Wednesday, February 1, 2012

Do Groundhogs make Better Forecasters than Economists?

Feb. 2 is Groundhog Day. Legend has it that if the groundhog—Punxsutawney Phil—casts a shadow that day, six weeks of winter lie ahead. No shadow and the forecast is for an early spring. Statistical records suggest the groundhog has been right about 40% of the time. Are we headed for economic spring or winter? If past performance is any guide, we might be better off asking groundhogs than economists.

A dismal record

In 2000, I wrote in the Financial Times that “the record of failure to predict recessions is virtually unblemished.” A dozen years and many recessions later, there is little reason to change my assessment.

My initial conclusion was based on my findings that only two of the 60 recessions that occurred around the world during the 1990s were predicted by private sector forecasters a year in advance. About 40 of the 60 recessions remained undetected seven months before they occurred. As even as late as two months before each recession began, about a quarter of the forecasts still predicted positive growth for the country concerned.

With my colleagues Jair Rodriguez and Hites Ahir, I’ve since looked at the record of forecasting recessions over the decade of the 2000s and during the Great Recession of 2007-09.

Let’s consider the 2000s first and restrict attention to forecasts for twelve large economies—the G7 plus the ‘E7’ (emerging market economies–Brazil, China, India, Korea, Mexico, Russia and Turkey), which together account for over three-quarters of world GDP.

There were a total of 26 recessions in this set of countries. Only two recessions were predicted a year in advance and one of those predictions came toward the turn of the year. Requiring recessions to be predicted a year ahead may seem like an unreasonably high bar to set.

Lowering the bar to the start of the year in which the recession occurred does indeed improve the performance somewhat: 8 of the 26 recessions were predicted in February of the year in which they occurred and 16 were predicted by August. But even as the year drew to a close, 6 of 26 recessions remained undetected by forecasters.

Moreover, while forecasters increasingly started to recognize recessions in the year in which they occurred, the magnitude of the recession was underpredicted in the vast majority of cases. For instance, even as late as December of the year of the recession, the forecast was more optimistic than the outcome in 15 cases.

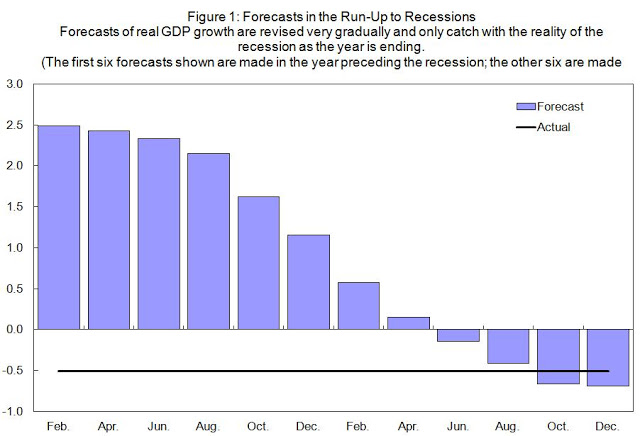

Figure 1 shows the evolution of forecasts on average across the 26 episodes. The forecast in February of the year before was for about 2.5% growth. This forecast was slowly lowered over the course of the year and by the start of the year of the recession the average forecast was for a small decline in real GDP. It was only as the year was drawing to a close that the average forecast caught up with the reality of the recession.

The impression one gets is of forecasts chasing the data rather than staying a step ahead of it.

The forecasting performance at the onset of the Great Recession was no better. Looking at forecasts for over 80 countries, it turns out that none of the nine recessions that started in 2008 was predicted a year in advance. Even by April 2008, none of the nine recessions were predicted and by October 2008, only four were.

Official sector forecasts?

If private sector growth forecasts are of little use in spotting recessions, why not use the forecasts made by the official sector? The IMF, the World Bank and the OECD all provide economic forecasts for free.

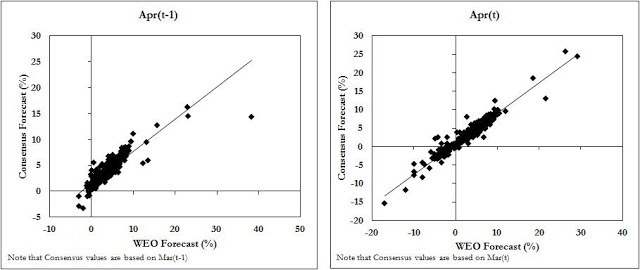

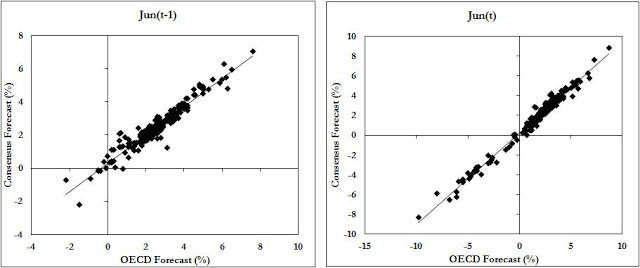

Yet there is not much to choose between private sector and official sector forecasts. Statistical “horse races” between the two tend to end up in a photo-finish in most cases. As just one example of this, look at Figure 2 above which compares private sector (consensus) forecasts vs. the IMF’s World Economic Outlook and the OECD’s forecasts. It is evident from these charts that there is little daylight between private sector forecasts and official sector forecasts: the forecasts have a correlation of over 0.9.

This finding casts new light on claims sometimes made that the growth projections of international organizations tend to be over-optimistic. Since the private sector is not subject to the same pressures, it is puzzling that its forecasts end up so close to those of international organizations. At the same time, the pressures acting on private forecasters to lead them towards over-optimism are not faced by forecasters in international organizations.

One possible explanation for the similarity of the predictions is that private and official sector forecasters feed on each other and—in many countries—are heavily reliant on government forecasts. Exuberance on the part of governments may affect both private sector forecasts and those of international organizations.

Buyer beware

The failure to predict recessions does not mean that forecasts of economic growth have no value. But it does suggest that users of forecasts might be better served by paying greater attention to the description of the outlook and the associated risks than to just the central forecast itself.

Reassuringly, it is becoming more common to show how much uncertainty there is about whether the central forecast will come true. It is particularly useful to be explicit about the downside risks to a growth forecast as it can provide a wake-up call for policies and actions needed to keep those risks from materializing.

Feb. 2 is Groundhog Day. Legend has it that if the groundhog—Punxsutawney Phil—casts a shadow that day, six weeks of winter lie ahead. No shadow and the forecast is for an early spring. Statistical records suggest the groundhog has been right about 40% of the time. Are we headed for economic spring or winter? If past performance is any guide, we might be better off asking groundhogs than economists.

A dismal record

Posted by at 8:03 PM

Labels: Forecasting Forum

Subscribe to: Posts