Saturday, September 29, 2018

Francesco Saraceno on the End of the (Macro) Consensus

From a new paper by Francesco Saraceno:

“The New Consensus that has dominated macroeconomics since the 1980s was based on a fundamentally neoclassical structure: efficient markets that on their own converged on a natural equilibrium with a very limited role for macroeconomic (mostly monetary) policy to smooth fluctuations. The crisis shattered this consensus and saw the return of monetary and fiscal activism, at least in academic debate. The profession is reconsidering the pillars of the Consensus, from the size of the multipliers to the implementation of reform, including the links between business cycles and trends. It is still too soon to know what macroeconomics will look like tomorrow, but hopefully it will be more eclectic and open. ”

From a new paper by Francesco Saraceno:

“The New Consensus that has dominated macroeconomics since the 1980s was based on a fundamentally neoclassical structure: efficient markets that on their own converged on a natural equilibrium with a very limited role for macroeconomic (mostly monetary) policy to smooth fluctuations. The crisis shattered this consensus and saw the return of monetary and fiscal activism, at least in academic debate. The profession is reconsidering the pillars of the Consensus,

Posted by at 11:42 AM

Labels: Inclusive Growth

Friday, September 28, 2018

Technology and the Future of Work

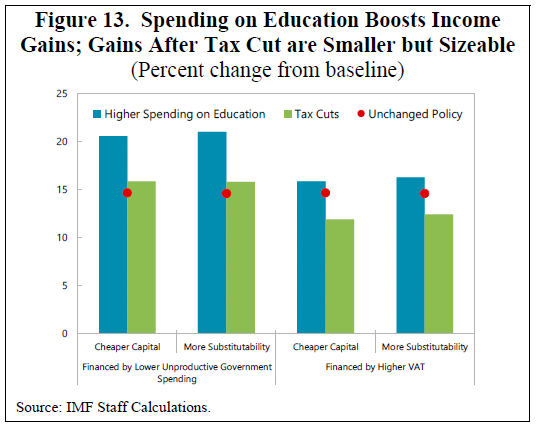

A new IMF working paper “uses a DSGE model to simulate the impact of technological change on labor markets and income distribution. It finds that technological advances offers prospects for stronger productivity and growth, but brings risks of increased income polarization. This calls for inclusive policies tailored to country-specific circumstances and preferences, such as investment in human capital to facilitate retooling of low-skilled workers so that they can partake in the gains of technological change, and redistributive policies (such as differentiated income tax cuts) to help reallocate gains. Policies are also needed to facilitate the process of adjustment.”

“Policies can change the impact of technological change. Depending on societies’ preferences for growth versus income equality, governments may want to distribute the gains from technology more evenly. Certain policies, if well designed, could mitigate the trade-off between both objectives. For example, illustrative model simulations show that higher education spending would not only allow low-skilled workers to participate in the gains of technological change, it would also increase output; this holds even when taking into account that higher spending will require higher rates of taxation. More generally, while the use of the tax/benefit system to redistribute the gains from technological advances tends to come with some loss in efficiency, the resulting loss in output tends to be relatively small.”

A new IMF working paper “uses a DSGE model to simulate the impact of technological change on labor markets and income distribution. It finds that technological advances offers prospects for stronger productivity and growth, but brings risks of increased income polarization. This calls for inclusive policies tailored to country-specific circumstances and preferences, such as investment in human capital to facilitate retooling of low-skilled workers so that they can partake in the gains of technological change,

Posted by at 6:12 PM

Labels: Inclusive Growth

Housing View – September 28, 2018

On the US:

- Perception of House Price Risk and Homeownership – NBER

- Affordable Housing: Hard Way and Easy Way – Cato Institute

- Barriers to Accessing Homeownership Down Payment, Credit, and Affordability – 2018 – Urban Institute

- Texas Property Taxes Soar as Homeowners Confront Rising Values – Federal Reserve Bank of Dallas

- The housing bubble, the credit crunch, and the Great Recession: A reply to Paul Krugman – Brookings

- America Needs to Revive the American Dream of Homeownership – Bloomberg

- How Much Will Homeowners Spend to Rebuild & Repair After Hurricane Florence? – Harvard Joint Center for Housing Studies

