Friday, March 30, 2012

Seven Questions: Unemployment through the Prism of the Great Recession

The Great Recession of 2007–09 led to a worldwide increase of 30 million in the number of people unemployed, with about half of that increase among advanced countries. This article discusses the factors behind this rise in unemployment, the reasons why countries such as Germany experienced little increase in unemployment while others were hit hard, whether policies were able to stave off an even worse outcome, and what the prospects are for labor markets in advanced countries. Here is a link to the full article.

The Great Recession of 2007–09 led to a worldwide increase of 30 million in the number of people unemployed, with about half of that increase among advanced countries. This article discusses the factors behind this rise in unemployment, the reasons why countries such as Germany experienced little increase in unemployment while others were hit hard, whether policies were able to stave off an even worse outcome, and what the prospects are for labor markets in advanced countries.

Posted by at 1:31 PM

Labels: Inclusive Growth

Wednesday, March 7, 2012

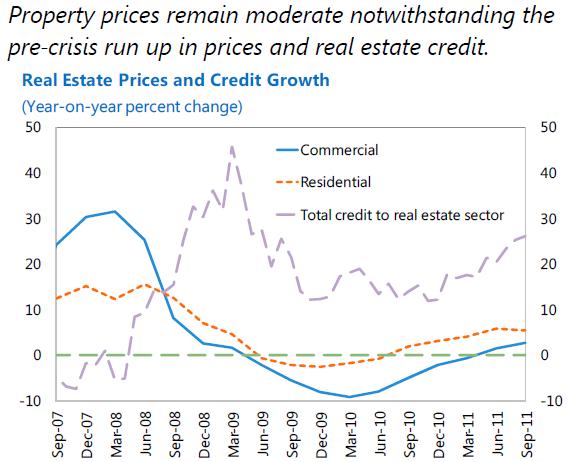

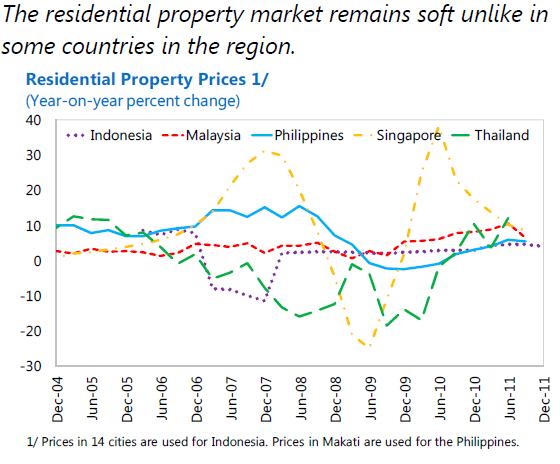

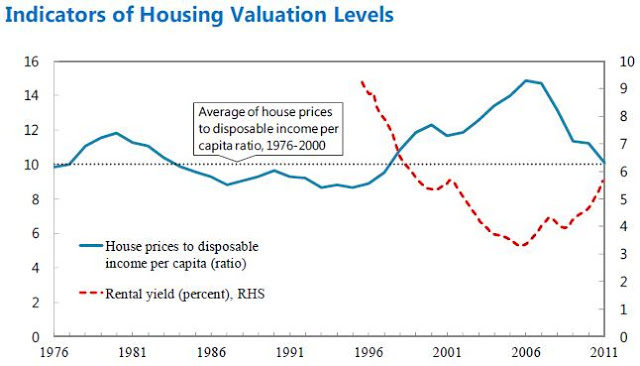

House Prices in Philippines

Posted by at 9:27 PM

Labels: Global Housing Watch

Friday, March 2, 2012

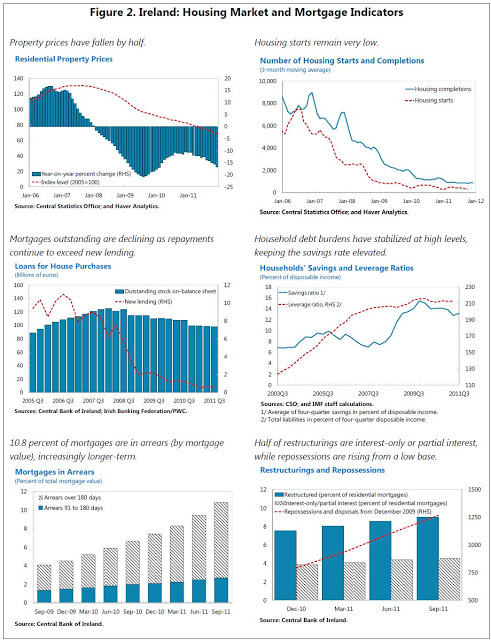

House Prices in Ireland

The IMF report notes:

“House price declines accelerated in the second half of 2011, while mortgage arrears continued to rise (Figure 2). Nonetheless the rate of decline in house prices at 13.2 percent y/y in 2011, remained within the stress scenario for the bank recapitalization, which allowed for a house price decline of 17.4 percent in 2011, and a further fall of 18.8 percent in 2012. With house prices down 47.4 percent from their peak in 2007, indicators of house valuation are returning to historical norms. The value share of owner-occupied residential mortgages in arrears rose to 10.8 percent in Q3 2011. About 10.7 percent of this loan book value has undergone restructuring, mostly reducing payments to interest-only, but about half of the restructured loans are still in arrears.”

