Friday, March 29, 2019

Housing Market in Sweden

From the IMF’s latest report on Sweden:

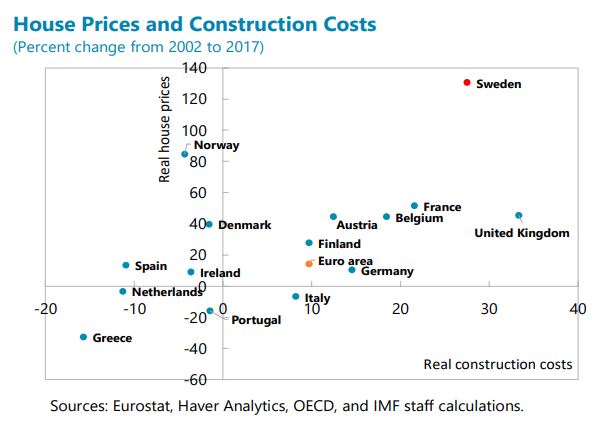

“High housing prices and high market rents increase vulnerabilities and inequality. Despite their recent moderation, house prices have tripled in real terms since the mid-1990s, lifting

the price-to-income (PTI) ratio to almost 30 percent above its 20-year average, with Stockholm’s PTI nearly twice the national average and among the highest worldwide. New purchasers must take on high debts relative to income (DTI), typically at floating rates, a macrofinancial vulnerability (…). Moreover, long queues for rent-controlled apartments meant that those unable to purchase housing had to pay much higher rents on subletted or newly constructed apartments, that are estimated to be 65 percent higher on average. An “insider-outsider” problem arises as labor mobility to the main centers is most impaired for those without parents able to assist with large down payments, impeding growth and exacerbating intergenerational and regional inequality.The “January agreement” includes promising steps but comprehensive housing reforms are needed given the scale of the problem. Key elements of a reform package include:

- Making the rental market work: in addition to fully liberalizing rents of newly constructed apartments, there is a need to phase out existing controls. A common approach is to apply market rents when there is a change in tenant. Access to the housing allowance could be expanded to cushion this adjustment (see below), while also applying a temporary “windfall” tax on significant rental income gains. To help reduce market rents more quickly, rental supply should be increased, such as by reducing impediments to sub-letting and to households renting out their own apartments, while containing macrofinancial risks from buy-to-let housing.

- Taxing property to rebalance the housing market: Sweden’s property tax was capped in 2008 to be among the lowest in the OECD, limiting the cost to households of occupying housing beyond their needs. A broad-based increase in the ceiling on the property tax would be most efficient, but an increase targeted to the main centers could be considered to incentivize mobility where it is most needed. Abolishing the interest on deferrals of capital gains taxes will help ease deterrents to mobility. An additional step to be considered is to tax only a portion of the capital gains on primary dwellings. Implementing a phase out of mortgage interest deductibility—which boosts housing demand and prices—would have limited impact on household finances currently given the low level of interest rates.

- Producing housing that is affordable: it is important to simplify the planning process to reduce the cost of construction which have risen by over 28 percent in real terms over the past 15 years, compared with 10 percent in the euro area. Productivity in the construction sector should be enhanced by strengthening competition, including by harmonizing land sale procedures across the municipalities and preventing requirements beyond national building standards in the approval process. The government should also expand existing subsidies for construction of affordable rental apartments, together with those for student and elderly housing in view of changing demographics.

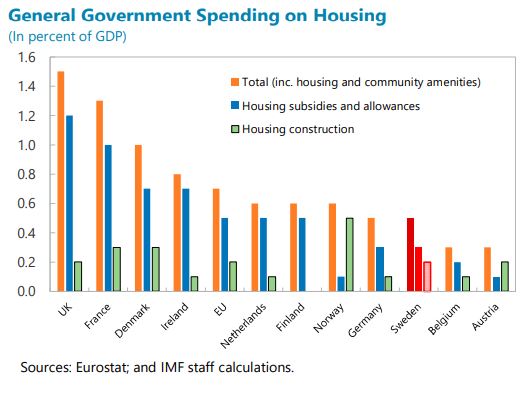

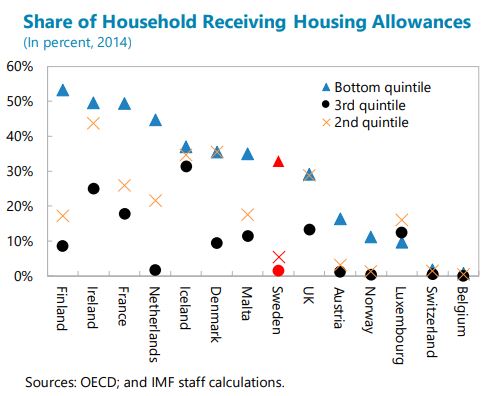

Protecting households in the transition is important to help build broad consensus on comprehensive reforms. On average, the share of rental expenditure in disposable income would increase from 24 percent to 31 percent, with most impact on households in the lowest income decile, which could be cushioned by expanding payments under the existing housing allowance. However, this allowance is seldom paid to households in the second or third income quintiles, contributing to relatively low total expenditure on housing allowances in Sweden. There is a need to review the coverage and amounts of housing allowances to give confidence that a transition to market rents will be manageable.

