Wednesday, March 26, 2014

Robert Barro doesn’t look 70

My profile of one of my thesis advisors, Robert Barro, for whom the LSE held a major conference last week. Of all the profiles I’ve written I like this the best — I think I knew the subject matter well and it shows.

My profile of one of my thesis advisors, Robert Barro, for whom the LSE held a major conference last week. Of all the profiles I’ve written I like this the best — I think I knew the subject matter well and it shows.

Posted by at 12:15 AM

Labels: Profiles of Economists

Wednesday, March 19, 2014

IMF Releases Independent Assessment of its Forecast Accuracy

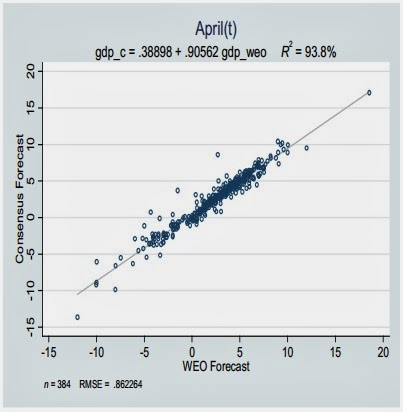

The IMF’s independent evaluation office released its study of IMF Forecasts: Process, Quality, and Country Perspectives. It concludes that “the accuracy of IMF short-term forecasts is comparable to that of private forecasts. Both tend to over predict GDP growth significantly during regional or global recessions, as well as during crises in individual countries.” The study thus confirms the two main findings of my 2001 paper: first, “the record of failure to predict recessions is virtually unblemished,” as I wrote; second, a statistical horse race between private sector and official sector forecasts ends up in a photo finish. My recent work with Hites Ahir looks at the record of professional forecasters in predicting recessions over the period 2008-12, also confirming both findings. The figure shows the close correspondence between Consensus (private sector) and IMF forecasts.

The IMF’s independent evaluation office released its study of IMF Forecasts: Process, Quality, and Country Perspectives. It concludes that “the accuracy of IMF short-term forecasts is comparable to that of private forecasts. Both tend to over predict GDP growth significantly during regional or global recessions, as well as during crises in individual countries.” The study thus confirms the two main findings of my 2001 paper: first, “the record of failure to predict recessions is virtually unblemished,” as I wrote;

Posted by at 12:57 PM

Labels: Forecasting Forum

Saturday, March 15, 2014

House Prices in Malaysia

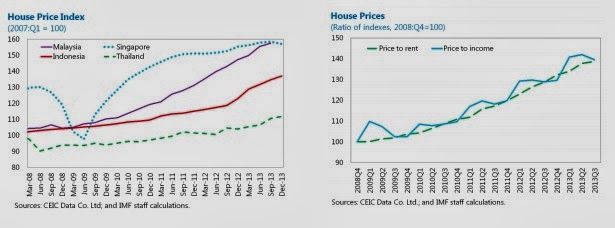

“House prices have increased rapidly, outpacing income and rental growth, along with strong demand for residential property loans, driven by a robust labor markets and falling lending rates. However, underwriting standards do not appear to have deteriorated, as evidenced by lower default rates by month on book for more recent vintages,” says the annual IMF economic report on Malaysia.

“House prices have increased rapidly, outpacing income and rental growth, along with strong demand for residential property loans, driven by a robust labor markets and falling lending rates. However, underwriting standards do not appear to have deteriorated, as evidenced by lower default rates by month on book for more recent vintages,” says the annual IMF economic report on Malaysia.

Posted by at 4:46 PM

Labels: Global Housing Watch

Thursday, March 13, 2014

Lipton Releases IMF Paper on Fiscal Policy and Inequality

IMF First Deputy Managing Director David Lipton released a new paper on fiscal policy and inequality, adding to the stock of IMF work on this issue. Here are links and a cheat sheet to the key papers:

1) Painful Medicine: This (non-wonkish) paper documented that fiscal consolidations not only lower aggregate incomes but have distributional consequences—wage incomes fall more than profits; and the long-term unemployed are affected more than short-term unemployed.

