Wednesday, February 26, 2014

The IMF on Inequality: New Ostry-Berg Paper on Redistribution

A new paper by Andrew Berg and Jonathan Ostry (along with Haris Tsangarides) adds to the growing stock on IMF work on inequality.

In the recent past, the IMF has released papers on the impacts of fiscal tightening on inequality — see a summary here and to the research on which it is based here and here.

The IMF has also looked at the impact of capital account liberalization on inequality — see this article and Vox post.

The Berg-Ostry paper showed that inequality lowers the duration of growth spells. The new paper makes the case that redistribution efforts to lower inequality are not harmful to growth.

A new paper by Andrew Berg and Jonathan Ostry (along with Haris Tsangarides) adds to the growing stock on IMF work on inequality.

In the recent past, the IMF has released papers on the impacts of fiscal tightening on inequality — see a summary here and to the research on which it is based here and here.

The IMF has also looked at the impact of capital account liberalization on inequality —

Posted by at 4:04 PM

Labels: Inclusive Growth

Thursday, February 20, 2014

House Prices in Spain

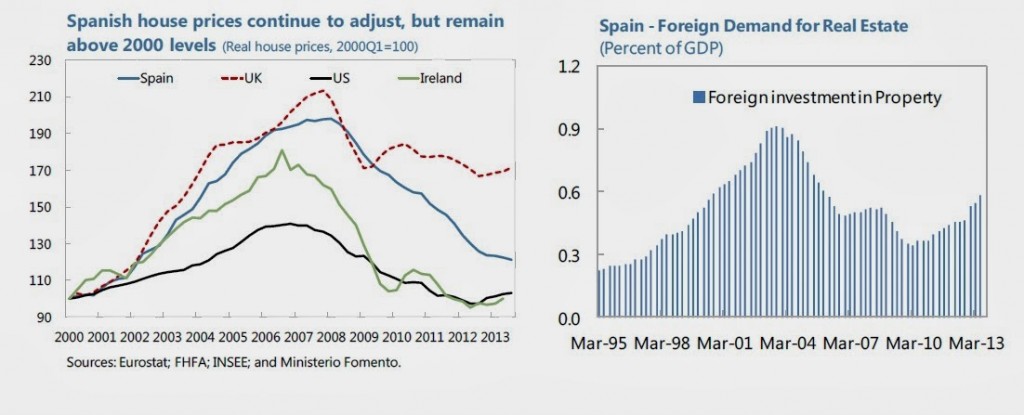

“Although house prices have started to stabilize in the most recent data, further declines are possible as the supply overhang is still large (the stock of vacant new houses equals four years of sales, and the population is falling). On the upside, foreign investor interest in Spanish property has increased noticeably in recent months,” according to a new report from the IMF.