The authorities recognize the long-standing structural weaknesses in the Swedish housing market. They emphasized that housing policies were politically contentious in Sweden, limiting the feasibility of some reforms that could be most effective in principle, such as raising property taxation. Nevertheless, implementing the measures included in the “January agreement” during the term of the government would represent a step forward.”

From the IMF’s latest report on Sweden:

“High housing prices and high market rents increase vulnerabilities and inequality. Despite their recent moderation, house prices have tripled in real terms since the mid-1990s, lifting

the price-to-income (PTI) ratio to almost 30 percent above its 20-year average, with Stockholm’s PTI nearly twice the national average and among the highest worldwide. New purchasers must take on high debts relative to income (DTI), typically at floating rates,

Posted by at 10:25 AM

Labels: Global Housing Watch

Accounting for Urban China’s Rising Income Inequality: The Roles of the Labor Market, Human Capital, and Marriage Market Factors

From a new VoxChina post on China’s rising income inequality:

“China has witnessed persistent increases in economic inequality since the early 1990s when the urban labor market began its transformation — from centrally-controlled to market-driven. Using the Urban Household Survey data, this paper (Feng and Tang, 2018) documents the trends in income inequality over the period of 1992-2009 and decomposes changes in income inequality by considering three main factors: the labor market, human capital, and marriage market. We find that labor market factors account for approximately three-quarters of the overall increases in income inequality while the falling marriage rate has contributed the other quarter. Changes in human capital levels and marital assortativeness have not contributed to the rising inequality.”

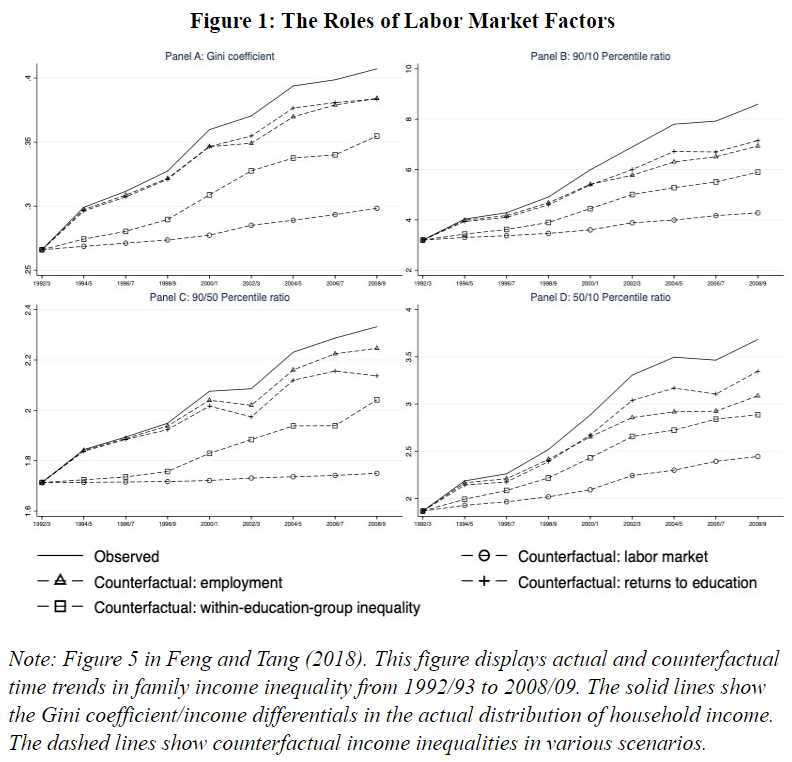

“Our results suggest that labor market factors are most important to the increases in family income inequality during the 1992-2009 period. Figure 1 shows that if allthree of the factors are held unchanged at the levels of 1992/93, the Gini coefficient would only increase from 0.266 to 0.298, instead of to the actual 0.407. Therefore, labor market factors collectively contribute more than three-quarters of the total increase in inequality. Further, labor market factors are more important in affecting the upper part of the income distribution as they account for almost all of the changes in P90/P50, the ratio of the 90th percentile to median family incomes.