- Affordable housing is just the beginning of YIMBY – VOX

- Builders Slump as U.S. Housing Market Shifts to the Slow Lane – Bloomberg

- Is There a Better Way to Measure Housing Affordability? – Harvard Joint Center for Housing Studies

- Elizabeth Warren’s Ambitious Fix for America’s Housing Crisis – The Atlantic

- School shootings affect school quality, housing value – University of Illinois at Urbana – Champaign

- Building More Houses Isn’t Always the Answer – Bloomberg

On other countries:

- [Chile] ¿Cómo influye la cercanía del Metro en el valor de una propiedad? – CNN

- [China] Understanding Real Estate Price Dynamics: The Case of Housing Prices in Five Major Cities of China – Journal of Housing Economics

- [China] How Much Would China’s GDP Respond to a Slowdown in Housing Activity? – Federal Reserve Bank of Kansas City

- [China] China Developers’ Funding Source at Risk in Sales Crackdown – Bloomberg

- [Germany] Germany sets out measures to tackle affordable housing shortage – Reuters

- [Germany] Germany’s soaring housing prices spark calls for reform – Deutsche Welle

- [Hong Kong] Higher interest rates threaten overvalued property markets – Financial Times

- [Hong Kong] Hong Kong at greatest risk of housing bubble: UBS – Financial Times

- [United Kingdom] Is Richmond the Nimbyest place in London? – Financial Times

Photo by Aliis Sinisalu

On the US:

- Perception of House Price Risk and Homeownership – NBER

- Affordable Housing: Hard Way and Easy Way – Cato Institute

- Barriers to Accessing Homeownership Down Payment, Credit, and Affordability – 2018 – Urban Institute

- Texas Property Taxes Soar as Homeowners Confront Rising Values – Federal Reserve Bank of Dallas

- The housing bubble, the credit crunch,

Posted by at 5:00 AM

Labels: Global Housing Watch

Thursday, September 27, 2018

What is the yield curve forecasting?

From a new post by David Andolfatto:

“Does the recent flattening of the yield curve portend recession? Not necessarily. The flattening of the real yield curve may simply reflect the fact that real consumption growth is not expected to accelerate or decelerate from the present growth rate of about 1% per annum. On the other hand, a 1% growth rate is substantially lower than the historical average of 2% in the United States. Because of this, the risk that a negative shock (of comparable magnitude to past shocks) sends the economy into technical recession is increased. While the exact date at which the shock arrives is itself is unpredictable, the likelihood of recession is higher relative to a high real interest rate, high growth economy.”

From a new post by David Andolfatto:

“Does the recent flattening of the yield curve portend recession? Not necessarily. The flattening of the real yield curve may simply reflect the fact that real consumption growth is not expected to accelerate or decelerate from the present growth rate of about 1% per annum. On the other hand, a 1% growth rate is substantially lower than the historical average of 2% in the United States.

Posted by at 5:48 PM

Labels: Forecasting Forum

Underemployment in the US and Europe

From a new VOX post:

“The most widely available measure of underemployment is the share of involuntary part-time workers in total employment. This column argues that this does not fully capture the extent of worker dissatisfaction with currently contracted hours. An underemployment index measuring how many extra or fewer hours individuals would like to work suggests that the US and the UK are a long way from full employment, and that policymakers should not be focused on the unemployment rate in the years after a recession, but rather on the underemployment rate. ”

“Figure 2 shows our estimates for the UK of the number of desired hours of those who want more hours (the underemployed) and those who want less (the overemployed) at the going wage. The latter series was broadly flat until recently but was always above the fewer hours series before 2008. That suggests there is still a good deal of under-utilized resources in the labour market available to be used up before the UK reaches full-employment. There has been a rise both in the number of hours of those who want more hours and those who want less in the post-recession years. ”

From a new VOX post:

“The most widely available measure of underemployment is the share of involuntary part-time workers in total employment. This column argues that this does not fully capture the extent of worker dissatisfaction with currently contracted hours. An underemployment index measuring how many extra or fewer hours individuals would like to work suggests that the US and the UK are a long way from full employment, and that policymakers should not be focused on the unemployment rate in the years after a recession,

Posted by at 5:36 PM

Labels: Inclusive Growth

Subscribe to: Posts