Thursday, December 31, 2015

The Top Ten Blogs of 2015

1. Lower unionization associated with increased inequality: IMF F&D

2. Jobs & Inequality: Special Feature in Finance & Development

5. On Groundhog Day, Honoring A Forecasting Giant

6. On U.S. Labor Market Slack: Updated Estimates of the Impact of Uncertainty on Unemployment

7. Understanding China’s Housing Market

8. Uncertainty and U.S. Unemployment

Below is a list of the most read blogs of the year:

1. Lower unionization associated with increased inequality: IMF F&D

2. Jobs & Inequality: Special Feature in Finance & Development

3. Fund Fires Employment Guru?

4. India’s Housing Market: What’s happened? What’s next?

5. On Groundhog Day, Honoring A Forecasting Giant

6. On U.S. Labor Market Slack: Updated Estimates of the Impact of Uncertainty on Unemployment

7.

Posted by at 12:55 PM

Labels: Uncategorized

Tuesday, December 29, 2015

Thomas Sargent Recounts History of U.S. Debt Limits

On December 2, Thomas Sargent, 2011 Nobel Laureate in Economics, delivered the inaugural Richard Goode Lecture at the IMF. Convened by the IMF’s Fiscal Affairs Department (FAD), the Richard Goode Lecture, named after FAD’s first director, who served from 1965–1981, is designed to bring together annually academia and policymakers to discuss important topics of fiscal policy.

As noted by David Lipton, First Deputy Managing Director of the IMF, the forum “will offer an opportunity to reflect on the evolution of fiscal policy and think about fiscal challenges that lie ahead.”

In his address, Sargent, the William R. Berkley Professor of Economics and Business at New York University, the Donald L. Lucas Professor in Economics, Emeritus, at Stanford University, and Senior Fellow at the Hoover Institution, discussed the role debt limits have played throughout the economic and financial history of the United States. IMF Survey sat with Sargent to discuss his work on the debt limits.

IMF Survey: Professor Sargent, could you please explain the role debt limits have played in the economic history of the U.S.?

Sargent: Based on the evidence that my friend George Hall and I have assembled, the answer is different before 1917 and after 1939.

Before 1917, there was not an aggregate debt limit. Instead, interestingly, there was a debt limit bond by bond. Congress designed every bond and put a limit on the amount that could be issued. And those limits were taken seriously. They seem to have provided information about what upper bound on what future debt would be, except during wars.

After 1939, an aggregate debt limit was created for the first time. It restricts the par value of the total amount of debt. If you adjust for inflation, in real value, the government debt limit was constant until a little after 1980. It actually went down after 1945. In real terms, the value of debt relative to GDP went down even more. After 1983, nominal debt limits rose and more than inflation except in the Clinton administration. So, as I said, the answer seems to differ substantially after 1939 and before 1917.

IMF Survey: And what was the reason for moving from this bond-by-bond approach to the aggregate limit?

Sargent: Good question. The U.S. Secretary of the Treasury, Andrew Mellon, gave his reasons. After World War I, the federal government had big debts. These debts were in discrete issues of bond of particular maturities. They were issued in big lumps with “echo effects”: lumpy debt service events; potential liquidity and roll-over risks. In the 1920s, the U.S. ran a primary surplus, but not big enough to service all the debt that would come due. So when those big bonds matured, Mellon knew that he was going to have to ask Congress for authority to issue new bonds. He foresaw those “echo effects”. So he asked Congress for authority and flexibility to smooth those things over time. Congress assented. Mellon wanted to manage the debt in ways that would increase the liquidity and allow him freedom basically to be a good portfolio manager.

It is interesting why Congress assented to Mellon’s request while it had denied such requests from earlier Secretaries of the Treasury. You have to know more about the politics of the times than I do to answer that question. The Republicans had big majorities in Congress in the 1920s and they mostly trusted Mellon. Congress evidently thought Mellon’s was a reasonable request and at that time he was respected a lot.

IMF Survey: When would debt limits work effectively in restricting spending?

Sargent: I don’t know. I began this talk [Richard Goode lecture] with a quote from a smart Assistant Treasury Secretary who said debt limits are totally a sideshow, meaning that they are totally irrelevant. Just entertainment. But if you go back to 19th century, they seem to have been taken seriously. In various episodes, they constrained what the President and the Secretary of the Treasury could do, or thought that they could do. Something must have changed between then and now. We are trying to learn more about those changes or at least to frame the question.