A more careful examination suggests that each labor market factor plays an important role. Changes in employment and returns to education both contribute about 16 percent of the change in inequality over the study period, while within-education-group inequality accounts for around 37 percent of the overall increase in inequality. Therefore, within-education-group inequalities are not only crucial in changes to individual income inequality, as many previous researchers have noted, but are also important in the rise in regards to family income inequality.”

From a new VoxChina post on China’s rising income inequality:

“China has witnessed persistent increases in economic inequality since the early 1990s when the urban labor market began its transformation — from centrally-controlled to market-driven. Using the Urban Household Survey data, this paper (Feng and Tang, 2018) documents the trends in income inequality over the period of 1992-2009 and decomposes changes in income inequality by considering three main factors: the labor market,

Posted by at 10:20 AM

Labels: Inclusive Growth

I’m taking Friday off—permanently

From a new Social Europe post:

“Traditionally, higher productivity has benefited workers through reductions in working time, among other things. When the TUC was founded in 1868, average working hours were 62 per week. Now (including those who work part-time), average weekly hours have almost halved, to around 32.”

“That change didn’t happen by accident, but was the result of union campaigning. Robert Owen, the socialist pioneer who had popularised the demand for an eight-hour day at the beginning of the 19th century, coined the slogan: Eight hours’ labour, Eight hours’ recreation, Eight hours’ rest.

Following trade-union agitation, the Factory Acts of 1874 were the first kind of legislation to put clear limits on the working day—though back then, at ten hours, they fell short of union demands. The May Day demonstration of 1890, which drew hundreds of thousands of people to Hyde Park in London, was centred around the demand for an eight-hour day—following a call from the international trade-union movement for ‘a great international demonstration’ so that in all countries and all cities, on the appointed day, ‘the toiling masses shall demand of the State authorities the legal reduction of the working day to eight hours’.

And in 1919, when the International Labour Organisation (ILO) met for the first time in the wake of World War I, its initial convention was on working time. The preamble explicitly adopted ‘the principle of the 8 hours day or of the 48 hours week’ (though there was a long list of carve-outs—including the entirety of India).

So trade unions have an eye on history when they see predictions about the potential for extra wealth to be generated from robotics and artificial intelligence. The consultancy firm PWC has estimated that UK gross domestic product will be up to 10 per cent higher in 2030 as a result of artificial intelligence, equivalent to a boost to GDP of more than £20 billion, or extra spending power of up to £2,300 a year per household. One way that wealth could potentially be shared more equitably with workers is through a reduction in working time—as we saw in the last century.”

From a new Social Europe post:

“Traditionally, higher productivity has benefited workers through reductions in working time, among other things. When the TUC was founded in 1868, average working hours were 62 per week. Now (including those who work part-time), average weekly hours have almost halved, to around 32.”

“That change didn’t happen by accident, but was the result of union campaigning. Robert Owen, the socialist pioneer who had popularised the demand for an eight-hour day at the beginning of the 19th century,

Posted by at 10:16 AM

Labels: Inclusive Growth

Work of the past, work of the future

From a new VOX post by David Autor:

“Labour markets in US cities today are vastly more educated and skill-intensive than they were 50 years ago, but urban non-college workers now perform much less skilled work than they did. This column shows that automation and international trade have eliminated many of the mid-skilled non-college jobs that were disproportionately based in cities. This has contributed to a secular fall in real non-college wages.”

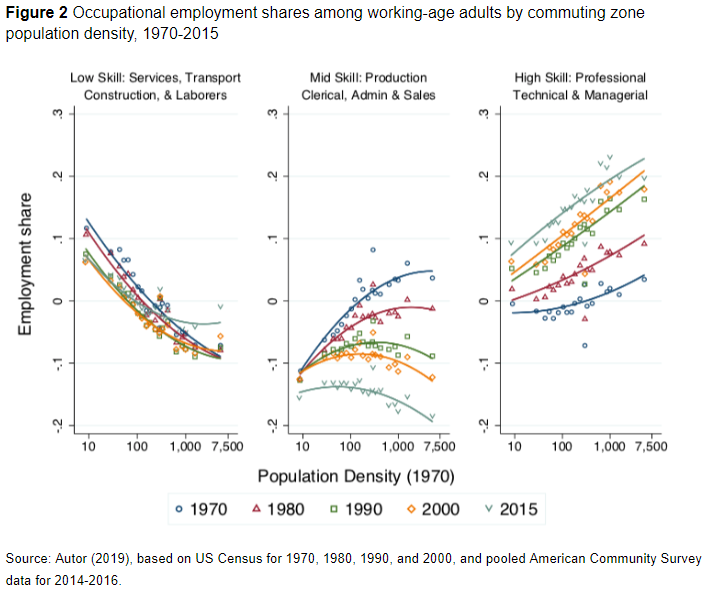

“Figure 2 depicts the aggregate relationship between population density and occupational structure at the level of 722 commuting zones (CZs) covering the contiguous US states between 1970 and 2015.

