Wednesday, August 21, 2019

Attempting to Avoid a Recession: Fortune or Folly?

An intriguing analysis by the SEI Knowledge Center on forecasting recessions:

“To explore this possibility, we looked at the last 13 recessions in the US dating back to 1937. US data was used due to availability of a longer history; we believe the core conclusions of the analysis should be the same for any geography or market. We considered a range of sell-and-buy scenarios surrounding the official start and end dates of each recession, as determined by the National Bureau of Economic Research (or NBER, a private, non-profit, non-partisan organisation). The timing of our hypothetical decisions to sell out of the market and buy back into the market varied by up to eight quarters before and after each actual recession start and end date. This gave us a grand total of 2,577 scenarios to consider, as highlighted in Exhibit 1.”

Exhibit 1: Endless Possibilities

Source: Bloomberg, SEI

An intriguing analysis by the SEI Knowledge Center on forecasting recessions:

“To explore this possibility, we looked at the last 13 recessions in the US dating back to 1937. US data was used due to availability of a longer history; we believe the core conclusions of the analysis should be the same for any geography or market. We considered a range of sell-and-buy scenarios surrounding the official start and end dates of each recession,

Posted by at 12:29 PM

Labels: Forecasting Forum

Tuesday, August 20, 2019

Housing markets and inequality

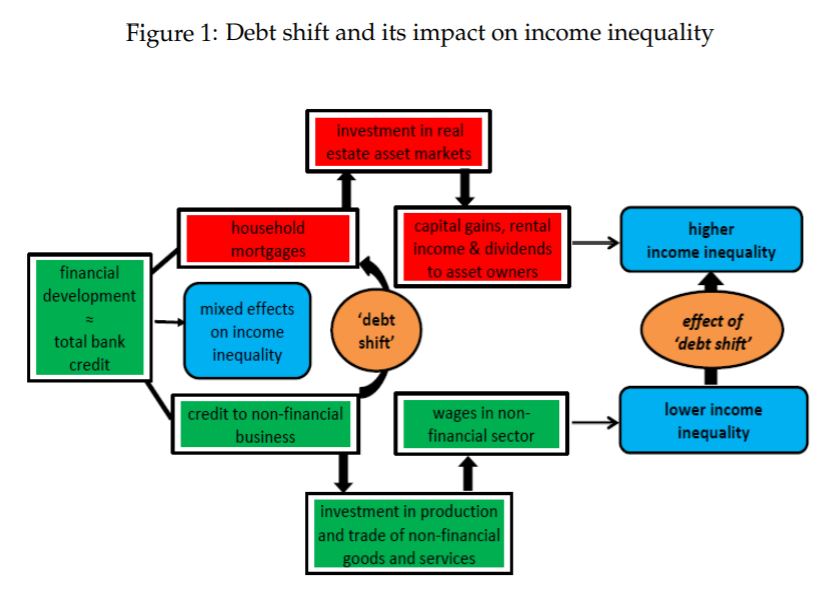

From a working paper by Dirk Bezemer and Anna Samarina:

“These results suggest that ‘debt shift’ may be one of the factors explaining recent

trends in income inequality. Credit to real estate asset markets results in rising capital

gains and growth of incomes connected to the real estate sector. Since these incomes

are concentrated among rich households, this widens income disparities. In support,

we find that mortgage credit increases the income share of households in the top 10%

of the income distribution.”Continue reading here.

From a working paper by Dirk Bezemer and Anna Samarina:

“These results suggest that ‘debt shift’ may be one of the factors explaining recent

trends in income inequality. Credit to real estate asset markets results in rising capital

gains and growth of incomes connected to the real estate sector. Since these incomes

are concentrated among rich households, this widens income disparities. In support,

we find that mortgage credit increases the income share of households in the top 10%

of the income distribution.”

Posted by at 8:13 AM

Labels: Global Housing Watch

Lessons in economics from Algeria’s victory in the Africa Cup of Nations

From a VoxEU post by Rabah Arezki:

“Algeria’s recent victory in the Africa Cup of Nations has united a country whose development model has frustrated its young and educated workforce. This column offers four lessons for economic development from the national football team’s success: on the role of competition and market forces, mobilising talent, the role of managers, and the importance of referees (i.e. regulation).

On 19 July, Algeria won the 2019 edition of the Africa Cup of Nations. The victory was the culmination of a strongly contested international football tournament with 24 teams where we saw the best of competition, talent, and refereeing on the continent. Algeria’s consecration comes amid sweeping political transformation triggered by massive demonstrations in the past few months, in turn driven by youths asking for radical change. This has united Algerians and emboldened the national team. This can-do spirit and renewed momentum are likely to be key ingredients for delivering big reforms.

On the economic front, Algeria’s development model has frustrated an educated young and increasingly female labour force aspiring to economic empowerment beyond subsidies and public jobs. The model is essentially stuck in the transition from an administrated economy to a market economy. Moreover, decades of state domination with episodes of liberalisation have yielded crony capitalism, further distancing the population from appreciating the power of harnessing markets for development.

