Saturday, May 30, 2015

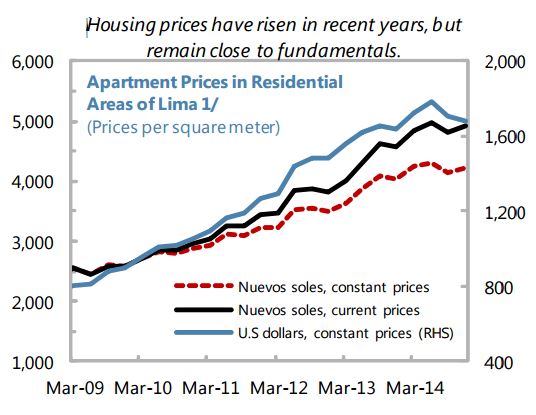

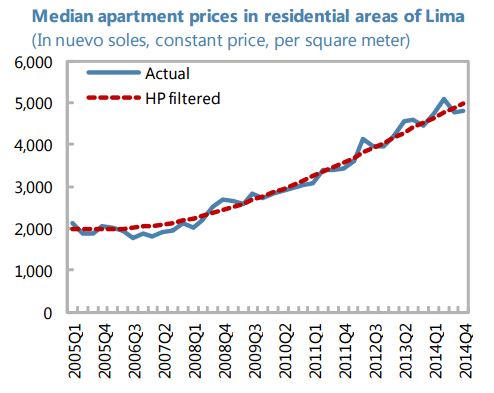

House Prices in Peru

“There are no signs of asset price bubbles. (…) Housing prices continued to increase, but there is no evidence of misalignment from the trend average and the housing price-to-rent ratio was 15 percent―one of the lowest in the region,” according to IMF’s latest report on Peru.

Posted by at 6:34 PM

Labels: Global Housing Watch

House Prices in Switzerland

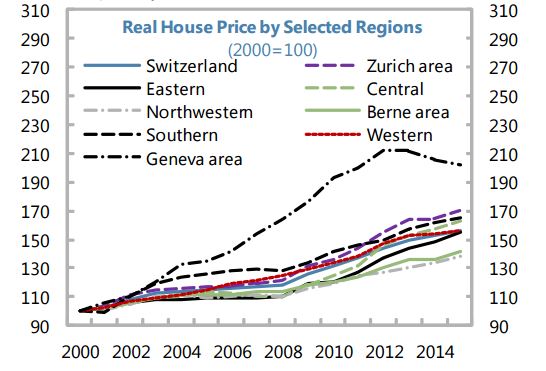

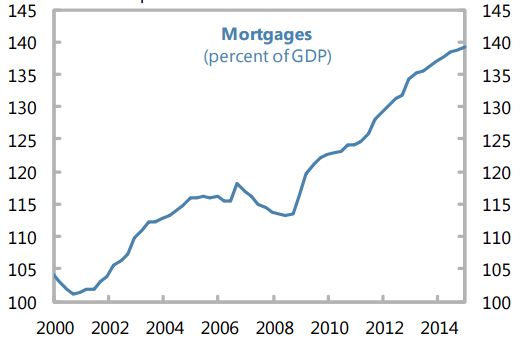

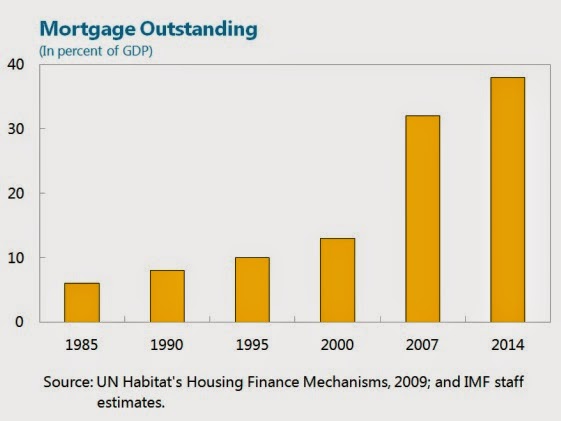

On the measures taken by the Swiss authorities, the report points out that the “(…) Swiss authorities have undertaken various prudential measures over the last three years aimed at reducing housing-related risks. Swiss household debt (mainly mortgages) is high by international standards, and mortgage debt has been rising steadily since 2008, in tandem with a buoyant housing market (…). To reduce related financial stability risks, the authorities have undertaken a number of prudential measures, including strengthened bank “self-regulation” standards approved by FINMA, effective September 2014 (…). These measures appear to have had some effect, as housing and mortgage markets show some signs of cooling. The growth rate of residential real estate prices has eased both for owner-occupied apartments and single family houses, including in areas, such as Lake Geneva, that previously saw rapid house price growth (…). Mortgage growth has also decelerated, although this effect is less pronounced (…). Similarly, price-to-rent and price-to-income ratios have started to stabilize (…). The percent of new mortgages for owner-occupied real estate with loan-to-value ratios exceeding 80 percent have also been on a declining trend. As the authorities have taken a range of measures to address the risk of a build-up of imbalances in the housing and mortgage markets, it is difficult to clearly disentangle which have been the most effective. However, the consensus view among the authorities and banks was that the required down payment from the borrower’s own funds (not funded by using pension savings) has perhaps been the most important measure.”