The three panels of this figure report the CZ-level share of employment among working-age adults into the three broad occupational categories described above: traditionally low-education, low-wage services, transportation, labourer, and construction workers; traditionally mid-education, middle-wage occupations made up of clerical, administrative support, sales, and production workers; and high-education, high-wage, professional, technical, and managerial workers.

The horizontal axis is the natural log of population density (the number of residents divided by CZ land area). For consistency, I used each zone’s population density in 1970 throughout, and the data are weighted by the count of working-age adults in each CZ. Each plotted point in the bin-scatter represents approximately 5% of all workers in each year.

The rising set of upward-sloping curves in the right panel show that while denser CZs have traditionally been more intensive in high-skill work, the level and slope of this relationship between density and skill-intensity has risen consistently over multiple decades. The overlapping downward-sloping curves in the left panel show that the fraction of workers engaged in low-skill occupations has historically been much smaller in high-density CZs, and this pattern has changed little over decades. In the middle panel, the fan-shaped set of curves show that the denser CZs were exceptional in the 1970s for having far more middle-skill work than suburban and rural CZs. But this exceptional feature attenuated. By 2015, the densest CZs had less middle-skill work than the suburbs or rural areas.”

From a new VOX post by David Autor:

“Labour markets in US cities today are vastly more educated and skill-intensive than they were 50 years ago, but urban non-college workers now perform much less skilled work than they did. This column shows that automation and international trade have eliminated many of the mid-skilled non-college jobs that were disproportionately based in cities. This has contributed to a secular fall in real non-college wages.”

Posted by at 10:13 AM

Labels: Inclusive Growth

Housing View – March 29, 2019

On cross-country:

- Scared of Stocks? Buy a House Instead – Bloomberg

- Can Upzoning Increase Housing Supply and Affordability? – Planetizen

- Changing the Housing Story – the Shaping Futures report – SF21

On the US:

- Why Housing Policy Is Climate Policy – New York Times

- Three Scenarios for Growth in Homeowner and Renter Households – Harvard Joint Center for Housing Studies

- How Poor Americans Get Exploited by Their Landlords – Citylab

- A Growing Problem in Real Estate: Too Many Too Big Houses – Wall Street Journal

- Rural America Faces a Housing Cost Crunch – Pew Charitable Trusts

- Zoned Out? The Determinants of Manufactured Housing Rents: Evidence from North Carolina – Journal of Housing Economics

- U.S. housing, consumer confidence data point to slowing economy – Reuters

- A Decade After the Housing Bust, the Exurbs Are Back – Wall Street Journal

On other countries:

- [Australia] Australia central bank research shows income, not just property weakness, key for policy – Reuters

- [Australia] Australia’s Property Stocks Are Ignoring the Housing Slump – Bloomberg

- [Canada] Trudeau housing plan ignores local drivers of affordability – Fraser Institute

- [Canada] The Big Short’s Steve Eisman raises bets against Canadian banks – Financial Times

- [Canada] Housing Is a Magnet for Money Launderers in Toronto: Study – Bloomberg

- [China] That Property Boom Could Be the Reason Employees Are Goofing Off – Bloomberg

- [Denmark] World’s Cheapest Mortgage May Be Around the Corner in Denmark – Bloomberg

- [Finland] Finland’s housing market remains weak – Global Property Guide

- [Italy] Italy House Price Drop Adds Woe for Economy in Recession – Bloomberg

- [Netherlands] Brexit Is Making It Even Harder to Find a Flat in Amsterdam – Bloomberg

- [United Arab Emirates] How Dubai can solve its lack of affordable housing – World Economic Forum

On cross-country:

- Scared of Stocks? Buy a House Instead – Bloomberg

- Can Upzoning Increase Housing Supply and Affordability? – Planetizen

- Changing the Housing Story – the Shaping Futures report – SF21

On the US:

- Why Housing Policy Is Climate Policy – New York Times

- Three Scenarios for Growth in Homeowner and Renter Households – Harvard Joint Center for Housing Studies

- How Poor Americans Get Exploited by Their Landlords – Citylab

- A Growing Problem in Real Estate: Too Many Too Big Houses – Wall Street Journal

- Rural America Faces a Housing Cost Crunch – Pew Charitable Trusts

- Zoned Out?

Posted by at 10:05 AM

Labels: Global Housing Watch

Subscribe to: Posts