IMF Survey: What lessons can policymakers in other countries learn from the U.S.?

Sargent: This is speculative, but the way I look at it is that any decision maker, whether he or she admits it, has two things: (1) a model about the way the world is put together, and (2) some interests they want to advance or protect, that is their constituents’ interests. To me, they try to do the best they can in terms of their constituents’ interests, given their understanding of the way the world is put together. They have theories of economics, including theories about government fiscal policy, whether it matters or not, how it matters.

I think if you go back in the 19th century and try to read and listen, people talk about their theories. Congressmen and journalists discussed and debated them. Presidential elections were fought about intricate technical matters of monetary policy: the silver standard, the greenback, the gold standard, bimetallism. It looks to me as though people on both sides had a common theory.

I believe that the economic doctrines that are in policymakers’ heads are very important. It is very corny to say it, but it is still true.

IMF Survey: How about the IMF? What can we learn from this history?

Sargent: The IMF was set up for good reasons. Keynes and Harry Dexter White and many other good people wanted to solve problems that had devastated the world economy after World War I: adjusting international monetary policies and international debts. The founders of the IMF had theories about how the international monetary system could be set up to handle adverse events in ways that would attenuate adverse consequences.

I see a pretty straight line: the IMF has embodied that theory in a set of practices. I view it as an important institution that seeks to keep alive the thoughts and concerns of its founders. For better or worse, in some countries, they say we don’t want to do it the IMF way. Well, the IMF way is that you have to respect the government budget constraint, mostly from your own domestic taxpayers’ resources, not from abroad. If you want some good outcome, this is what you have to do. A lot of this is just arithmetic and sensible economics. (Some of the arithmetic is unpleasant—that is one reason they call ours “the dismal science”.) The package of IMF policies is coherent and makes sense.

IMF Survey: What is the most interesting thing you have learned from your work?

Sargent: To me, one of the most fascinating things is how the U.S. Congress and Treasury recognized and managed rollover risks and interest rate risks; and how they thought about the sources of the fundamentals that drove interest rate risk, some under the government’s control, some not. Many of their discussions and decision seem very wise and modern. The government did various things about rescheduling and issuing callable debt and exercising call options. It was quite a sophisticated operation, done 150 years ago. We are trying to understand: (1) were those good things to do; and (2) what motivated those decisions.

IMF Survey: What’s next for your research?

Sargent: Debt limits are just a part of what we are doing. We are digging deeper and trying to find interesting stories behind individual episodes. Then, we hope to tell some convincing stories—and supplement them with sensible analysis.

The interview below is from the IMF Survey. Also, see my interviews with Thomas Sargent in 2002, 2012, and a recap in 2015 after Sargent winning the Nobel-Prize.

In a recent visit to the IMF, Nobel Laureate Thomas Sargent brought to life the economic and financial history of the United States, with stories of how debt limits have evolved over the years before and since the creation of the Bretton Woods Institutions. Read the full article…

Posted by at 10:21 PM

Labels: Profiles of Economists

Wednesday, December 23, 2015

Understanding China’s Housing Market

For several years, analysts have been expressing concerns about China’s housing market. “Boom to bust: China’s property bubble is about to burst”—this was the headline of an article in the Economist magazine in 2008. Fast forward a few years and we continue to see similar headlines. “Haunted housing: Even big developers and state-owned newspapers are beginning to express fears of a property bubble”, in 2013. “End of the golden era: China’s property market is cooling off, at long last”, in 2014. These days, together with the housing market, analysts are also expressing concerns about the overall health of the Chinese economy. Here is one headline from 2015: “Coming down to earth: Chinese growth is losing altitude. Will it be a soft or hard landing?”

So why China’s housing market has not seen a bust yet? At last weekend’s conference in Shenzhen on December 18-19, leading experts on China’s housing market provided some answers. The conference—International Symposium on Housing and Financial Stability in China—was organized by the Chinese University of Hong Kong in Shenzhen, International Monetary Fund, and Princeton University.

