Thursday, August 27, 2015

Behind the commodities bust

First was the dot-com bubble, then the housing bubble. Now comes the commodities bubble. We don’t fully understand the stock market’s current turmoil, but we know it’s driven at least in part by a bubble of raw material prices. Their collapse weighs on world stock markets through fears of slower economic growth and large financial losses.

All bubbles share similar characteristics. There’s a strong, enthusiastic demand for some object (whether stocks, homes, oil or tulips). High demand pushes up prices, which inspires more demand. Prices ultimately reach unsustainable levels so that when spending slows, the bubble implodes. Commodities have now traced this familiar path.

As the Economist reminds us, raw material prices respond to different influences. Weather affects crops; technology (a.k.a. “fracking”) affects oil recovery. Still, despite these variations, prices of many commodities — not just oil — have followed roughly similar trajectories in recent years. They have dropped steeply, according to figures from the International Monetary Fund.

Here are declines for five commodities from 2012 through July 2015: oil, down 48 percent; iron ore, 60 percent; copper, 31 percent; palm oil, 39 percent; and wheat, 37 percent. Many commodity prices have continued to fall.

The bubble formed on hopes that China’s rapid growth would feed an ever-expanding appetite for raw materials, says economist John Mothersole of the consulting firm IHS Global Insight. Demand and prices would remain high indefinitely. Although prices fell after the 2008-09 financial crisis, China’s huge “stimulus” package — intended to offset the crisis’s drag — sent them up again, says Mothersole. China’s demand seemed destined to stay strong, as economic growth would stabilize at a high level.

It didn’t. In 2010, China’s economy grew 10 percent; the IMF expects 6.8 percent in 2015 and 6.3 percent in 2016. Other economists think growth could be lower. As a result, much of the added production capacity — mines and the like — to supply China isn’t needed. “There’s a new commodities era,” says economist Rabah Arezki, head of the IMF’s commodities research. “Everyone was rushing to invest. Now they have to adjust to a new lower level of demand.”

Continue reading here.

|

| Workers carry pipes to install an irrigation line in a coffee farm in Santo Antonio do Jardim, Brazil, last year. (Paulo Whitaker/Reuters) |

By Bob Samuelson [The Washington Post]:

First was the dot-com bubble, then the housing bubble. Now comes the commodities bubble. We don’t fully understand the stock market’s current turmoil, but we know it’s driven at least in part by a bubble of raw material prices. Their collapse weighs on world stock markets through fears of slower economic growth and large financial losses.

