Wednesday, June 28, 2017

Cross-Country Spillovers of Fiscal Consolidations in the Euro Area

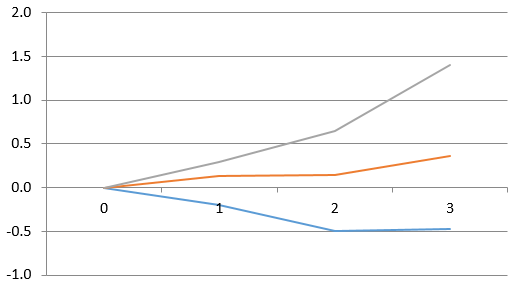

An IMF working paper finds: “This paper assesses spillovers from fiscal consolidations in 10 euro area countries using an innovative empirical methodology. The analysis lends support to the existence of fiscal spillovers, with fiscal consolidation in one country reducing not only the domestic output but also the output of other member states. Spillover effects are larger for: (i) more closely located and economically integrated countries, and (ii) for fiscal shocks originating from relatively larger countries. Most of the impact comes from revenue measures, while the impact of expenditure measures is relatively weaker. The latter result is consistent with the distortionary effects of taxation and empirical literature on fiscal multipliers using the narrative approach (Leigh and others 2010; Abiad and others 2011).

Our results have important policy implications. They suggest that fiscal consolidations in individual euro area countries, especially the larger ones, can reduce aggregate demand in others. The magnitude of cross-country spillovers has strengthened with the economic integration and introduction of a single currency. Also, spillovers can be larger if fiscal consolidations are implemented in downturns. Therefore, individual euro area countries should consider fiscal measures implemented in other members as well as the state of the economy when implementing domestic policies.”

For previous IMF work on negative demand spillovers in the euro area, see my VoxEU blog and Larry Elliott’s column.

Figure 1. Impact on Eurozone output from wage moderation, quantitative easing and structural

An IMF working paper finds: “This paper assesses spillovers from fiscal consolidations in 10 euro area countries using an innovative empirical methodology. The analysis lends support to the existence of fiscal spillovers, with fiscal consolidation in one country reducing not only the domestic output but also the output of other member states. Spillover effects are larger for: (i) more closely located and economically integrated countries, and (ii) for fiscal shocks originating from relatively larger countries.

Posted by at 4:19 PM

Labels: Inclusive Growth, Macro Demystified

House Prices in Peru

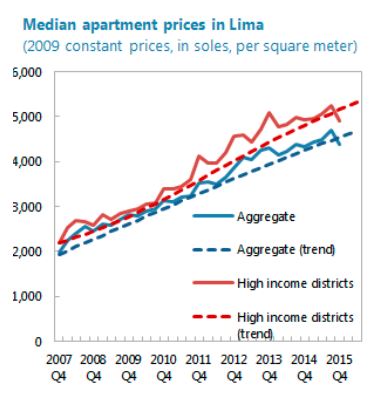

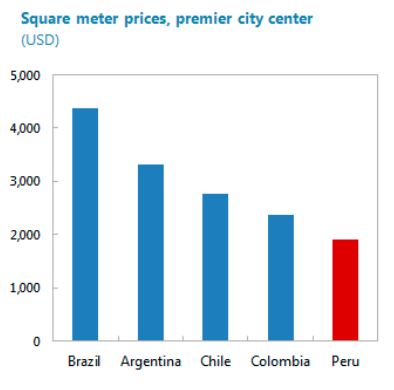

“The property sector has grown rapidly, though there has been some price moderation recently and indicators do not suggest overheating. Prices have risen over the decade, in tandem with Peru’s economic expansion. In Q2 2016, the growth in median apartment prices in Lima softened compared to Q2 2015, but remained well above the 5-year average. Valuation indicators show that Peru’s property market is on an average footing compared to regional peers (…). The country also faces a housing deficit, particularly in the lower-income segments, and buying patterns do not appear speculative. Furthermore, property price indices in Peru only reflect the capital, Lima, which has a higher population growth and urbanization level than the rest of the country”, according to the IMF’s annual economic report on Peru.