Getting the facts right: housing and mortgage market

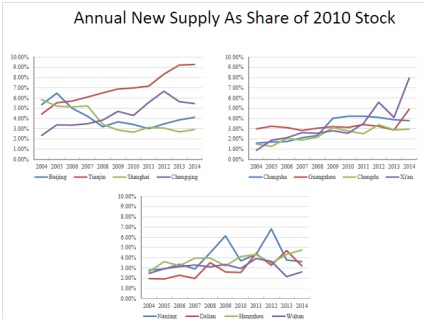

New research by Joe Gyourko (University of Pennsylvania) and his co-authors provides facts on China’s housing market from a supply and demand perspective. “In China, different housing markets behave very differently. A boom in Beijing and Shenzhen doesn’t mean a boom everywhere”, Gyourko said at the conference.

In his presentation, Gyourko made two key points. First point: there is substantial heterogeneity across cities in the balance between housing supply and demand. At one end, housing supply has outpaced demand in the interior part of the country. Specifically, housing supply has outpaced demand by at least 30 percent in twelve major markets and by 10 to 29 percent in another eight markets. On the other end, housing demand has outpaced supply in most major eastern markets. These include: Beijing, Hangzhou, Shanghai, and Shenzhen. Second point: markets such as Beijing, despite their strong measured fundamentals, should be considered somewhat risky because homes there trade at very high multiples of rent.

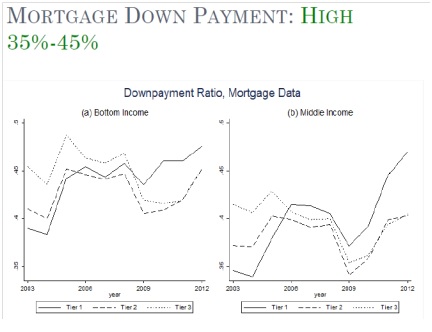

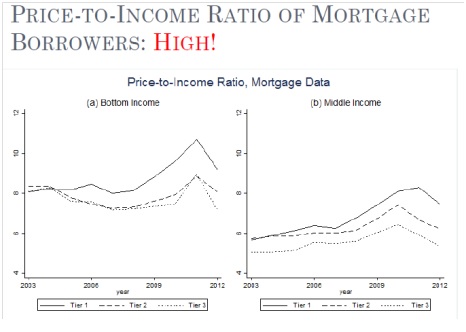

Another new piece of research, by Hanming Fang (University of Pennsylvania) and his co-authors, provides facts on China’s housing market from the mortgage market perspective. They have constructed a set of house price indices for 120 major cities in China and used a comprehensive data set of mortgage loans from 2003 to 2013. In his presentation, Fang showed that the Chinese housing boom has been accompanied by strong growth in income, and high mortgage down payments. For a decade, household’s disposable income has had an average annual real growth of 9 percent at the national level. Also, down payments have been over 30 percent on all mortgage loans.

However, Fang noted that the participation of low-income home buyers in the housing boom has been characterized by high price-to-income ratios. The ratios are around eight in second and third tier cities, and even ten in first tier cities.

Haizhou Huang (CICC) provided very interesting facts on China’s housing market from the perspective of population in big cities. Huang pointed out that population concentrates into big cities. For example, in Japan and the United States, an increase in urbanization was accompanied by an increase in population concentration in big cities. So Huang expects that population concentration in China’s big cities will continue to rise. This could lead to more pressure on the housing market in Tier 1 cities. Huang asks: “Should China follow the European or Japanese model of few cities that have a large amount of the population?” China needs to develop more megacities, in his view. This could imply that the housing market could continue to grow and pressure in the housing market in tier I cities could decrease in the future.

Xiaobo Zhang (Peking University) talked the impact on China’s housing market from cultural traditions. “In rural areas of China, a new home is a necessary condition for marriage”, says Zhang. This is due in part by the sex ratio imbalance in China. Zhang showed that in 2000, 1 in 14 males could not marry. And in 2005, it was 1 in 10.

Assessing the risks: the role of expectations and local government debt

One area of risk is the role of expectations. Fang and Gyourko said that risks in Chinese housing market could arise with a shift in expectations. Specifically, Fang said that the willingness of low-income homebuyers to endure high price-to-income rations is explained by expectation of continued growth in income. However, the high expectation of future income growth may not be sustainable. Likewise, Gyourko said that a modest downward shift in expectations could generate sharp decline in house prices.

Moreover, Richard Koss (Global Housing Watch Initiative) compared how expectations have played an important role in the housing market in China and the United States. In both countries, expectations have played a role, but in different ways. Koss said that in the United States, expectations played a role in terms of house prices (e.g. expectations that house prices would continue rising), while in China, expectations play a role in terms of income growth (e.g. expectations that income will continue rising).

