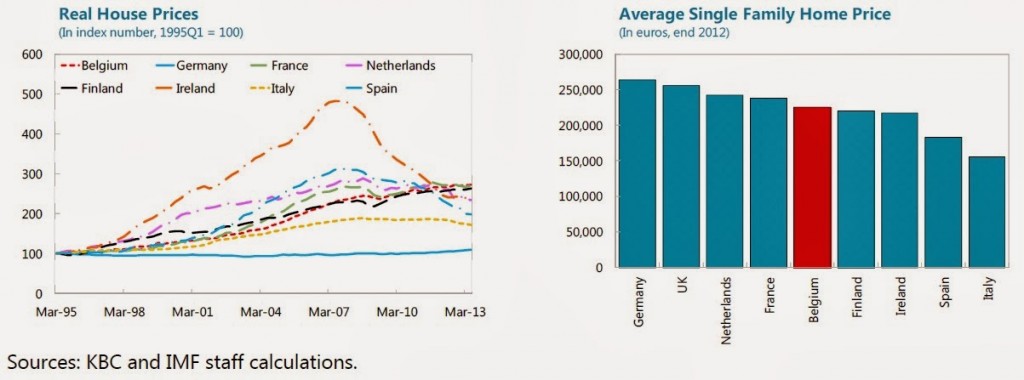

House prices are overvalued by “5–15 percent” according to a new IMF report on the Belgium economy. The report says that “Risks of a sharp correction of real estate prices appear contained. Property prices have risen by 110 percent in real terms since 2000, and, unlike in other EU countries, continued to increase through the financial crisis. Overvaluation estimates range from 10–60 percent, but valuation estimates based on price-to-income and price-to-rent ratios often miss catch-up effects. A finer assessment (interest-adjusted affordability regression analysis) suggests overvaluation of 5–15 percent. In fact, absolute prices remain moderate by European comparison. High ownership rates (around 70 percent), coupled with persistent housing shortages, are likely to prevent a rapid price decline. Robust household balance sheets, the prevalence of fixed interest rate mortgages, and the recent tightening of capital requirements on mortgage lending should limit the impact of an interest rate and/or unemployment shocks on the quality of the mortgage portfolio. However, the prevalence of fixed-rate mortgages shifts the interest rate risk to banks.”

House prices are overvalued by “5–15 percent” according to a new IMF report on the Belgium economy. The report says that “Risks of a sharp correction of real estate prices appear contained. Property prices have risen by 110 percent in real terms since 2000, and, unlike in other EU countries, continued to increase through the financial crisis. Overvaluation estimates range from 10–60 percent, but valuation estimates based on price-to-income and price-to-rent ratios often miss catch-up effects.

Posted by at 5:02 PM

Labels: Global Housing Watch

Wednesday, February 26, 2014

The IMF on Inequality: New Ostry-Berg Paper on Redistribution

A new paper by Andrew Berg and Jonathan Ostry (along with Haris Tsangarides) adds to the growing stock on IMF work on inequality.

In the recent past, the IMF has released papers on the impacts of fiscal tightening on inequality — see a summary here and to the research on which it is based here and here.

The IMF has also looked at the impact of capital account liberalization on inequality — see this article and Vox post.

The Berg-Ostry paper showed that inequality lowers the duration of growth spells. The new paper makes the case that redistribution efforts to lower inequality are not harmful to growth.

A new paper by Andrew Berg and Jonathan Ostry (along with Haris Tsangarides) adds to the growing stock on IMF work on inequality.

In the recent past, the IMF has released papers on the impacts of fiscal tightening on inequality — see a summary here and to the research on which it is based here and here.

The IMF has also looked at the impact of capital account liberalization on inequality —

Posted by at 4:04 PM

Labels: Inclusive Growth

Thursday, February 20, 2014

House Prices in Spain

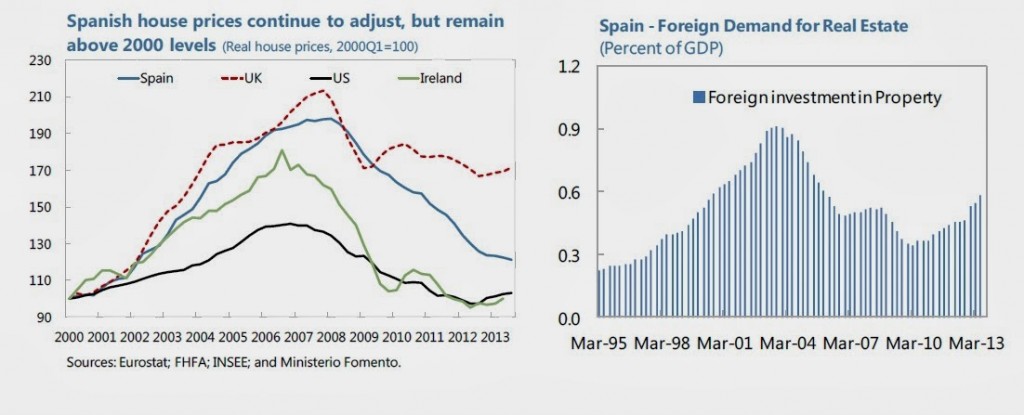

“Although house prices have started to stabilize in the most recent data, further declines are possible as the supply overhang is still large (the stock of vacant new houses equals four years of sales, and the population is falling). On the upside, foreign investor interest in Spanish property has increased noticeably in recent months,” according to a new report from the IMF.