“The property sector has grown rapidly, though there has been some price moderation recently and indicators do not suggest overheating. Prices have risen over the decade, in tandem with Peru’s economic expansion. In Q2 2016, the growth in median apartment prices in Lima softened compared to Q2 2015, but remained well above the 5-year average. Valuation indicators show that Peru’s property market is on an average footing compared to regional peers (…). The country also faces a housing deficit,

Posted by at 3:39 PM

Labels: Global Housing Watch

Tuesday, June 27, 2017

Housing View – June 27, 2017

On macroprudential policy:

- Stanley Fischer on Housing and Financial Stability – Federal Reserve Board

- DNB-Riksbank Macroprudential Conference – De Nederlandsche Bank

On cross-country:

- Global House Price Index – Q1 2017 – Knight Frank

- Q1 2017: World’s housing markets poised to slow, though the boom continues strongly in Europe, Canada, and some parts of Asia – Global Property Guide

- Global developments in residential property prices – Bank for International Settlements

- Europe’s Next Housing Boom Raises Red Flags in Ex-Communist East – Bloomberg

- Relevamiento Inmobiliario de América Latina – Universidad Torcuato Di Tella

- Recent Trends and Developments in European Mortgage Markets – CEPS

- House prices and monetary policy in the euro area: evidence from structural VARs – European Central Bank

- A housing policy that could almost pay for itself? Think retrofitting – World Bank

On the US:

- Is a Bubble Brewing in the Multifamily Housing Market? – Federal Reserve Bank of St. Louis

- The State of the Nation’s Housing 2017 – Harvard Joint Center for Housing Studies

- Does it matter whether those who lost their homes during the crisis come back to the housing market? – Federal Reserve Bank of Richmond

- Housing Constraints and Spatial Misallocation – University of California, Berkeley

- Dynamics of Housing Debt in the Recent Boom and Great Recession – NBER

On other countries:

- Is Australia’s property market overheating? – The Economist

- The lessons from Canada’s attempts to curb its house-price boom – The Economist

- Czech central bank moves to rein in lending in ‘overvalued’ property market – Financial Times

- How can we dampen the build-up of housing price bubbles? – Bank of Finland

- A review of residential mortgage lending in 2016 – Central Bank of Ireland

- [New Zealand] House prices slow, and will likely keep slowing – CoreLogic

- South Korea tightens rules on housing to restrain buying frenzy in some cities – Reuters

- [Spain] Buen desempeño del mercado inmobiliario en 1T17 – BBVA

On macroprudential policy:

- Stanley Fischer on Housing and Financial Stability – Federal Reserve Board

- DNB-Riksbank Macroprudential Conference – De Nederlandsche Bank

On cross-country:

- Global House Price Index – Q1 2017 – Knight Frank

- Q1 2017: World’s housing markets poised to slow, though the boom continues strongly in Europe, Canada, and some parts of Asia – Global Property Guide

- Global developments in residential property prices –

Posted by at 5:00 AM

Labels: Global Housing Watch

Monday, June 26, 2017

House Prices in Ireland

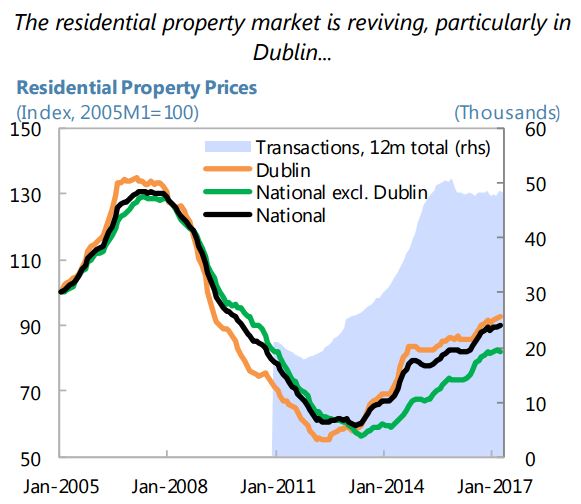

IMF’s new report on Ireland says that: “Strong momentum in the housing market requires close monitoring. Recent policy actions to address homelessness, improve housing affordability and the recalibration of macroprudential measures may have added impetus to the market, which also has seen an increase in price expectations and a surge in mortgage approvals. This suggests that strong demand is likely to be sustained in the period ahead, particularly given the positive momentum in the labor market and improved household balance sheets. Staff analysis—though subject to uncertainty—finds no clear evidence of a significant price misalignment in the residential property market (…), yet persistent pressures could lead to imbalances, particularly given the lagged supply response.”

IMF’s new report on Ireland says that: “Strong momentum in the housing market requires close monitoring. Recent policy actions to address homelessness, improve housing affordability and the recalibration of macroprudential measures may have added impetus to the market, which also has seen an increase in price expectations and a surge in mortgage approvals. This suggests that strong demand is likely to be sustained in the period ahead, particularly given the positive momentum in the labor market and improved household balance sheets.