In the United States, said Koss, “No one thought house prices could fall as they never had on a nationwide basis, although specific regions suffered declines in the past. Americans thought they were special and that financial innovation would minimize risks but that turned out to be completely wrong.” So, in China, there could be risks in terms of irrational expectations of income growth.

Another area of risk is the local government debt and its linkage with the housing market. A new paper by Yongheng Deng (National University of Singapore) and his co-authors explores this link. At the conference, Deng noted that unlike local governments in western countries, local Chinese governments are prevented from directly issuing debt to fund mandated capital projects. Therefore, local governments tap into the growing housing market by selling public land to rise funding.

More specifically, future land sales revenue are used to repay the local government’s debt and land parcels are the most widely-used collateral for local government debt. This implies that “a substantial drop in housing or land prices may increase the risk level of local government debt, or even trigger a systematic default”, said Deng.

From the Global Housing Watch Newsletter: December 2015

For several years, analysts have been expressing concerns about China’s housing market. “Boom to bust: China’s property bubble is about to burst”—this was the headline of an article in the Economist magazine in 2008. Fast forward a few years and we continue to see similar headlines. “Haunted housing: Even big developers and state-owned newspapers are beginning to express fears of a property bubble”,

Posted by at 4:46 PM

Labels: Global Housing Watch

Wednesday, December 9, 2015

Housing Market in Kuwait

On the policy front, the report says that “Macroprudential tools can help mitigate potential risks posed by banks’ high exposures to the real estate sector. It is important to ensure that macroprudential policies are reviewed constantly to ensure that they do not exacerbate any property price correction, while preempting the buildup of excessive risks related to real estate exposures. (…) House price growth is a core indicator to monitor and the authorities should construct indices for residential properties as well as commercial properties. Also, other indicators, such as both the average and distribution of the LTV and DSTI (DSC) ratio, should be collected and analyzed to adjust macroprudential policy measures properly and swiftly.”

“Prices have shown some signs of softening (…) As of July 2015, prices across the residential and investment property segments have seen average prices fall in year-on-year terms by 6 and 7 percent, respectively (…). As residential prices began to fall in the first half of 2014, average investment property prices began increasing, rising by some 71 percent between March and September. After peaking in September 2014, average investment property prices have fallen by approximately 32 percent as of July 2015. Read the full article…

Posted by at 10:00 AM

Labels: Global Housing Watch

Monday, December 7, 2015

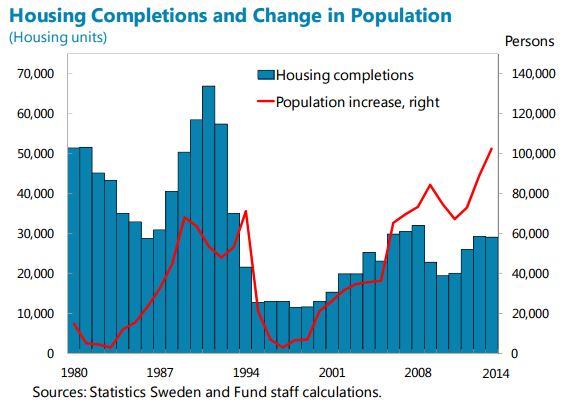

Sweden’s Housing Market

In terms of policies, the report recommends that:

- “Housing supply should be enhanced through land sale and planning reforms, which will also facilitate more competition in residential construction. Rent controls should be eliminated on new rental apartments and phased out more broadly.”

- “Mortgage interest deductibility should be phased out to moderate housing demand over time and limits on capital gains tax deferrals raised to release pent up supply.”

- “A debt-to-income limit should be adopted to contain rises in the already sizable share of highly indebted households, which adds to macroeconomic vulnerabilities.”

A separate IMF report looks at the role of supply constraints in driving prices of owner-occupied housing using municipal-level data.

“The housing market shows imbalances, with double-digit price gains as the urban population outpaces construction, pushing up household debt from already high levels. Dwelling price rises accelerated to 16 percent y/y in September, led by apartment price increases exceeding 20 percent in Stockholm and Gothenburg. Housing supply is constrained by construction impediments and rent controls while demand is bolstered by population growth and urbanization, rising income and financial savings, and historically low interest rates. Households need to borrow more at higher house prices, Read the full article…

Posted by at 10:00 AM

Labels: Global Housing Watch

Subscribe to: Posts