Posted by at 8:25 PM

Labels: Global Housing Watch

Friday, February 14, 2014

Does Debt Hurt Growth? Revisiting Reinhart and Rogoff

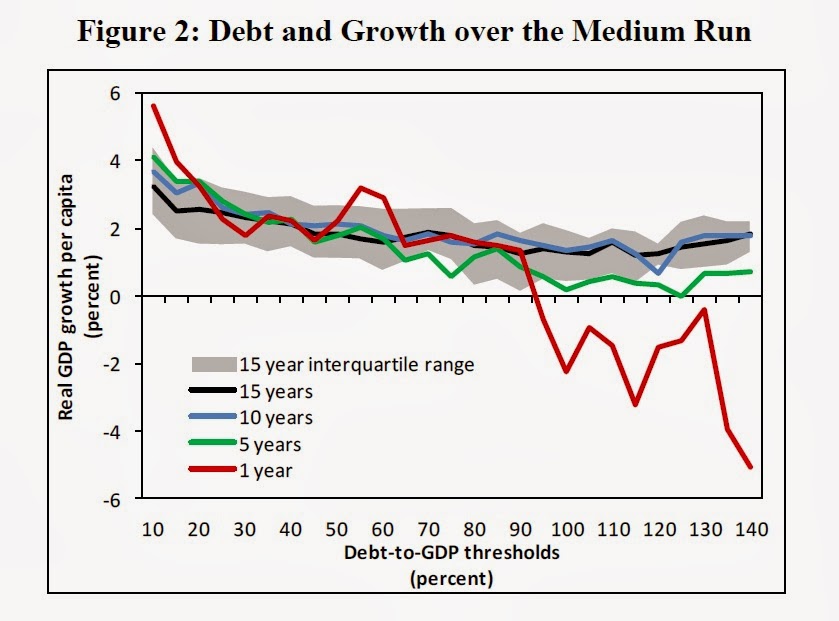

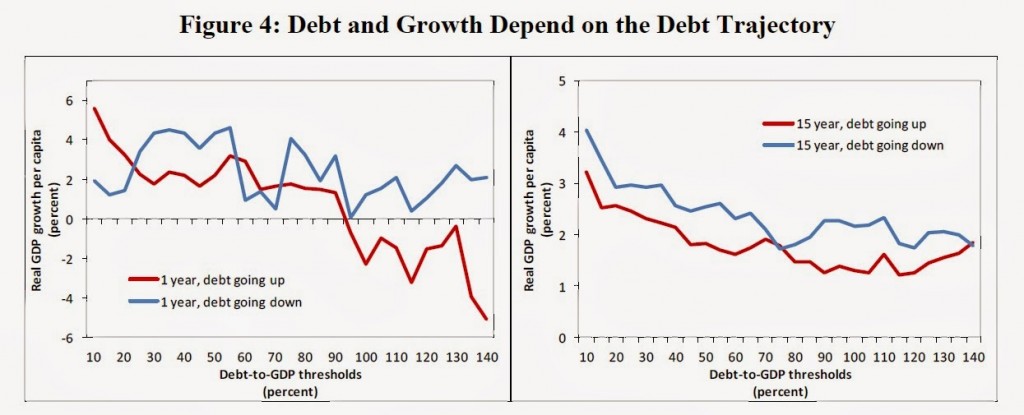

Is there a debt threshold that impairs medium term economic growth? The answer is no, according to a research paper by Andrea Pescatori, Damiano Sandri, and John Simon. They say that “Our analysis of historical data has highlighted that there is no simple threshold for debt ratios above which medium-term growth prospects are severely undermined. On the contrary, the association between debt and growth at high levels of debt becomes rather weak when one focuses on any but the shortest-term relationship, especially when controlling for the average growth performance of country peers. Furthermore, we find evidence that the relation between the level of debt and growth is importantly influenced by the trajectory of debt: countries with high but declining levels of debt have historically grown just as fast as their peers. The fact that there is no clear debt threshold that severely impairs medium term growth should not, however, be interpreted as a conclusion that debt does not matter. For example, we have found some evidence that higher debt appears to be associated with more volatile growth. And volatile growth can still be damaging to economic welfare.

As in previous empirical studies, our analysis is still subject to potential endogeneity concerns that should caution against drawing strong policy implications. However, by mitigating the short-term and mechanical reverse causality problems whereby low growth leads to higher debt, we show that the prima facie case for debt thresholds is substantially weakened. We find no evidence of threshold effects over any but the shortest-term horizons. Furthermore, the remaining relationship between debt and growth is relatively muted and the magnitude is much smaller than the dramatic figures suggested in earlier studies. Notwithstanding this, because of residual issues that confound the interpretation of the medium-term relationship between debt and growth, we emphasize that this does not establish what the underlying structural relationship is. That must wait for more sophisticated work that can properly address the complex identification issues that characterized this area of research.”

Is there a debt threshold that impairs medium term economic growth? The answer is no, according to a research paper by Andrea Pescatori, Damiano Sandri, and John Simon. They say that “Our analysis of historical data has highlighted that there is no simple threshold for debt ratios above which medium-term growth prospects are severely undermined. On the contrary, the association between debt and growth at high levels of debt becomes rather weak when one focuses on any but the shortest-term relationship,

Posted by at 10:31 PM

Labels: Inclusive Growth

Thursday, February 13, 2014

Okun’s Not Brokun’: Jobs and Growth are Still Linked

In an update of our work, Laurence Ball, Daniel Leigh and I find that the link between output growth and employment growth holds strongly in most advanced economies. We find no evidence that this link—which goes by the wonkish name of Okun’s Law—broke down during 2008 to 2013, including in high unemployment countries like Ireland and Spain. On average across the 20 advanced economies we study, a 1 percentage point increase in output growth leads to a ½ percentage point increase in employment growth. We find that Okun’s Law survived the stress test of the Great Recession: there is little evidence that the link between growth and jobs changed appreciably over the course of the Great Recession. The alleged breakdown of Okun’s Law is often a jumping-off point for arguing that structural reforms are needed to make a major dent in unemployment. Our results suggest that while there may be good reasons to recommend structural reforms to boost employment, proposing them in the belief that Okun’s Law has broken down should not be one of them.

