Monday, April 27, 2015

Current State of House Prices Across the Globe

Even though real house prices are rising in many countries, the global housing recovery remains on a two-speed pattern: in some countries, house prices have rebounded, while in others, they are still recovering. The bullet points below give a summary on experts’ views on current house price developments, policy response, short and long term outlook, and potential risks.

- Current house price developments. Global Property Guide gives a positive view of the global house price developments. It notes that global house prices continue to boom with real house prices rising in 31 out of 41 countries. Similarly, the latest update from the Economist shows that real house prices are rising in 19 out of 26 countries. The Economist notes that “Although the nuances of each market are many and varied, a single unifying theme is the cheapness of borrowing (…).”

- Policy response. Scotiabank says that the “uneven global performance is prompting divergent policy responses. Policymakers in a number of countries have recently tightened macro-prudential rules (UK, Ireland, Sweden) and/or foreign purchase restrictions (Australia), as the persistence of ultra-low borrowing costs heightens concerns of overheating. Others are easing lending restrictions to bolster housing demand (China, Korea). Spain recently enhanced its purchase incentives targeted to non-EU buyers.”

- Short and long term outlook. On the outlook for this year, Knight Frank says that the performance of the global housing market will depend on two monetary policy decisions: (1) the extent to which the ECB’s new QE programme will stimulate the Eurozone’s housing markets and (2) the timing of the US Federal Reserve’s rate rise. On the long term outlook, an article from the Financial Times asks: “The best real estate investment in the world today? Beachfront huts in Somalia. (…) The explanation lies in demographics. All of the world’s forecast 3bn population growth through to 2100 will be urban, [Hans Rosling—a Swedish public health professor] points out; a third will be in Asia, while two-thirds will be in Africa. In economic terms the developed west will grow at 1 to 2 per cent a year through until 2100, while the rest of the world will grow at 4 to 6 per cent. This amounts to a startling global shift in the pattern of trade.”

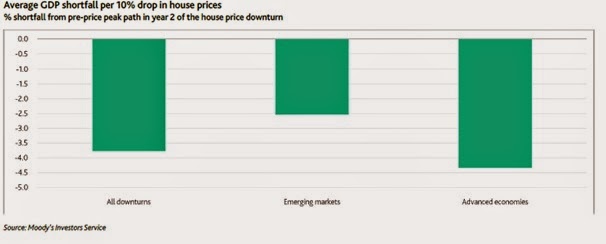

- The risk of a raise in interest rates. On the risks to emerging markets, “In some parts of the emerging world, housing markets have grown well ahead of income in recent years. US interest rates are about to rise, and international capital will revert to the center, seeking higher and safer yields. This will bring about an earthquake in housing markets at the periphery of the global financial system,” according to Alessandro Rebucci (Johns Hopkins University). Also, an article from Bloomberg notes that “Experience shows that when the Fed has embarked on significant rate hiking campaigns, there are global repercussions.” Separately, a new analysis from Moody’s says that the eventual rise in interest rates, and an economic slowdown with an increase in unemployment could prompt corrections in housing markets. In this context, Moody’s studied declines in real house prices since 1973 and how it affects GDP. In 50 episodes of real house price declines, Moody’s finds that house price corrections coincide with a GDP shortfall of around 6 percent and this shortfall is larger in advanced economies compared to emerging economies. This is in line with the view that wealth effects are bigger in advanced economies and lower in emerging economies.

- Housing affordability crisis. “New risks as young Londoners priced out of housing market (…) The problem has become a hot issue in national elections due next month.” writes Reuters. The issue of housing affordability is also being talked about in other parts of the world. For example, housing affordability was one of the most talked-about subjects at this year’s American Planning Association’s annual National Planning Conference (Citylab). Moreover, in an excellent article, Kate Allen of the Financial Times says that we need to ensure that the lowest paid workers are not forced out of the cities. “Spiralling living costs and poor housing conditions are pushing much-needed workers out of these cities — and inequality is rising (…) A dazzling array of policy options [demand controls, supply controls, remove the market, remove spatial restrictions, encourage renting, build elsewhere, and subsidize ownership] has emerged in recent years as employers and city authorities worldwide attempt to stem the tide — none is a complete answer in itself; all have pros and cons,” according to Allen.