Posted by at 8:25 PM

Labels: Global Housing Watch

Friday, February 14, 2014

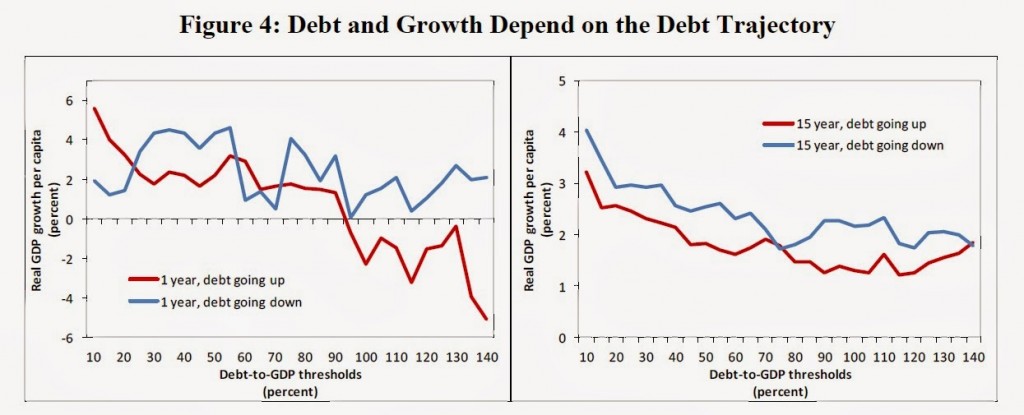

Does Debt Hurt Growth? Revisiting Reinhart and Rogoff

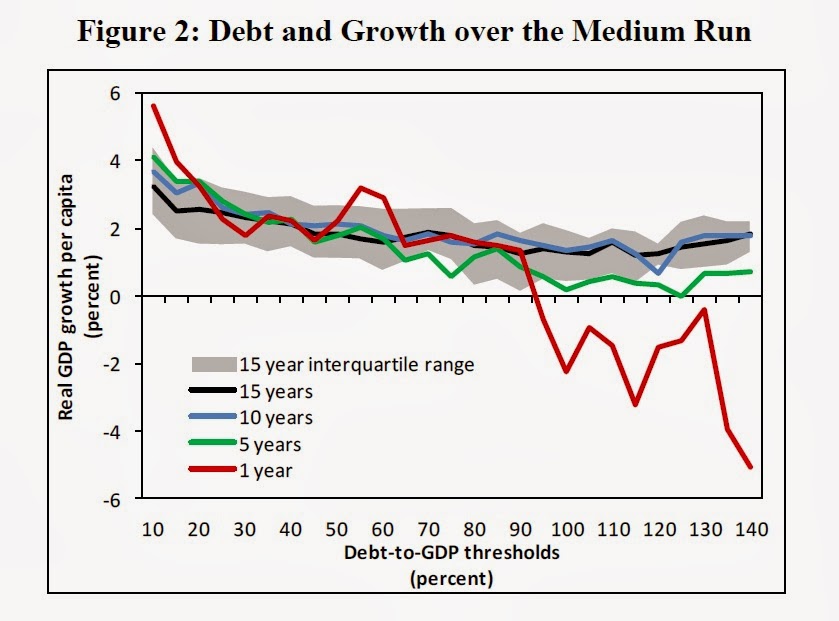

Is there a debt threshold that impairs medium term economic growth? The answer is no, according to a research paper by Andrea Pescatori, Damiano Sandri, and John Simon. They say that “Our analysis of historical data has highlighted that there is no simple threshold for debt ratios above which medium-term growth prospects are severely undermined. On the contrary, the association between debt and growth at high levels of debt becomes rather weak when one focuses on any but the shortest-term relationship, especially when controlling for the average growth performance of country peers. Furthermore, we find evidence that the relation between the level of debt and growth is importantly influenced by the trajectory of debt: countries with high but declining levels of debt have historically grown just as fast as their peers. The fact that there is no clear debt threshold that severely impairs medium term growth should not, however, be interpreted as a conclusion that debt does not matter. For example, we have found some evidence that higher debt appears to be associated with more volatile growth. And volatile growth can still be damaging to economic welfare.

As in previous empirical studies, our analysis is still subject to potential endogeneity concerns that should caution against drawing strong policy implications. However, by mitigating the short-term and mechanical reverse causality problems whereby low growth leads to higher debt, we show that the prima facie case for debt thresholds is substantially weakened. We find no evidence of threshold effects over any but the shortest-term horizons. Furthermore, the remaining relationship between debt and growth is relatively muted and the magnitude is much smaller than the dramatic figures suggested in earlier studies. Notwithstanding this, because of residual issues that confound the interpretation of the medium-term relationship between debt and growth, we emphasize that this does not establish what the underlying structural relationship is. That must wait for more sophisticated work that can properly address the complex identification issues that characterized this area of research.”

Is there a debt threshold that impairs medium term economic growth? The answer is no, according to a research paper by Andrea Pescatori, Damiano Sandri, and John Simon. They say that “Our analysis of historical data has highlighted that there is no simple threshold for debt ratios above which medium-term growth prospects are severely undermined. On the contrary, the association between debt and growth at high levels of debt becomes rather weak when one focuses on any but the shortest-term relationship,

Posted by at 10:31 PM

Labels: Inclusive Growth

Subscribe to: Posts