The IMF report notes:

“House price declines accelerated in the second half of 2011, while mortgage arrears continued to rise (Figure 2). Nonetheless the rate of decline in house prices at 13.2 percent y/y in 2011, remained within the stress scenario for the bank recapitalization, which allowed for a house price decline of 17.4 percent in 2011, and a further fall of 18.8 percent in 2012. With house prices down 47.4 percent from their peak in 2007,

Posted by at 5:58 PM

Labels: Global Housing Watch

Wednesday, February 29, 2012

Fred Bergsten: will the euro survive?

Fred Bergsten is the founder of the world’s most influential think tank on international economics, the Peterson Institute. Fred recently announced that he would be stepping down as the Institute’s director. My interview with him covers Fred’s views on whether the euro will survive, but other topics as well—his proposal for a G-2 (a tacit economic club of the U.S. and China to go alongside the G-20), his early work predicting the rise and success of OPEC, and his Cold War with Henry Kissinger. Not many people would have the courage, as Fred did at the age of 30, to quit working for Kissinger telling him: “Henry, you do not seem to need—or deserve—the quality of the advice I am giving you.”

|

| Photo: Michael Spilotro/IMF |

Bergsten on the Euro crisis

The adoption of the euro was a singular event in world monetary history. But most U.S. economists have been skeptical of the euro’s success. Two U.S. economists have bucked the trend: Robert Mundell and Fred Bergsten. Has the euro crisis led Bergsten to change his mind about the euro’s successt?

BERGSTEN: Mundell actually waxed and waned. Sometimes he’s a fixed rate guy. Sometimes he’s a floating rate guy. Anyway, maybe with him as the other exception, I was about the only other American economist that really supported the euro right from the start.

The difference was methodological. The other American economists, including Mundell, based their views on optimal currency areas. They all concluded that Europe was not an optimal currency area and, therefore, the euro was a bad idea.

I came at it with a totally different perspective. This was a political economy perspective. In my jobs in government, but also from outside, I had been actually quite close to the European integration exercise really from the start. And what deeply impressed me was that every time Europe had a crisis, they not only overcame it, they came out stronger. As Monnet said impressively way back at the start, “Europe will be built by crises and it will move forward through crises, but it will always move forward.” And so far he’s been proven right.

And so when you get into this crisis, my mantra is “Watch what they do, not what they say.” And at every stage of this crisis, they have done enough to avoid a collapse — not enough to sway the market, but mind you that’s because they can’t say to the markets what they are going to do, because then that would take all the pressure off the other countries and it would be a moral hazard.

So they’re playing a risky game, but again, based on this political kind of motive, I say very strongly Germany will pay whatever it has to pay, both because of that continuing geo-strategic imperative, but also now because the euro is so hugely important to Germany’s economy. The ECB will discount to whatever extent it has to to avoid a collapse even though they can’t say that they’ll do it and, therefore, can’t give the markets the assurance they want.

So I’m actually quite confident still, despite all the rumor mills, that the euro will survive. There will be no widespread defaults. The Greeks might have to, but you might say they’ve already defaulted a lot.

And, even more importantly I’m convinced Europe will come out of it stronger When they created the so-called economic and monetary union they were pretty complete with the monetary union, but there was no economic union. So it was a half-way house, it had to be reconciled sometime. Either you had to forget about the euro or you had to create an economic union. And I’m convinced they will never, never, never let the euro just fail.

Therefore, they have to create an economic union, and I’m convinced that all the steps that they’re taking now — the EFSF, the successor mechanism, the economic governing systems they’re setting up, Merkel’s calls for a political union — I think all that’s leading toward a full economic union. And five years from now — I think it will take years and it it’ll take key Constitutional amendments — they’ll have it.

|

| Photo: Michael Spilotro/IMF |

**

Read the full interview here. The interview was conducted on December 22, 2011 for a profile of Fred that just appeared in the IMF’s magazine Finance & Development.

Fred Bergsten is the founder of the world’s most influential think tank on international economics, the Peterson Institute. Fred recently announced that he would be stepping down as the Institute’s director. My interview with him covers Fred’s views on whether the euro will survive, but other topics as well—his proposal for a G-2 (a tacit economic club of the U.S. and China to go alongside the G-20), his early work predicting the rise and success of OPEC,

Posted by at 5:57 PM

Labels: Profiles of Economists

Monday, February 13, 2012

BP’s Cheerful Energy Outlook for 2030

BP has a surprisingly cheerful energy outlook for 2030.

