Tuesday, June 30, 2015

Latest Work on Macroprudential Policy

Since the Great Recession, there has been a lot of research done on macroprudential policy. Here is the new research of the past month:

Macruprudential policy in country-specific cases: A new IMF paper reviews the use of macroprudential policy in Hong Kong SAR, the Netherlands, New Zealand, Singapore, and Sweden. The analysis shows that each country reviewed adopted an institutional framework for macroprudential policy suited to their own circumstances. The evidence reviewed confirms that “one size does not fit all,” and that it is possible to conduct macroprudential policy with a heterogenous set of institutional frameworks. In all cases, most of the macroprudential tools used were directed at containing risks arising from a booming housing market (for e.g., LTV and DSTI ratio limits). This study complements an earlier note issued by the IMF, which provides a framework for staff’s advice on macroprudential policy in its bilateral surveillance.

Macroprudential policy in Asia and Pacific: A new working paper from the Bank for International Settlements (BIS) finds that macroprudential policies are more successful when they complement monetary policy by reinforcing monetary tightening, than when they act in opposite directions (on a related note, see Box IV.A of the latest BIS annual report).

Macroprudential policy in Europe: A new paper from the European Central Bank (ECB) says that policies need to be granular enough to deal with the fact that property credit cycles can exhibit strong regional features. There is increasing theoretical support and empirical evidence that borrower-based regulatory policies can be effective, diminishing the credibility of claims that there is not enough experience to practically apply such instruments. In the case of the euro area there may be room in a significant number of countries for putting these instruments more clearly in the hands of newly created macroprudential policy authorities and for creating coordination mechanisms for national LTV or DTI policies at the area-wide level to address the cross-border spillovers potentially caused by these policies.

Experience with macroprudential policy: Research by Kenneth N. Kuttner (Williams College) and Ilhyock Shim (BIS) concurs with the work of others who say that experience with macro-prudential policy measures in various countries is not extensive and may, in any case, have only limited applicability elsewhere because of differences in economic conditions, the relative importance of capital market and traditional bank intermediation, and many other factors. Therefore, it would be unwise to rely solely on macroprodudential policies for taming financial booms and busts.

Riksbank macroprudential conference: The Riksbank has started to hold an annual conference for frontier thinking on macroprudential policies. The keynote speaker at this year’s conference was Raghuram Rajan, Governor of the Reserve Bank of India. It also included presentations from: Jeremy Stein of Harvard University, Atif Mian of Princeton University, Gianni De Nicolò of the IMF and others.

From the Global Housing Watch Newsletter: June 2015

Since the Great Recession, there has been a lot of research done on macroprudential policy. Here is the new research of the past month:

Macruprudential policy in country-specific cases: A new IMF paper reviews the use of macroprudential policy in Hong Kong SAR, the Netherlands, New Zealand, Singapore, and Sweden. The analysis shows that each country reviewed adopted an institutional framework for macroprudential policy suited to their own circumstances.

Posted by at 12:50 PM

Labels: Global Housing Watch

Monday, June 29, 2015

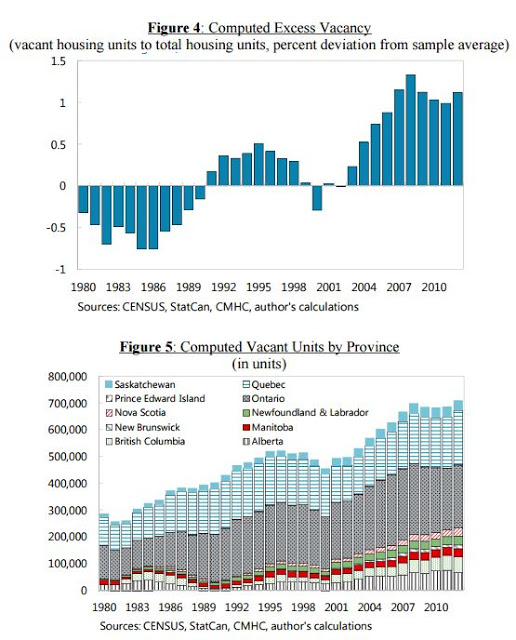

Housing Supply in Canada

A new IMF working paper sheds “new light on the supply of housing units in Canada. It contributes to the existing literature by (i) providing yearly estimates of housing stock and household formation for the 10 Canadian provinces over the period 1980-2013, (ii) and by estimating excess supply in housing units for the ten Canadian provinces. The empirical results suggest that the Canadian housing market was in excess supply by about 0.5 percent of the total housing stock by end 2013. Read the full article…