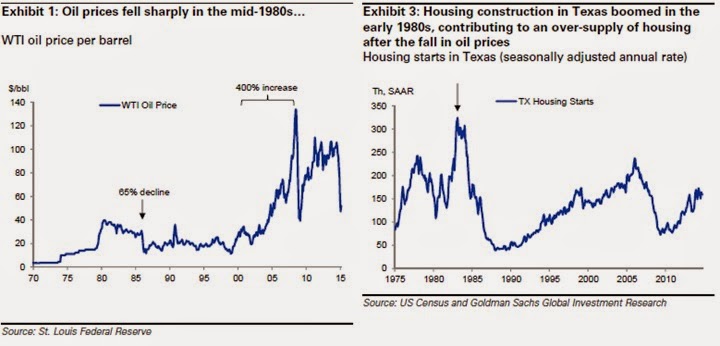

- The risk of persistently low oil prices. So far, the decline in oil prices has had no major impact on the housing market. However, it “(…) will impact housing values over the next 15-24 months, but the effect varies geographically” according to Chris Stroud (HouseCanary). Stroud notes that while some markets positively correlate and have a dampening effect on home prices (e.g. Houston), others negatively correlate and can be stimulated by falling oil prices (e.g. Detroit). This view is also shared by Jed Kolko, who says that in oil producing markets, home prices tend to follow oil prices, but it typically takes two years for oil prices to fully affect home prices in those markets. “For instance, in the 1980s, the largest year-over-year oil price declines were in early- and mid-1986. In Houston, job losses were steepest in late 1986. But home prices didn’t slide most until the third quarter of 1987. Since 1980, employment in oil-producing markets has followed oil-price movements roughly two quarters later and home prices have followed oil-price movements roughly two years later,” according to Kolko. Moreover, an analysis from Goldman Sachs also looked into previous episodes of oil price decline and its impact on the housing market. The analysis points out that “(…) construction [in Texas] grew dramatically during the boom phase of the oil cycle, with starts tripling between 1975 and 1984. By comparison, housing construction has been more moderate over the past several years.” Therefore, the negative impact in oil producing housing markets is expected to be smaller compared to previous episode.

However, other analysts are already worried. In a recent note, Capital Economics says that “The slump in oil prices has already had a huge adverse impact on drilling activity. (…) And it surely won’t be long before local employment and income levels are hit. That would obviously pose problems for the local housing market.” Meanwhile, Forbes says that the energy sector could spark a repeat of the subprime bust. House prices have started to decline in Calgary (Globe and Mail), and Dubai (National). Also, “Lenders are reassessing risks in energy towns as roughly $1.1 trillion of property loans come due across the U.S. over the next three years,” according to Bloomberg.

From the Global Housing Watch Newsletter: April 2015 Issue

Even though real house prices are rising in many countries, the global housing recovery remains on a two-speed pattern: in some countries, house prices have rebounded, while in others, they are still recovering. The bullet points below give a summary on experts’ views on current house price developments, policy response, short and long term outlook, and potential risks.

- Current house price developments.

Posted by at 1:28 PM

Labels: Global Housing Watch

Tuesday, April 21, 2015

Re-thinking Housing Markets

“[here’s] my list of culprits who might be to blame for getting so many Americans to buy homes they could not afford at prices that were unsustainable: (i) the Greenspan Fed, (ii) the rating agencies, (iii) the securitizers, (iv) Fannie Mae and Freddie Mac, (v) the mortgage originators, and (vi) Chinese savers. Greenspan has often provided a shorter list: (i) Chinese savers.”

Policy Papers:

On housing & the macroeconomy:

Ed Leamer: “The downturn of 2008–09 has confirmed that: (i) housing is the single most critical part of the U.S. business cycle, (ii) the proper conduct of monetary policy needs to be cognizant that choices made at one point in time affect the options later, and (iii) the best time to intervene in the housing cycle is when the volume of building is above normal and growing more so.”

John Muellbauer: “Three themes connecting housing and the macroeconomy are discussed. First, evidence is presented for the property market as one of the drivers of U.S. consumer price inflation. Second, key drivers of house prices are explained to account for the remarkable diversity of international experience. Finally, three potential links between housing, credit, and the financial accelerator are discussed. These are the consumption channel, the investment channel, and feedback between bad loans and risk-spreads via the financial system—and how institutional differences between countries can explain the presence, absence and magnitudes of these linkages.”

Stijn Claessens: [The paper discusses] “(i) house prices cycles and the macroeconomy, (ii) the current state of housing markets, and (iii) what to do about housing bubbles.”

On U.S. vs. Europe; why Canada has avoided a crisis; macropru and beyond:

Susan Wachter: “A house price boom occurred simultaneously in the United States and in a number of European countries from 2003 to 2007, accompanied in each case by an expansion in housing finance. This article considers the role of financial innovation along with incomplete markets in these cycles.”