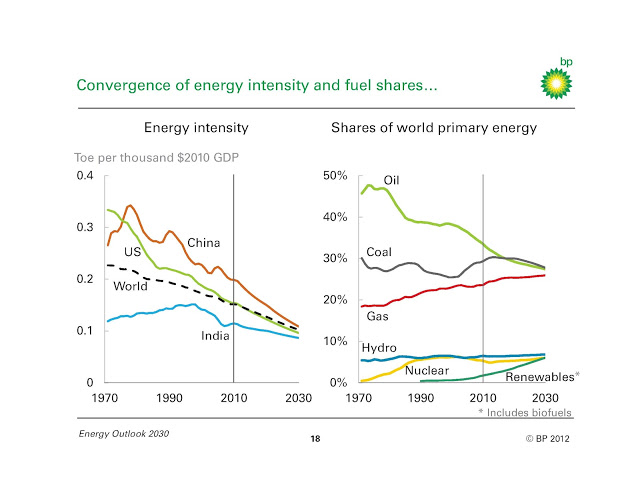

Energy intensity—the amount of energy it takes to produce a dollar of income—has been continuing a steady downward march for 40 years, and BP expects this to continue. By 2030, the major regions of the world—the U.S., China and India—will have the same energy intensity. Energy use will be diversified across sources: oil, coal, and gas will each have a 30% market share, with hydro, nuclear and renewables accounting for the remaining 10%.

Energy supply from the Americas—US and Brazilian biofuels, Canadian oil sands, Brazilian deepwater and US shale oil—will help in balancing supply and demand in 2030.

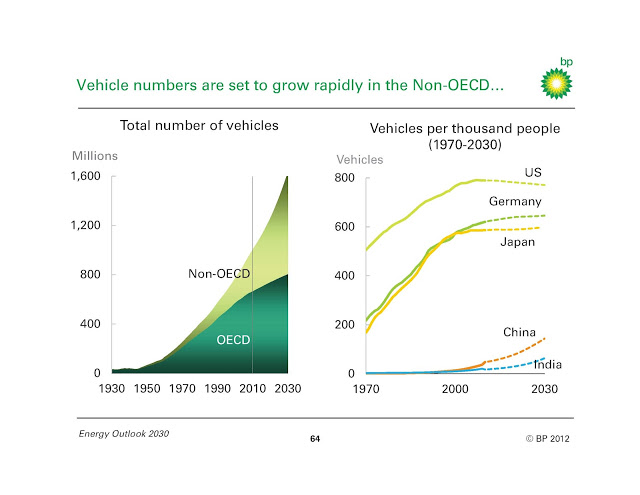

Vehicle ownership (per person) will hit saturation in the rich nations. And while it will grow in China and India, it will follow a slower path than seen historically in other countries.

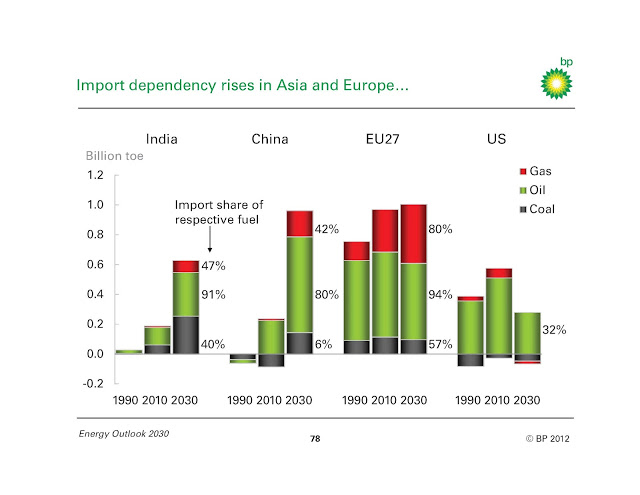

If we could keep politics out of the picture, we could have an energy outlook by 2030 in which the America are largely energy self-sufficient, the FSU supplies nearby Europe, and the Mid-East and Africa take care of the needs of the Asia-Pacific.

Import dependence in 2030 is projected to be higher than it is today for all major energy importers—Europe, China and India—but will decline for the United States. BP predicts that by 2030 “the import share of oil demand and the volume of oil imports in the US will fall below the 1990s levels, largely due to rising domestic shale oil production and ethanol displacing crude imports. The US will also become a net exporter of natural gas.”

BP has a surprisingly cheerful energy outlook for 2030.

Energy intensity—the amount of energy it takes to produce a dollar of income—has been continuing a steady downward march for 40 years, and BP expects this to continue. By 2030, the major regions of the world—the U.S., China and India—will have the same energy intensity. Energy use will be diversified across sources: oil, coal, and gas will each have a 30% market share,

Posted by at 1:33 AM

Labels: Energy & Climate Change

Subscribe to: Posts