Monday, February 29, 2016

Housing Market in the United Kingdom

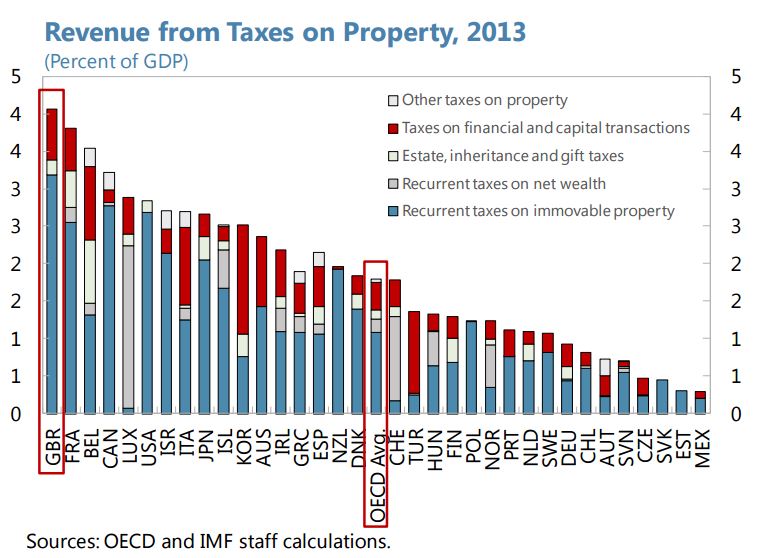

A separate IMF paper examines how tax reforms could help ease structural supply constraints in the UK’s housing market. “Property taxation in the UK delivers larger revenue as a percent of GDP than any other OECD country. (…) However, a closer look at the UK’s property tax system suggests that some areas could be reformed to reduce constraints on housing supply and thereby reduce risks stemming from high house prices. In particular, deducing council tax discounts [and (…)] reducing reliance on the stamp duty land tax.”

“Housing markets have decelerated somewhat since mid-2014, but significant pressures remain. (…) Persistent upward pressure on house prices partly reflects supply constraints. (…) High house prices result in some households taking on high leverage, posing financial stability risks. (…) Further macroprudential tightening may thus be needed if the reduction in high leverage mortgages does not continue”, says the IMF’s new report on the United Kingdom.

A separate IMF paper examines how tax reforms could help ease structural supply constraints in the UK’s housing market.

Posted by at 10:00 AM

Labels: Global Housing Watch

Thursday, February 25, 2016

Inequality and opening up to foreign capital and inequality: some new results

In June 1979, shortly after winning a landmark election, Margaret Thatcher eliminated restrictions on “the ability to move money in and out” of the United Kingdom, which some of her supporters regard as “one of her best and most revolutionary acts” (Heath, 2015).

Thatcher’s critics [have] regarded this same liberalization as starting a global trend whose “downside . . . proved to be painful” (Schiffrin, 2016). In their view, while the free mobility of capital across national borders confers many benefits in theory, in practice liberalization has often led to economic volatility and financial crisis. This in turn has adverse consequences for many in the economy, particularly for those who are not well off. Liberalization also affects the relative bargaining power of companies and workers (that is, of capital and labor, respectively, in the jargon of economists) because capital is generally able to move across national boundaries with greater ease than labor. The threat of being able to move production abroad reduces labor’s bargaining power and the share of the income pie that goes to workers.

In studying such distributional effects of capital account liberalization, Davide Furceri and I found that after countries take steps to open their capital account, an increase in inequality in incomes within countries follows (Furceri and Loungani, 2015). The impact is greater when liberalization is followed by a financial crisis and in countries where there is low financial development—that is, where financial institutions are small and access to these institutions is limited. We also find that the share of income going to labor declines in the aftermath of liberalization. Thus, like trade liberalization, capital account liberalization can lead to winners and losers. But while the distributional effects of trade have long been studied by economists, the distributional impacts of opening the capital account are just starting to be analyzed.

Read the rest of this (non-technical) summary of our results here: http://www.imf.org/external/pubs/ft/fandd/2016/03/furceri.htm

Here’s a link to the IMF Working Paper: http://www.imf.org/external/pubs/ft/wp/2015/wp15243.pdf

Earlier versions of this research, based on data for advanced economies, were featured on Krugman’s blog and in VoxEU. These new results extend our results to developing economies as well as lay out possible channels through which capital account liberalization leads to inequality.

After countries remove restrictions on capital flows, inequality often gets worse

In June 1979, shortly after winning a landmark election, Margaret Thatcher eliminated restrictions on “the ability to move money in and out” of the United Kingdom, which some of her supporters regard as “one of her best and most revolutionary acts” (Heath, 2015).

Thatcher’s critics [have] regarded this same liberalization as starting a global trend whose “downside . .