Posted by at 8:50 PM

Labels: Global Housing Watch

Thursday, June 25, 2015

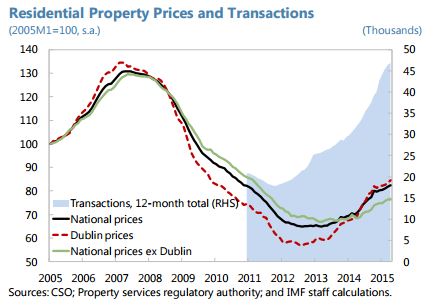

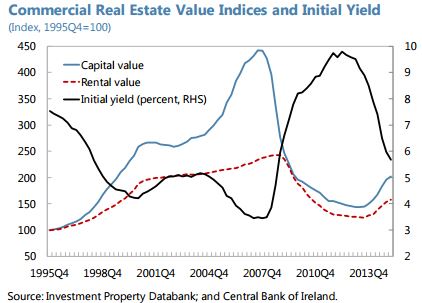

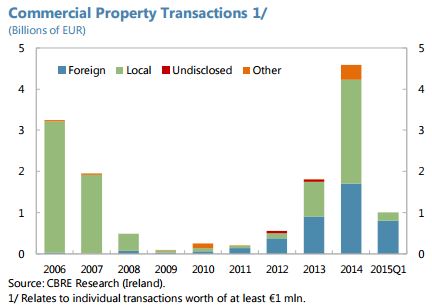

House Prices in Ireland

“The share of mortgages on primary dwellings in arrears continues to decline, except for arrears over 720 days. The residential property market is reviving, particularly in Dublin, with some price deceleration in recent months. Commercial property prices and rents rose sharply from a low base in 2014 and transactions rose strongly in 2014 with over one-third by non-residents, and further inflows in Q1,” notes the latest IMF report on Ireland.

Posted by at 2:56 PM

Labels: Global Housing Watch

Friday, June 19, 2015

Fiscal Forecasting Follies: Private Sector vs. Government

Government forecasts of budget deficits invoke considerable skepticism. A prominent critic is Jeff Frankel who mocks the ‘‘budgetary wishful thinking’’ of many government agencies. Frankel notes that during the 2000s, the U.S. Office of Management and Budget ‘‘turned out optimistic forecasts’’ for eight years in a row; likewise, in 2000, the Greek government projected that its budget deficits would shrink below 2 percent of GDP within a year, a far cry from the outcome of 4–5 percent of GDP. Read the full article…

Posted by at 2:44 PM

Labels: Forecasting Forum

Wednesday, June 10, 2015

Housing Finance and Real-Estate Booms: A Cross-Country Perspective

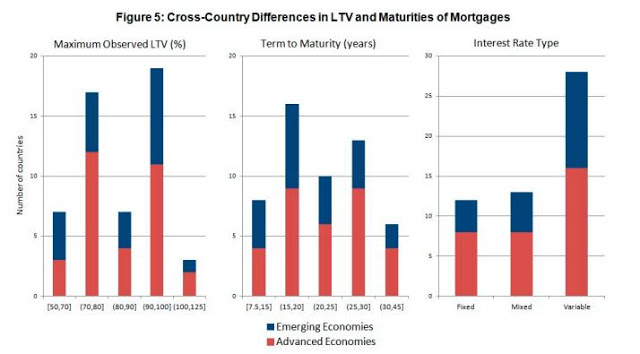

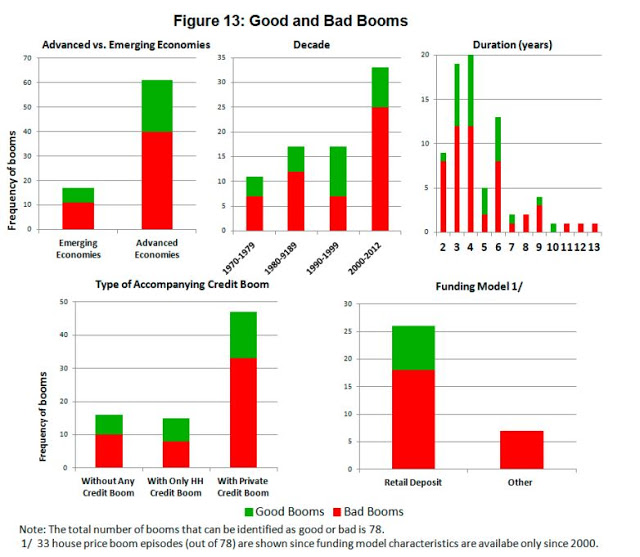

A new IMF paper “analyzes the conflict between the objective of increasing access to housing finance and the dangers associated with fast-growing housing credit. [The paper finds the following:] First, housing finance characteristics vary widely across countries, and several characteristics are correlated with the relative depth of mortgage markets. (…) Second, some of the housing finance characteristics associated with deeper mortgage markets are also associated with increased risks of crisis. (…) Third, in this context, both advanced and emerging markets should avoid relaxing house financing standards in order to achieve deeper mortgage markets, Read the full article…

Posted by at 5:43 PM

Labels: Global Housing Watch

Subscribe to: Posts