Dwight Jaffee: “The United States and certain European countries (e.g., Ireland and Spain) have recently experienced serious distress in their residential mortgage markets. Public policy has responded with interventions to limit the deadweight costs of mortgage foreclosures, but with limited success. There are also open questions with respect to long-term reforms in mortgage market structures. In this paper, I make use of the important differences that exist between U.S. and European mortgage markets to help identify those aspects of residential mortgage markets that are most in need of reform.”

Philipp Hartmann: “An increasing number of studies suggest that borrower-based regulatory policies, such as reductions in loan-to-value or debt-to-income limits, can be effective in leaning against real estate booms. But many of the new macroprudential policy authorities in Europe do not have clear powers to determine them. Moreover, the cross-border spillovers they may give rise to suggest the establishment of a well-defined macroprudential coordination mechanism for the single European market.”

Allan Crawford: “This article discusses elements of Canada’s policy framework that contributed to the relatively good performance of its mortgage market in recent years, including supervisory practices and mortgage underwriting standards. Lender recourse and the nondeductibility of mortgage interest payments played a complementary role. Ongoing policy challenges are also identified, including the need for monitoring to ensure the current prolonged period of low interest rates does not lead to levels of debt and house prices that create future instability in housing and mortgage markets.”

David Miles: [The paper explores] “ways in which volatility in the housing market … can be reduced. Alternatives to standard debt contracts to finance house purchase are considered. A form of equity loan, where repayments are linked to the value of the house, have major advantages in terms of risk reduction. The way in which such loans can be structured is analyzed.”

There are also eight academic papers plus comments from discussants. The editors offer an executive summary of these papers.

Arezki et al: “This article provides an introduction to the JMCB special issue on housing bubbles, the global financial crisis, and the ensuing recessions in countries that experienced housing busts. We focus on five themes that are important for policymakers and researchers alike: the domestic and international factors driving housing booms and busts, the relevance of the housing sector for the real economy, how monetary policy should react to housing booms and busts, how housing and mortgage finance reform could affect financial stability, and the broad lessons learned for macroeconomics and macroprudential policy.”

Link to special issue of JMCB on housing: http://onlinelibrary.wiley.com/doi/10.1111/jmcb.2015.47.issue-S1/issuetoc

The issue was based on the proceedings of a conference, the first of three conferences that were organized as part of the Global Housing Watch initiative under IMF Deputy Managing Director Zhu. Ungated versions of the conference papers and some of the panel discussions, plus a keynote address by Bob Shiller, are available here: http://www.dallasfed.org/research/events/2013/13housing.cfm

Rabah Arezki and I are among the co-editors of a special issue of the Journal of Money Credit & Banking on housing markets that was just published. It has an interesting set of policy papers by experts (Ed Leamer, Susan Wachter, Stijn Claessens, David Miles, Dwight Jaffee, Allan Crawford, John Muellbauer, Philipp Hartmann) and eight academic papers with comments from discussants—including Ed Leamer’s lightly-censored views on various things (including DSGE models). Here for example is Ed on who was to blame for the housing crisis:

“[here’s] my list of culprits who might be to blame for getting so many Americans to buy homes they could not afford at prices that were unsustainable: (i) the Greenspan Fed,

Posted by at 6:22 PM

Labels: Global Housing Watch

Tuesday, April 7, 2015

House Prices in the United States

The National Association of Realtors takes a look at single-family median home prices in metro areas of 16 teams playing baseball Opening Day on April 6, 2015.

Posted by at 6:28 PM

Labels: Global Housing Watch

Thursday, April 2, 2015

House Prices in Qatar

- While the total number of real estate transactions has decreased from the 2013 peak, the total value of real estate transactions has dramatically increased, reflecting higher average prices and compositional changes.

- Land prices appear to have increased at the fastest pace, followed by villas where land is typically the most important cost component. Price increases have been slower for apartments and villas with extension (e.g., a guest house).

- While the Doha market experienced intermittent price hikes, price growth was recently strongest outside of Doha, given development projects and urbanization. For example, prices in Al Wakrah, a previously underdeveloped neighbor to Doha, have notably risen over the past year in light of its proximity to the new Hamad International Airport and the planned Doha Expressway route. Al Daayen has similarly experienced rapid price growth, due in part to its proximity to Lusail City and various 2022 World Cup projects.”

“Real estate prices accelerated last year, despite the sharp drop in oil prices,” according to the IMF’s latest annual report on Qatar. The report points out that “price growth gathered speed especially in the second half of 2014, with the December real estate values up by 35 percent year-on-year. Staff calculations based on transaction-level data from the Ministry of Justice point to the following broad trends:

- While the total number of real estate transactions has decreased from the 2013 peak,

Posted by at 5:15 PM

Labels: Global Housing Watch

Subscribe to: Posts