Posted by at 4:11 PM

Labels: Inclusive Growth

Wednesday, February 24, 2016

Experts Weigh in on the State of the Global Housing Market

“Global house price boom accelerates further, led by Europe, North America, and some parts of Asia Pacific”, according to the Q3 2015 quarterly note from the Global Property Guide. This house price boom is reflected in two measures. First, real house prices rose in 28 out of a sample of 41 countries. Second, there is stronger upward momentum—in 22 countries house prices have risen faster compared to the previous quarter. These results are also in line with the Q3 2015 data reported by Knight Frank. Of the 55 housing markets tracked by Knight Frank, 82 percent recorded positive annual price growth, up from 75 percent. However, FITCH notes that even though the housing and mortgage outlook for the 22 countries remain stable/positive, divergence is increasing.

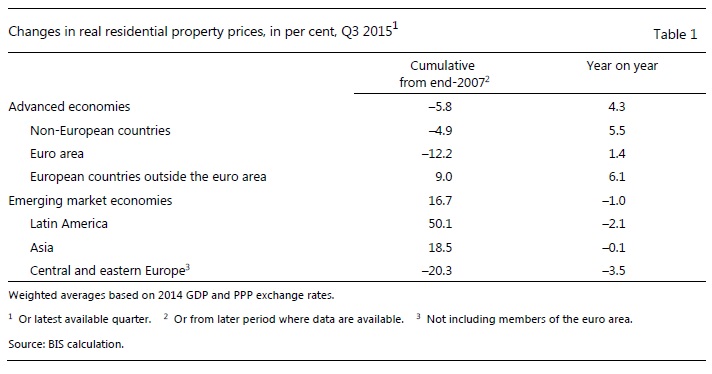

Looking at global house price developments in more detail, the Bank for International Settlement (BIS) says that real house prices increased by 4.3 percent year-on-year in advanced economies vs. a decline of 1.0 percent in emerging market economies. Within emerging market economies, the BIS notes that “there were significant disparities across countries: while prices continued to rise strongly in Hong Kong SAR, India and Turkey, they kept falling in Brazil, China and Russia.” Going forward, “the EM house price boom will be curbed by slowing income growth and weaker economic prospects”, says Oxford Analytica.

In the Euro area—where house price data coverage is higher compared to other regions—house prices rose by 2.3 percent in the third quarter of 2015 compared with the same quarter of the previous year, according to Eurostat. On the outlook for Europe, FITCH says that “Rising GDP, low rates, recovering credit flows, and improving labour markets will support the bounce-back in the eurozone periphery.” Moreover, according to Urban Land Institute’s Emerging Trends Europe, the five leading cities for investment prospects in 2016 are Berlin at Number 1, followed by Hamburg, Dublin, Madrid and Copenhagen.

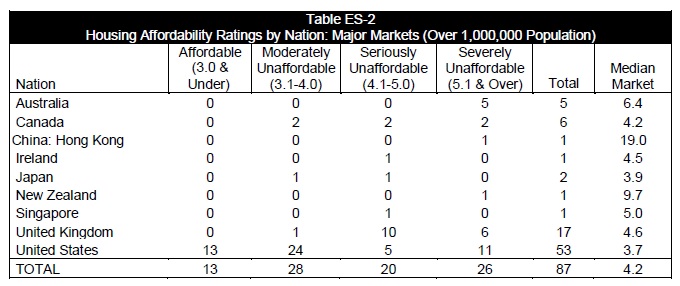

Finally, the latest survey from Demographia International Housing Affordability Survey finds that “The most affordable major metropolitan markets in 2015 were in the United States, which had a moderately unaffordable rating of 3.7, followed by Japan, with a Median Multiple of 3.9. Major metropolitan markets were rated “seriously unaffordable,” in Canada (4.2), Ireland (4.5), the United Kingdom (4.6) and Singapore (5.0). The major markets of Australia (6.4), New Zealand (9.7) and Hong Kong (19.0) were severely unaffordable.”

From the Global Housing Watch Newsletter: February 2016

“Global house price boom accelerates further, led by Europe, North America, and some parts of Asia Pacific”, according to the Q3 2015 quarterly note from the Global Property Guide. This house price boom is reflected in two measures. First, real house prices rose in 28 out of a sample of 41 countries. Second, there is stronger upward momentum—in 22 countries house prices have risen faster compared to the previous quarter.

Posted by at 10:00 AM

Labels: Global Housing Watch

Tuesday, February 23, 2016

Financial Development, Inequality and Poverty: Some International Evidence

A new IMF paper by Sami Ben Naceur and RuiXin Zhang “(…) provides evidence on the link between financial development and income distribution. Several dimensions of financial development are considered: financial access, efficiency, stability, and liberalization. Each aspect is represented by two indicators: one related to financial institutions, and the other to financial markets. Using a sample of 143 countries from 1961 to 2011, the paper finds that four of the five dimensions of financial development can significantly reduce income inequality and poverty, Read the full article…

Posted by at 3:51 PM

Labels: Inclusive Growth

Friday, February 19, 2016

The IMF’s Interest in Inclusive Growth: Promising or PR?

My presentation today at CIGI tries to provide a framework for the IMF’s various recent policy forays and some of the key changes in IMF advice.

Posted by at 9:25 PM

Labels: Inclusive Growth

Subscribe to: Posts