Posted by at 6:05 PM

Labels: Global Housing Watch

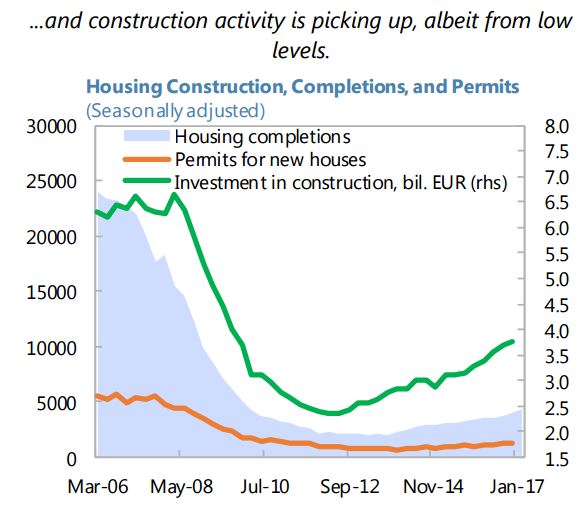

House Prices in Czech Republic

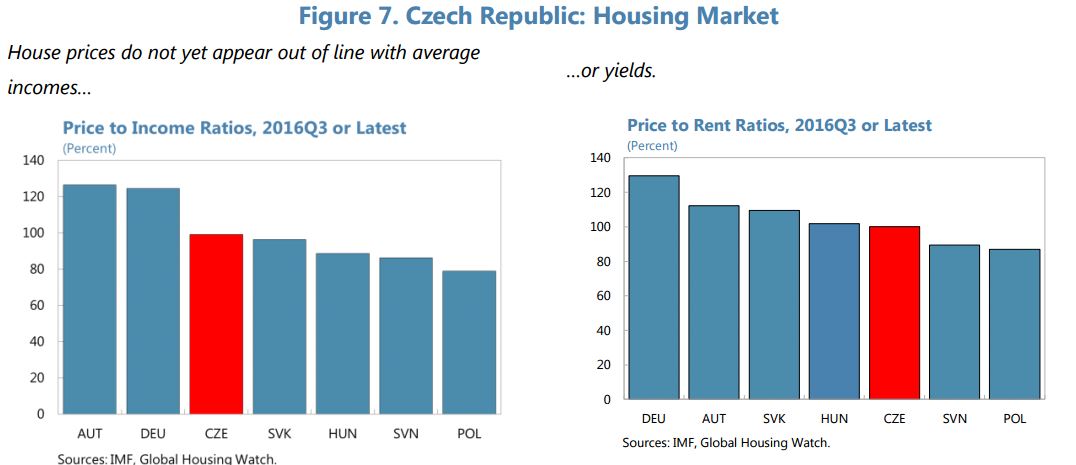

“Real estate values have also been increasing quickly. House prices have escalated rapidly from a post-crisis trough in 2012, both in Prague and outside the capital region. The increases are in line with those in neighboring countries, and simple metrics—price to income and price to rent ratios—do not yet show current house price levels to be unusually high (Figure 7, charts 1–2). However, data gaps preclude a more conclusive analysis—in particular, an aggregate price index for the commercial real estate market is not publicly available”, says IMF’s new report on Czech Republic.

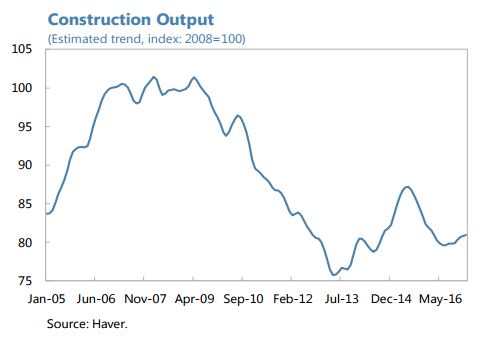

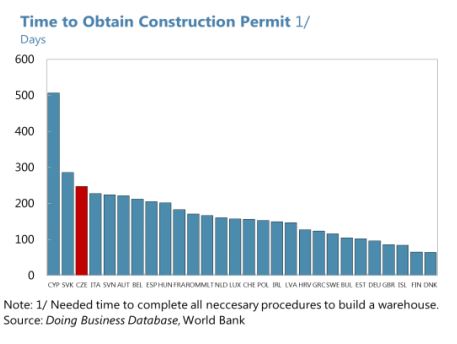

On housing supply the report says that: “House price increases are amplified by inelastic supply. Construction declined considerably after the global financial crisis, and has not recovered significantly, despite the increase in house prices. In addition, the processes for obtaining necessary permits are long, complex, and often inconsistent, limiting the ability of supply to respond quickly to demand.”

“Real estate values have also been increasing quickly. House prices have escalated rapidly from a post-crisis trough in 2012, both in Prague and outside the capital region. The increases are in line with those in neighboring countries, and simple metrics—price to income and price to rent ratios—do not yet show current house price levels to be unusually high (Figure 7, charts 1–2). However, data gaps preclude a more conclusive analysis—in particular, an aggregate price index for the commercial real estate market is not publicly available”,

Posted by at 5:56 PM

Labels: Global Housing Watch

Subscribe to: Posts