In related work, Laurence Ball, Joao Jalles and I find that forecasters believe in Okun’s Law. For the nine advanced economies we study, the estimates of the Okun’s coefficients from forecasts is fairly similar to that in the data for various countries.

In an update of our work, Laurence Ball, Daniel Leigh and I find that the link between output growth and employment growth holds strongly in most advanced economies. We find no evidence that this link—which goes by the wonkish name of Okun’s Law—broke down during 2008 to 2013, including in high unemployment countries like Ireland and Spain. On average across the 20 advanced economies we study, a 1 percentage point increase in output growth leads to a ½ percentage point increase in employment growth.

Posted by at 7:06 PM

Labels: Inclusive Growth

House Prices in Australia

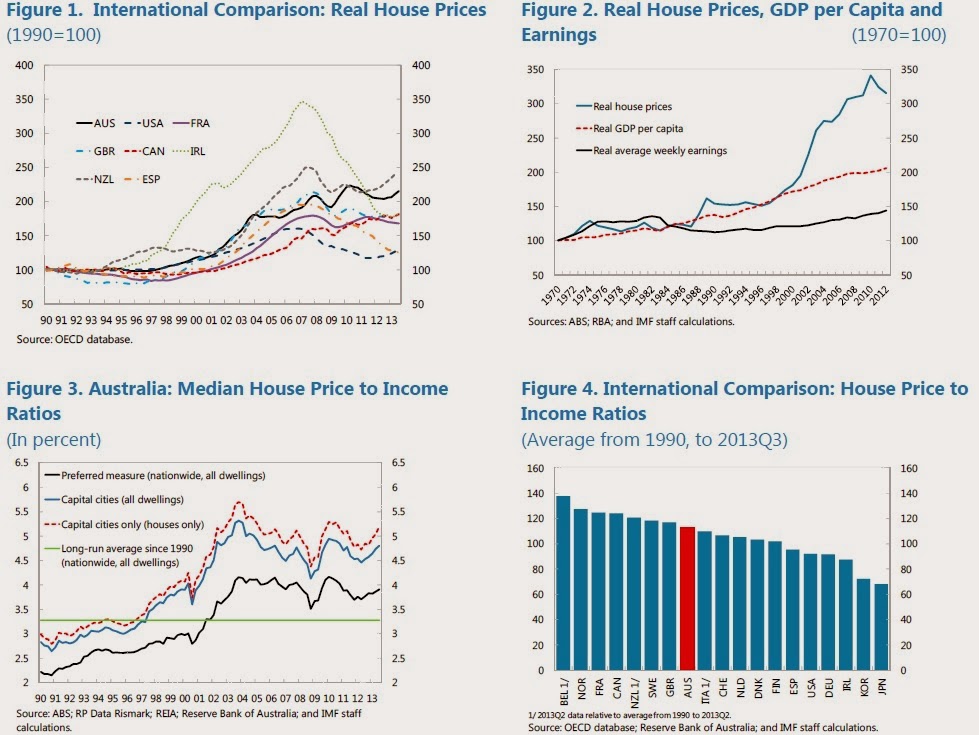

“Reflecting structural factors both shared with many other countries and unique to Australia, real house prices have roughly doubled since 1990 (Figure 1). After growing broadly in line with real GDP per capita from 1960-90, real house price inflation picked up in the 2000s and exceeded income growth for much of the period up to the global financial crisis (Figure 2). As a result, the median house price to income ratio rose sharply from around 3 at the beginning of the 2000s (when based on the authorities’ preferred measure for all dwellings) peaking at just over 4 in 2009 (Figure 3). Since then the price/income ratio has eased back and international comparisons suggest that while Australia’s is on the high side it is not out of line with peers (Figure 4). Rising house prices were also accompanied by increased household borrowing with the debt to income ratio rising from among the lowest at 46 percent in 1990 to around 150 per cent in 2013,” according to the latest IMF’s annual report on Australia.

“Reflecting structural factors both shared with many other countries and unique to Australia, real house prices have roughly doubled since 1990 (Figure 1). After growing broadly in line with real GDP per capita from 1960-90, real house price inflation picked up in the 2000s and exceeded income growth for much of the period up to the global financial crisis (Figure 2). As a result, the median house price to income ratio rose sharply from around 3 at the beginning of the 2000s (when based on the authorities’ preferred measure for all dwellings) peaking at just over 4 in 2009 (Figure 3).

Posted by at 6:50 PM

Labels: Global Housing Watch

Subscribe to: Posts