“Though it has cooled recently, Switzerland’s house prices have had a rapid run-up over the last decade, and mortgage debt is high as percent of GDP (…). The economy could thus be vulnerable to a sharp decline in house prices, which would weaken household balance sheets and impede growth. Such a decline would also adversely affect the banking and insurance industries, with their large respective exposures to the mortgage market and real estate,” says the new IMF report on Switzerland. Read the full article…

Posted by at 6:23 PM

Labels: Global Housing Watch

Tuesday, May 26, 2015

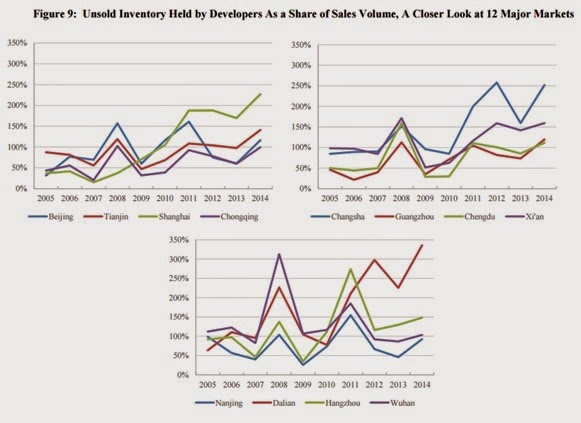

China’s Housing Market

Picture this: “(…) in 1972, only 17% of the 862 million Chinese lived in urban areas and the entire stock of housing was state owned. Today, more than half of China’s 1.4 billion residents live in cities, while 9 out of 10 households own their homes. Unsurprisingly, this housing revolution has brought with it a property price boom,” (Money & Banking). These developments have led many experts to debate whether there is a housing bubble or not? What are the risks and the likely impact? For example, the New York University Stern School of Business recently hosted a conference that brought together the world’s leading experts on China’s real estate markets for an in-depth discussion. The bullet points below summarize the latest research and developments on China’s housing market.

What are the housing demand and supply indicators saying? A new IMF research confirms that there is a nationwide slowdown in China’s housing market since 2014. In contrast to the slowdown in 2012, there is no tightening of policies directed at property market. This time, the slowdown reflects overbuilding across many cities, in particular in Tier III and IV cities and in the northeast region. “Using different adjustment scenarios, the paper highlights that the adjustment is likely to be a multiyear process with implications for investment and growth. Under reasonable assumptions, real estate investment growth in 2015, could, for example, be negative,” according to IMF research.

Another research by Yongheng Deng (National University of Singapore), Joe Gyourko (University of Pennsylvania), and Jing Wu (Tsinghua University) looks into the housing demand and supply conditions in China. The paper finds the following: first, “(…) there is substantial heterogeneity in supply-demand imbalances across markets, both over time and in the shorter run; [second,] (…) there are a number (much more than a handful) of markets, primarily off the coast, where oversupply looks to be substantial by one or more measures; even absent a negative economic shock, these markets look very risky (…); [third,] even markets such as Beijing with strong measured fundamentals should be considered risky because homes there trade at very high multiples of rent; (…).”

However, the latest figures on housing sales from April show that there are signs of a turnaround in the Chinese housing market (Wall Street Journal and New York Times). Also, an analysis from the Financial Times says that “empty units may be less of an obstacle to short-term recovery than many think.” In contrast, an article from Seeking Alpha questions whether China’s housing market is recovering. To what extent the housing recovery is here to stay or it is just a blip, remains uncertain.

What are the mortgage indicators saying? Research by Hanming Fang (University of Pennsylvania), Quanlin Gu (Peking University), Wei Xiong (Princeton University), and Li-An Zhou (Peking University) analyze the characteristics of mortgage borrowers. They find the following: “On the comforting side, the rapid income growth, which accompanied the enormous housing price appreciation, helped support the steady participation by low-income households in the housing market. On the concerning side, high expectations about future income growth might have motivated low-income households to buy homes by undertaking substantial financial burdens [price-to-income ratios over eight to buy homes], causing them to be particularly vulnerable to future sudden stops in the Chinese economy.” On a related note, a new article from Seeking Alpha points out that exposure to real estate is high and that bad loans are increasing in China.