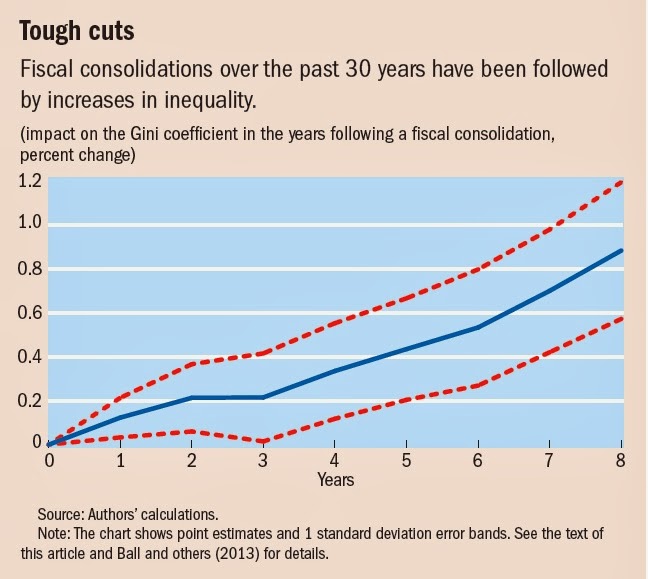

2) The Distributional Effects of Fiscal Consolidation: A wonkish version of the “Painful Medicine” article, with the additional result that, between 1978 and 2009, fiscal consolidations in advanced economies increased the Gini measure on income inequality.

3) Distributional Consequences of Fiscal Consolidation and the Role of Fiscal Policy: In addition to confirming the results in the previous papers, this paper brings in evidence from emerging markets. It also discusses how policies can be designed to mitigate the impacts of fiscal policy on inequality.

4) Who Let the Gini Out? A (non-wonkish) summary of some of the previous papers.

5) Fiscal Policy and Inequality: A key finding of the paper is that fiscal consolidations during the Great Recession did not lead to increases in inequality.

IMF First Deputy Managing Director David Lipton released a new paper on fiscal policy and inequality, adding to the stock of IMF work on this issue. Here are links and a cheat sheet to the key papers:

1) Painful Medicine: This (non-wonkish) paper documented that fiscal consolidations not only lower aggregate incomes but have distributional consequences—wage incomes fall more than profits; and the long-term unemployed are affected more than short-term unemployed.

Posted by at 5:49 PM

Labels: Inclusive Growth

Wednesday, March 12, 2014

House Prices in Belgium

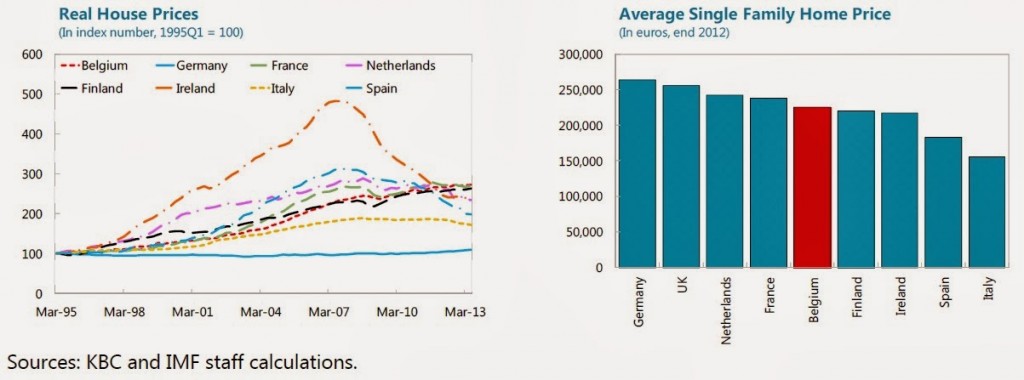

House prices are overvalued by “5–15 percent” according to a new IMF report on the Belgium economy. The report says that “Risks of a sharp correction of real estate prices appear contained. Property prices have risen by 110 percent in real terms since 2000, and, unlike in other EU countries, continued to increase through the financial crisis. Overvaluation estimates range from 10–60 percent, but valuation estimates based on price-to-income and price-to-rent ratios often miss catch-up effects. A finer assessment (interest-adjusted affordability regression analysis) suggests overvaluation of 5–15 percent. In fact, absolute prices remain moderate by European comparison. High ownership rates (around 70 percent), coupled with persistent housing shortages, are likely to prevent a rapid price decline. Robust household balance sheets, the prevalence of fixed interest rate mortgages, and the recent tightening of capital requirements on mortgage lending should limit the impact of an interest rate and/or unemployment shocks on the quality of the mortgage portfolio. However, the prevalence of fixed-rate mortgages shifts the interest rate risk to banks.”

House prices are overvalued by “5–15 percent” according to a new IMF report on the Belgium economy. The report says that “Risks of a sharp correction of real estate prices appear contained. Property prices have risen by 110 percent in real terms since 2000, and, unlike in other EU countries, continued to increase through the financial crisis. Overvaluation estimates range from 10–60 percent, but valuation estimates based on price-to-income and price-to-rent ratios often miss catch-up effects.

Posted by at 5:02 PM

Labels: Global Housing Watch

Subscribe to: Posts