Monday, September 12, 2011

Whom Will it Hurt? The Short-Run Impacts of Fiscal Consolidation

WHEN British Prime Minister David Cameron announced his government’s deficit reduction plans earlier this year he said, “Those who argue that dealing with our deficit and promoting growth are somehow alternatives are wrong. You cannot put off the first in order to promote the second” (Cameron, 2011).

The challenge facing the United Kingdom and many advanced economies is how to bring debt down to safer levels in the face of a weak recovery. Will deficit reduction lead to stronger growth and job creation in the short run?

Recent IMF research provides an answer to this question. Evidence from data over the past 30 years shows that consolidation lowers incomes in the short term, with wage-earners taking more of a hit than others; it also raises unemployment, particularly long-term unemployment.

For the advanced economies, there is an unmistakable need to restore fiscal sustainability through credible consolidation plans. At the same time, we know that slamming on the brakes too quickly will hurt the recovery and worsen job prospects. Hence the potential longer-run benefits of fiscal consolidation must be balanced against the short- and medium-run adverse impacts on growth and jobs.

Read full article on the IMF website.

WHEN British Prime Minister David Cameron announced his government’s deficit reduction plans earlier this year he said, “Those who argue that dealing with our deficit and promoting growth are somehow alternatives are wrong. You cannot put off the first in order to promote the second” (Cameron, 2011).

The challenge facing the United Kingdom and many advanced economies is how to bring debt down to safer levels in the face of a weak recovery.

Posted by at 10:42 PM

Labels: Inclusive Growth

Monday, September 5, 2011

Roubini ups his recession probability from 40% to 60%

The 40% prediction was made in a talk at the IMF in September 2010. Below is what he said a few days ago for the current scenario and few years back:

September 2006 (IMF)

“my view is that the risk of a hard landing is very high for the U.S. economy. I see essentially a recession coming by next year. I give it a very high likelihood. I argue that housing today, like the tech bust in 2000-2001 will have a macro effect; it is not going to be just a sectoral effect. I argue that U.S. consumers are now close to a ‘tipping over’ point given all the vulnerabilities I have discussed. I argue that the Fed easing will occur, so the next move is going to be a cut, but it is not going to prevent a recession. And, finally, I argue that the rest of the world is not going to be able to decouple from the U.S. even if it is not going to experience an outright recession like the United States. So on that cheerful note, I will stop.”

The 40% prediction was made in a talk at the IMF in September 2010. Below is what he said a few days ago for the current scenario and few years back:

August 2011 (Portfolio.com)

“We’ve reached a stall speed in the economy, not just in the U.S., but in the euro zone and the UK. We see probably a 60 percent probability of recession next year, Read the full article…

Posted by at 1:48 AM

Labels: Profiles of Economists

Tuesday, August 2, 2011

Presentation video on “Long-Term Unemployment- Causes, Costs, Cures”

See my presentation video on where do the industrialized nations stand in regard to the effect of long-term unemployment after the Great Recession of 2009-2011? And trends related to the effects of long-term unemployment on western industrialized nations.

See my presentation video on where do the industrialized nations stand in regard to the effect of long-term unemployment after the Great Recession of 2009-2011? And trends related to the effects of long-term unemployment on western industrialized nations.

Posted by at 4:03 PM

Labels: Inclusive Growth

Friday, July 15, 2011

How do Countries Rank in Energy Security?

My presentation at EMEE ranked countries’ energy security based on how diversified they were in the sources of their energy supplies.

My presentation at EMEE ranked countries’ energy security based on how diversified they were in the sources of their energy supplies.

Posted by at 6:17 PM

Labels: Energy & Climate Change

Tuesday, July 12, 2011

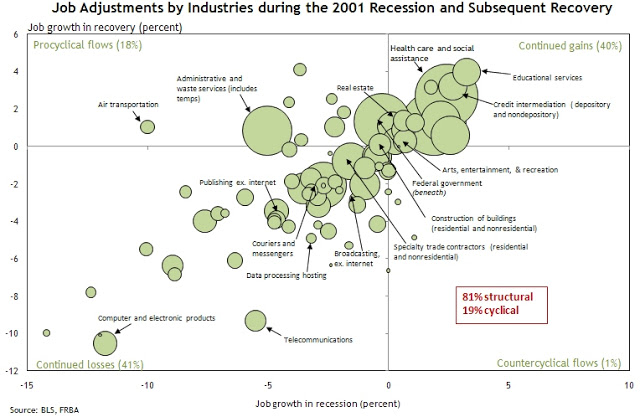

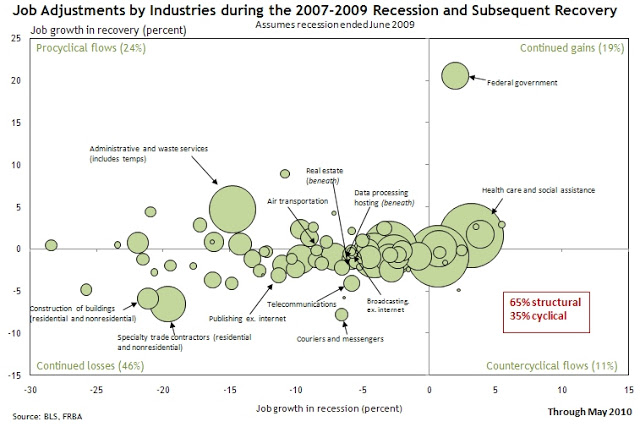

More on Structural Unemployment: Manufacturers Struggling to Find Skilled Workers

At the Joint Economic Committee (JEC) hearing, Georgetown University public policy professor Harry Holzer said that “the ratio of job vacancies to new hires in manufacturing is higher than we find in any other major industry group, suggesting that employers are having some difficulty filling their newly created jobs (…) On its own, our system of higher education will not produce enough skills needed by American workers to prosper. Our education and work force systems largely operate in isolation from one another.” Indeed, BTE Technologies President Chuck Wetherington concurred with Holzer who said that “my job is getting a bit more technical. There are some micro and macroeconomic issues. Occasionally we have to recruit from abroad. There is a mismatch between skills and workers.” See the full article on the New York Times website. Also, a webcast of the hearing is available at the Joint Economic Committee site.

At the Joint Economic Committee (JEC) hearing, Georgetown University public policy professor Harry Holzer said that “the ratio of job vacancies to new hires in manufacturing is higher than we find in any other major industry group, suggesting that employers are having some difficulty filling their newly created jobs (…) On its own, our system of higher education will not produce enough skills needed by American workers to prosper. Our education and work force systems largely operate in isolation from one another.” Indeed,

Posted by at 11:22 PM

Labels: Inclusive Growth

Subscribe to: Posts