From the Global Housing Watch Newsletter: May 2015 Issue

Picture this: “(…) in 1972, only 17% of the 862 million Chinese lived in urban areas and the entire stock of housing was state owned. Today, more than half of China’s 1.4 billion residents live in cities, while 9 out of 10 households own their homes. Unsurprisingly, this housing revolution has brought with it a property price boom,” (Money &

Posted by at 6:59 PM

Labels: Global Housing Watch

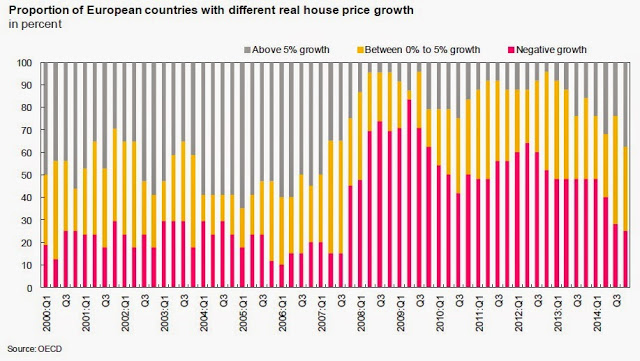

Europe’s Housing Market

The performance of the European housing market remains mixed. In Europe, house prices are rising in some countries and falling in others. Moreover, even though the number of transactions is recovering, housing supply indicators remain in the doldrums. There is also an issue of housing affordability. The bullet points below gives a summary of these developments.

House price developments. Europe was the weakest-performing world region in 2014, with house prices rising on average by 1.6 percent, says Knight Frank. Similarly, Global Property Guide notes that “Europe’s property markets are surging ahead [(…) However,] some parts of Europe continue to struggle. Seven of the 22 European housing markets included in our global survey saw house price falls in 2014.” This mixed performance in the housing market reflects the divergent economic performance in Europe, according to Scotiabank. However, the momentum in house prices could be shifting. The graph below shows that the proportion of European countries with negative real house price growth has been on a downward trend since the last three quarters of 2014.

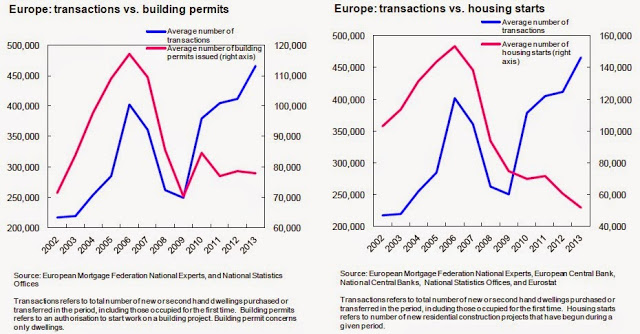

Housing supply developments. “The continued recovery in housing starts, relative to a period considered normal [2002], is not isolated to the United States, says Michael Neal of the National Association of Home Builders. Indeed, a review of Europe’s mortgage and housing market shows that housing supply indicators are continuing to shrink (EMF Hypostat 2014). The report notes that “Data for 2012 and 2013 shows a continued contraction in the [housing supply] market, which still is not feeling the positive effect of a pick-up in mortgage activity in many EU countries. This mainly reflects the existence of an overhang in the housing market in terms of unsold units, which therefore makes new construction unnecessary at the moment. It is likely that construction will pick up again in the coming months and years, though it is uncertain when (and whether) it will return to pre-crisis levels in Europe.”

Affordability. The issue of housing affordability has been discussed in many countries. In Europe, there are more people without a home today than six years ago, and there are not enough affordable homes available in most European countries to meet the increasing demand; these are two emerging issues from a new report that looks at the state of the housing market in the Europe (Housing Europe).

From the Global Housing Watch Newsletter: May 2015 Issue

The performance of the European housing market remains mixed. In Europe, house prices are rising in some countries and falling in others. Moreover, even though the number of transactions is recovering, housing supply indicators remain in the doldrums. There is also an issue of housing affordability. The bullet points below gives a summary of these developments.

House price developments. Europe was the weakest-performing world region in 2014,

Posted by at 6:57 PM

Labels: Global Housing Watch

Monday, May 25, 2015

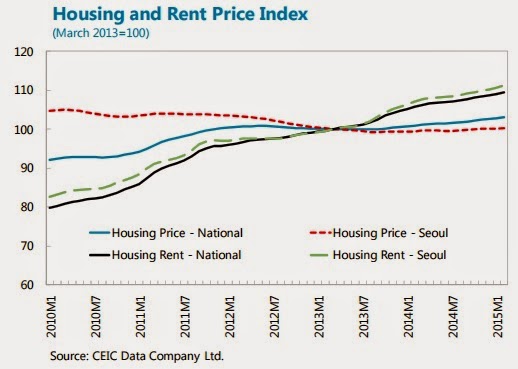

House Prices in Korea

On housing finance, the report says that “at the same time the structure of household debt could be strengthened. Reflecting Korea’s relatively young and rapidly growing mortgage market (…), a large share of houses are financed short-term either in the form of chonsei rental deposits or the rolling over of floating-rate interest-only mortgage loans with short maturities and bullet repayments. One key challenge will be to facilitate the transition by households and financial institutions toward a more stable, long-term structure (…).”

“Measures to try to revive a housing market that has been in a multi-year slump including legislation to unwind major regulatory roadblocks for housing reconstruction projects which had been previously introduced to curb house price inflation and speculative demand. In the wake of these measures, together with some unwinding of the earlier tightening of mortgage lending restrictions (…), there have been some preliminary signs of a pickup in house prices and transactions volumes,” says the latest IMF report on Korea. Read the full article…

Posted by at 4:33 AM

Labels: Global Housing Watch

Subscribe to: Posts