In Algeria, as in many countries, football has triggered passions capturing dreams of greatness and unifying nations. Football can offer four lessons for economic development in Algeria, which is looking to revamp its economic model (see also Kuper and Szymanski 2009 and Palacios-Huerta 2014).

The first lesson is on the role of competition and the power of market forces. In too many sectors in Algeria, prices are controlled and state or private monopolies are the rule, stifling the space for talented Algerians to transform their economy and deterring foreign investment. This is unsustainable considering the shrinking rents coming from oil and gas ever since oil prices collapsed in 2014. Football illustrates how market mechanisms are an important filter for detecting and rewarding talent based on performance and for moving away from favouritism. Without free entry and failure, as in football, economic dynamism and momentum rapidly come to a halt.”

Continue reading here.

From a VoxEU post by Rabah Arezki:

“Algeria’s recent victory in the Africa Cup of Nations has united a country whose development model has frustrated its young and educated workforce. This column offers four lessons for economic development from the national football team’s success: on the role of competition and market forces, mobilising talent, the role of managers, and the importance of referees (i.e. regulation).

On 19 July,

Posted by at 8:09 AM

Labels: Inclusive Growth

Friday, August 16, 2019

Good for the environment, good for business: Foreign acquisitions and energy intensity

From a VoxEU post by Arlan Brucal, Beata Javorcik, and Inessa Love:

“The link between foreign ownership and environmental performance remains a controversial issue. Data from the Indonesian manufacturing census show that plants undergoing foreign acquisitions reduce their energy intensity by about 30% two years after acquisition by multinationals. This column argues that foreign direct investment can serve as a channel for the international transfer of environmentally friendly technologies and practices, thus directly contributing not only to economic growth but also to environmental progress.

According to the 2018 report of the UN Intergovernmental Panel on Climate Change (IPCC), exceeding the global threshold of 1.5°C above the pre-industrial temperature level will mean increased risk of extreme drought, wildfires, floods, and food shortages for hundreds of millions of people. Keeping emissions below the crucial threshold would require widespread changes in energy, industry, buildings, transportation, and cities. Can multinationals be part of the solution? Can flows of foreign direct investment (FDI) help put a brake on emissions? Or would they exacerbate the already worsening global climate condition?

Environmentalists argue that highly polluting multinationals relocate to countries with weaker environmental standards to circumvent costly regulations in their home country (Hanna 2010, Millimet and Roy 2015, Cai et al. 2016). In this way, they increase pollution levels not only in host countries but also globally.

In contrast, supporters of globalisation point out that FDI has a positive effect on the natural environment because multinationals tend to use more efficient and cleaner technologies than their domestic counterparts. With the spectacular growth in FDI flows and the increasing importance of developing nations as host countries, the potential effect of FDI on the natural environment remains controversial (Kellenberg 2009, Cole et al. 2017).

In a forthcoming paper (Brucal et al. 2019), we contribute to this discussion by examining the impact of foreign acquisitions on energy consumption and CO2 emissions of acquired plants. The study is based on plant-level data from the Indonesian Manufacturing Census, covering the period 1983-2001. The data contains detailed information on plant-level use of various energy inputs (both in value and physical units) and thus can be used to calculate the expected CO2 emissions using standard conversion factors specific to each type of energy. We then compare the changes in these variables in the acquired plants and a carefully selected group of domestic plants that had not changed ownership.1

Why would we expect acquired plants to improve energy efficiency?

There are several reasons why foreign acquisitions may improve energy efficiency. First, foreign acquisitions tend to increase production volume by boosting productivity and facilitating access to foreign markets through the foreign parent’s distribution network (Arnold and Javorcik 2009). This makes investments in improving energy efficiency more worthwhile as the sales base becomes large enough to cover the fixed cost of investment.”

Continue reading here.

From a VoxEU post by Arlan Brucal, Beata Javorcik, and Inessa Love:

“The link between foreign ownership and environmental performance remains a controversial issue. Data from the Indonesian manufacturing census show that plants undergoing foreign acquisitions reduce their energy intensity by about 30% two years after acquisition by multinationals. This column argues that foreign direct investment can serve as a channel for the international transfer of environmentally friendly technologies and practices,

Posted by at 9:50 AM

Labels: Energy & Climate Change

Monday, August 12, 2019

House Prices in China

From IMF’s latest report on China:

“The property market trended down. Growth in real estate investment (excluding land purchases) was mostly negative in 2018, and both house price growth and sales growth slowed since late 2018. Housing inventories have started to build up in recent months, suggesting the housing cycle may still be in a downturn.”

From IMF’s latest report on China:

“The property market trended down. Growth in real estate investment (excluding land purchases) was mostly negative in 2018, and both house price growth and sales growth slowed since late 2018. Housing inventories have started to build up in recent months, suggesting the housing cycle may still be in a downturn.”

Posted by at 10:58 AM

Labels: Global Housing Watch

Subscribe to: Posts