All bubbles share similar characteristics. There’s a strong,

Posted by at 4:27 AM

Labels: Energy & Climate Change

Friday, August 21, 2015

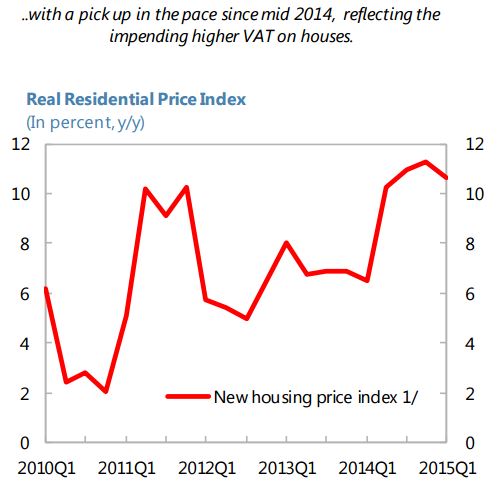

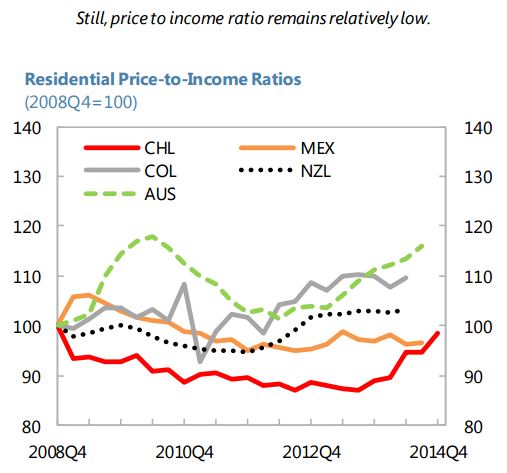

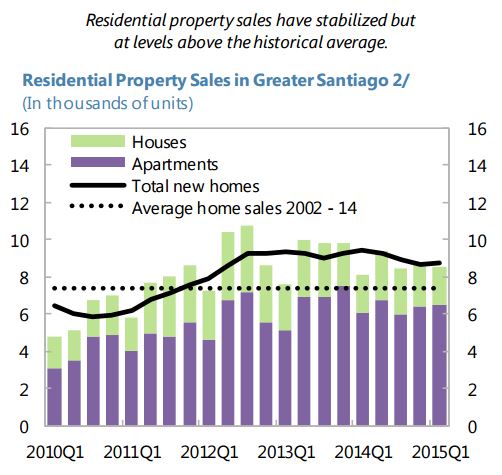

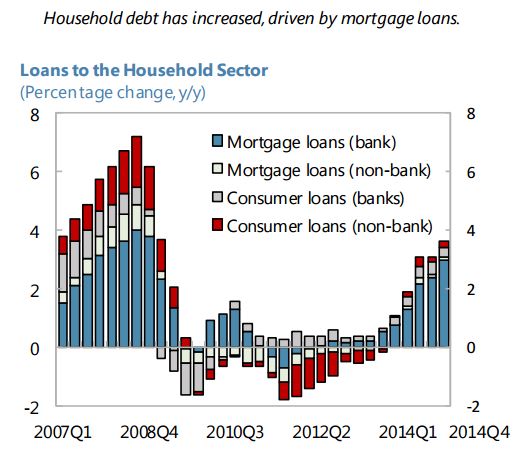

Chile’s Housing Market

Posted by at 9:00 AM

Labels: Global Housing Watch

Wednesday, August 19, 2015

Spain’s Housing Market

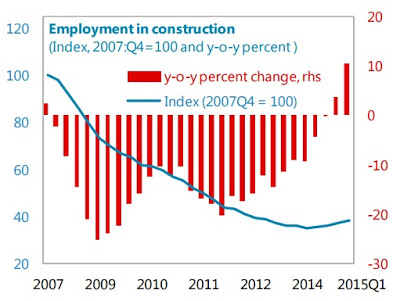

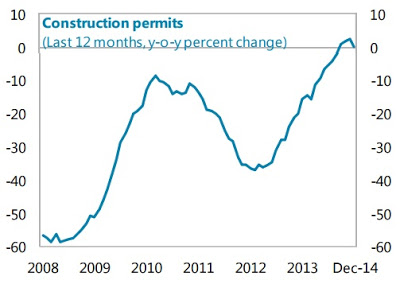

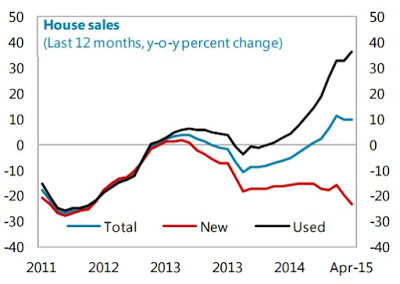

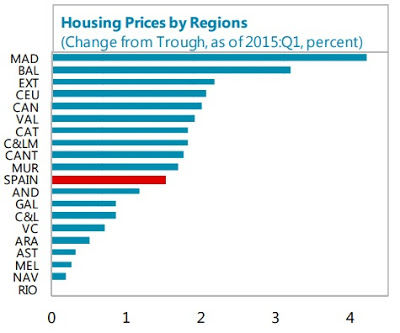

The Spanish housing sector appears to have bottomed out, says the IMF’s new report on Spain. The report notes that the construction activity has started to recover, mostly driven by the non-residential sector. Moreover, construction permits have stopped falling and house sales are picking up. And housing prices started to increase slightly, albeit unevenly across regions.

