Wednesday, October 10, 2012

The global impact of the ‘food supply crunch’

From the FT:

Which countries will be worst affected by the sharp rise in global grains prices?

The International Monetary Fund, which has an interest in the question because it is usually a source of loans for countries that have run out of money, has studied the vulnerability of different regions to the jump in food prices due to the US drought.

In one section of its World Economic Outlook published on Monday, the fund analyses the effects of the “food supply crunch”.

While commodities traders – who are awaiting the US Department of Agriculture’s monthly forecasts on Thursday – may have already moved on from the US drought, higher prices are still a reality for consumers of wheat, corn and soyabeans. Despite a recent correction, prices for the three staples are still up 20-40 per cent year on year.

The IMF breaks down the issue into three sub-questions: which countries have low food inventories; which countries are most dependent on the global markets for their food supply; and which countries’ populations spend the largest proportion of their income on food.

The countries and regions at the most vulnerable end of the range for each of the categories are the most likely to suffer problems, the fund explains.

While China is a large importer of some foodstuffs (especially oilseeds), it would be able to withstand higher prices better than others because of its large stockpiles. At the other end of the scale, inventories of food commodities in the US have fallen well below historical norms, but food is a relatively small proportion of US consumer expenditure, therefore the country is less exposed.

It may not come as a complete surprise to learn which countries are most at risk. They are: the Caribbean and Central America, which are heavily reliant on corn imports and whose stocks are lower than during the 2007-08 food crisis; the Middle East and sub-Saharan Africa, which have relatively high import reliance and low inventories of wheat; and north Africa, where food accounts for about 40 per cent of final consumption.

Indeed, Morocco, which is forecast to import a record 4.5m tonnes of wheat this year, has already sought a $6.2bn precautionary loan from the IMF.

But the IMF says that the current situation is less severe than in 2007-08 as rice prices remain subdued, oil prices are not so high, and so far, there have not been widespread export restrictions.

Nonetheless, the fund concludes: “Countries should expect rising inflation and balance of payments pressures.”

From the FT:

Which countries will be worst affected by the sharp rise in global grains prices?

The International Monetary Fund, which has an interest in the question because it is usually a source of loans for countries that have run out of money, has studied the vulnerability of different regions to the jump in food prices due to the US drought.

In one section of its World Economic Outlook published on Monday,

Posted by at 10:09 AM

Labels: Energy & Climate Change

State of Global Labor Markets

My regular look at the global employment picture is available here.

My regular look at the global employment picture is available here.

Posted by at 1:32 AM

Labels: Inclusive Growth

IMF’s latest commodity outlook

The IMF just released this commodity markets review as part of its World Economic Outlook. The review provides the outlook for energy, metals and food markets.

It also discusses:

- the tight link between commodity prices and global demand;

- impact of Chinese growth on base metals;

- the supply-demand balance in oil markets;

- the vulnerabilities of countries to food price shocks.

We hope you find the review useful. The review is a public document and can be cited without prior permission. Questions and comments can be sent to rescommodities@imf.org

The IMF just released this commodity markets review as part of its World Economic Outlook. The review provides the outlook for energy, metals and food markets.

It also discusses:

- the tight link between commodity prices and global demand;

- impact of Chinese growth on base metals;

- the supply-demand balance in oil markets;

- the vulnerabilities of countries to food price shocks.

We hope you find the review useful.

Posted by at 1:24 AM

Labels: Energy & Climate Change

Tuesday, October 2, 2012

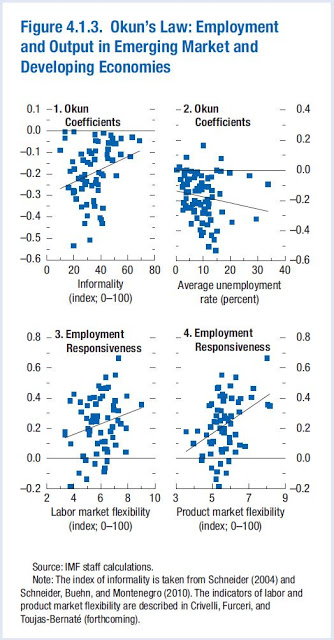

Jobs and Growth: Can’t Have One Without the Other?

Emerging market and developing economies have enjoyed robust growth during the past decade and bounced back quickly from the Great Recession, in marked contrast to the more tepid recovery—and even renewed recession—in advanced economies. Similarly, although unemployment in emerging market and developing economies did go up during the Great Recession, by 2011 it was essentially back to precrisis levels.Is the observed correspondence between jobs and growth a surprise, or does it represent a systemic feature of emerging market and developing economies? In a joint work with Davide Furceri, we show that the short-term relationship between labor market developments and output growth has been fairly strong in many of these economies for the past 30 years. This is particularly the case in many emerging markets. Hence, although the emphasis on structural policies to lower long term unemployment and raise labor force participation remains appropriate, cyclical developments deserve adequate consideration as well. The short term relationship between jobs and growth suggests that macroeconomic policies to maintain aggregate demand also likely play an important role in labor market outcomes in many of these economies.

Preliminary work on Okun’s Law in advanced economies is available here.

Emerging market and developing economies have enjoyed robust growth during the past decade and bounced back quickly from the Great Recession, in marked contrast to the more tepid recovery—and even renewed recession—in advanced economies. Similarly, although unemployment in emerging market and developing economies did go up during the Great Recession, by 2011 it was essentially back to precrisis levels.Is the observed correspondence between jobs and growth a surprise, or does it represent a systemic feature of emerging market and developing economies?

Posted by at 6:04 PM

Labels: Inclusive Growth

Friday, September 21, 2012

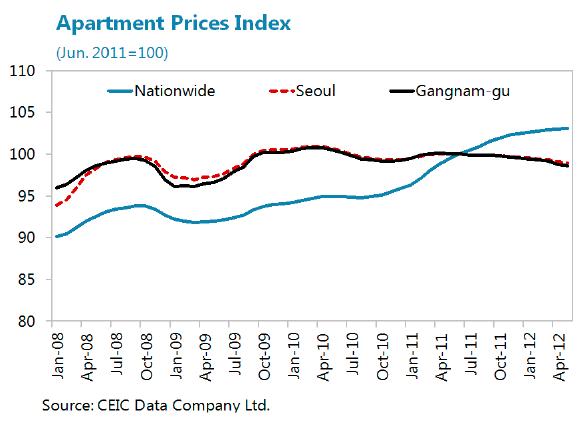

House Prices in Korea

“Housing prices have peaked in Seoul but are rising in the rest of Korea,” according to a new report from the IMF. The report says that “following a protracted period of rising prices, housing prices in Seoul have remained weak due to a still large, albeit declining, inventory of unsold homes and limited expectation of price appreciation. The steady rise in housing prices outside Seoul (which have moderated recently) has been supported by contracting supply, a rapid increase in rents, and a rise in demand supported by strong non-bank lending. In response to the weakness in the Seoul housing market, the authorities have relaxed regulations in May 2012, including by raising loan-to-value (LTV) and debt-to-income (DTI) ratios applied to some high-house price districts.”

“Housing prices have peaked in Seoul but are rising in the rest of Korea,” according to a new report from the IMF. The report says that “following a protracted period of rising prices, housing prices in Seoul have remained weak due to a still large, albeit declining, inventory of unsold homes and limited expectation of price appreciation. The steady rise in housing prices outside Seoul (which have moderated recently) has been supported by contracting supply, a rapid increase in rents, and a rise in demand supported by strong non-bank lending.

Posted by at 1:46 PM

Labels: Global Housing Watch

Subscribe to: Posts