Below are six charts that show the developments in the housing market in Spain.

Posted by at 9:00 AM

Labels: Global Housing Watch

Monday, August 17, 2015

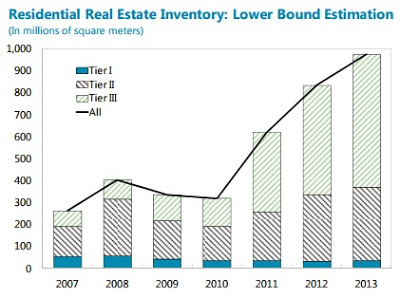

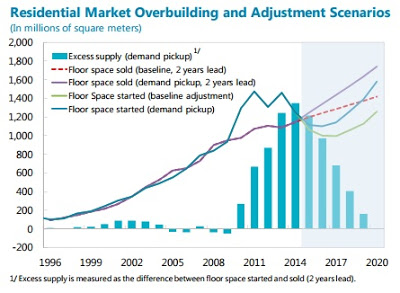

China: How Big Is the Risk of a Real Estate Slowdown and Does It Matter?

How big is the risk of a real estate slowdown? The report says:

“All indicators point to weakness in China’s housing market. Housing prices have been moderating both at the national level and across all city tiers, with the weakest performance among the smaller cities. (…) Housing inventory ratio—floor space unsold to floor space sold—shows a buildup since 2013, suggesting oversupply. Even though there is uncertainty regarding the level (National Bureau of Statistics (NBS) data show inventory of four months, while data from local housing bureaus suggest higher than two years), the direction of the buildup is clear. Inventory is especially high in Tier 3 and Tier 4 cities.”

Does it matter? The report says:

“Continued adjustment in floor space starts is warranted to let demand catch up with supply. (…) The adjustment will have significant impact on GDP growth. Given the estimated relationship between growth in floor space starts and in real estate gross fixed capital formation (GFCF), real estate GFCF could slow to -2 to -4 percent in 2015 from about 3 percent in 2014. As real estate GFCF accounts for about 9 percent of GDP, this would imply a drop of GDP growth by about ½ percentage point in the baseline scenario. This abstracts from the indirect effect arising from real estate linkages to upstream and downstream sectors. Some of these sectors suffer from oversupply, and a slowdown in construction activity could bring losses, exposing vulnerabilities and posing risks (…).”

“China’s housing market has softened visibly since 2014, reflecting oversupply in most cities. More adjustment is likely”, says the IMF’s latest report.

How big is the risk of a real estate slowdown? The report says:

“All indicators point to weakness in China’s housing market. Housing prices have been moderating both at the national level and across all city tiers, with the weakest performance among the smaller cities. (…) Housing inventory ratio—floor space unsold to floor space sold—shows a buildup since 2013,

Posted by at 9:00 AM

Labels: Global Housing Watch

Friday, August 14, 2015

Johan Norberg: India Awakes

At an event at Cato, Norberg said that “India is waking up because the government is starting to take a nap every now and then (imposing fewer regulations)”.

“What you can do and at what price matters more than who you are or what caste,” said Norberg.

“It’s morning in India but that is when the work day begins.”

India has set the goal of being in the top 50 countries in the World Bank’s Doing Business Index. Today it is at number 142 out of 189 countries.

A lesser known fact about Norberg is that he helped me inaugurate the IMF’s Book Forum: the topic was “Capitalism and its Critics”. The transcript makes for very interesting and prescient reading today – all the speakers (Jerry Muller, Ann Florini and Norberg) brought their ‘A’ game. For a short summary of the event click here.

Since 1991, 250 million people have been lifted out of poverty in India. Johan Norberg’s documentary India Awakes discusses how this happened.

It used to be said that Indians succeeded everywhere except in India. Now Indians are starting to succeed in India.

At an event at Cato, Norberg said that “India is waking up because the government is starting to take a nap every now and then (imposing fewer regulations)”.

“What you can do and at what price matters more than who you are or what caste,”

Posted by at 5:50 PM

Labels: Profiles of Economists

Subscribe to: Posts