Wednesday, October 23, 2013

House Prices in Brazil

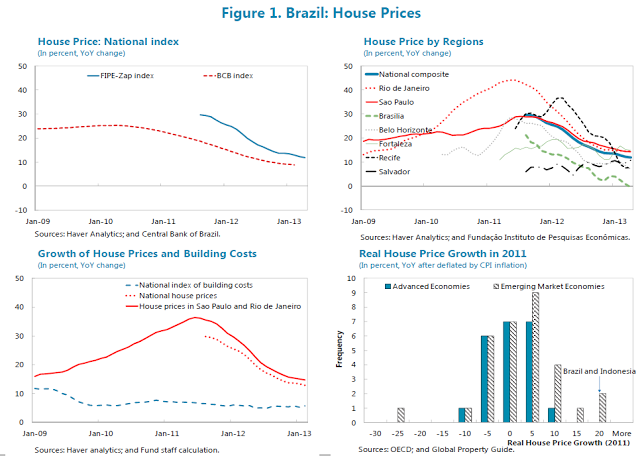

“Brazil’s house prices rose substantially over the last few years, especially in two major cities (Figure 1). The national FIPE–Zap index has increased 62 percent from August 2010 to April 2013. It rose 26 and 14 percent in 2011 and 2012 respectively, while construction costs did not rise in tandem. The prices for Sao Paulo and Rio de Janeiro have almost tripled since January 2009, and grew by 30 and 15 percent in 2011 and 2012. Brazil was one of two countries that showed the highest real house price appreciation in 2011 among 52 advanced and emerging market economies,” according to a new report from the IMF.

“Brazil’s house prices rose substantially over the last few years, especially in two major cities (Figure 1). The national FIPE–Zap index has increased 62 percent from August 2010 to April 2013. It rose 26 and 14 percent in 2011 and 2012 respectively, while construction costs did not rise in tandem. The prices for Sao Paulo and Rio de Janeiro have almost tripled since January 2009, and grew by 30 and 15 percent in 2011 and 2012.

Posted by at 11:43 PM

Labels: Global Housing Watch

Friday, October 18, 2013

Blanchard on Unemployment, Flexibility & IMF Advice

My VoxEU post with Olivier Blanchard and Florence Jaumotte tries to move beyond ritual invocation of the mantra of “labor market flexibility.” We develop the concepts of “micro” and “macro flexibility”; explain why they are needed; what labor market institutions help or hinder micro and macro flexibility; and assess IMF advice against the backdrop of these concepts. The Staff Discussion Note on which our post is based is available here.

My VoxEU post with Olivier Blanchard and Florence Jaumotte tries to move beyond ritual invocation of the mantra of “labor market flexibility.” We develop the concepts of “micro” and “macro flexibility”; explain why they are needed; what labor market institutions help or hinder micro and macro flexibility; and assess IMF advice against the backdrop of these concepts. The Staff Discussion Note on which our post is based is available here.

Posted by at 3:22 PM

Labels: Inclusive Growth

Monday, October 14, 2013

Nobel Prize winner Robert Shiller on house prices … and Eliot Spitzer

My ‘golden oldie’ interview with Robert Shiller still makes for interesting reading. It is prescient but even Shiller could not have predicted the fate of Eliot Spitzer.

Shiller on US corporate scandals: “On that score I’m actually somewhat sanguine … Eliot Spitzer has been going after corporate crime as aggressively as Eliot Ness, the guy who went after the gangster Al Capone. Combine that with people like … William Donaldson, Chair of the SEC, and it adds up to a lot of people who are really doing their jobs. The budget for the SEC has really been increased; for 2004, it was over $800 million, more than double what it was five years ago. And people can see what a price Martha Stewart paid for acting on a tip. This is the U.S. solution: the United States has generally handled financial scandals aggressively.”

Shiller on housing markets (in 2004): “I’m not exactly sure what’s going on with housing prices. People still report that a major consideration for their buying houses is that they think it is a good investment; that is, they expect house prices to appreciate. But fewer people report buying houses just to make a profit from speculation. I think the thought process a lot of homebuyers are going through right now is more like: I know prices are too high, but that’s what I thought last year and prices still went up. I better buy now before I’m totally priced out.”

Shiller on importance of combining psychology and economics: “We know the role that overconfidence and wishful thinking play in driving financial markets. But psychological theories have still not been completely integrated into economics. Human behavior is very complex, and economists have been in the mood to simplify it, and simplify it heroically. We will have to change our whole approach to problems—our methodology and our tool kits—if we are serious about grappling with the complexity of human behavior.”

Shiller on how he got into behavioral finance: “I wasn’t much of a rebel as a graduate student. My dissertation was on rational expectations. But I was always a bit skeptical about conventional economic theory. An early formative influence was George Katona, who wrote the book Psychological Economics in 1975. I never took one of his courses, but I sat in on one of his lectures and was impressed. It seemed fine to me, then, that there were only a few people like Katona who wanted to sit halfway between economics and psychology. It wasn’t as clear to me then as now that psychology should be central to economics. Much later, Stan Fischer invited me to write a review essay critiquing the rational expectations revolution for a conference he’d organized. Writing that essay awakened further doubts about rational expectations, which I always thought of as a construct that had some interest but was a small part of a big picture.”

Read the full interview here and also a very nice profile of Shiller written by Paolo Mauro.

My ‘golden oldie’ interview with Robert Shiller still makes for interesting reading. It is prescient but even Shiller could not have predicted the fate of Eliot Spitzer.

Shiller on US corporate scandals: “On that score I’m actually somewhat sanguine … Eliot Spitzer has been going after corporate crime as aggressively as Eliot Ness, the guy who went after the gangster Al Capone. Combine that with people like … William Donaldson, Chair of the SEC,

Posted by at 1:07 PM

Tuesday, October 8, 2013

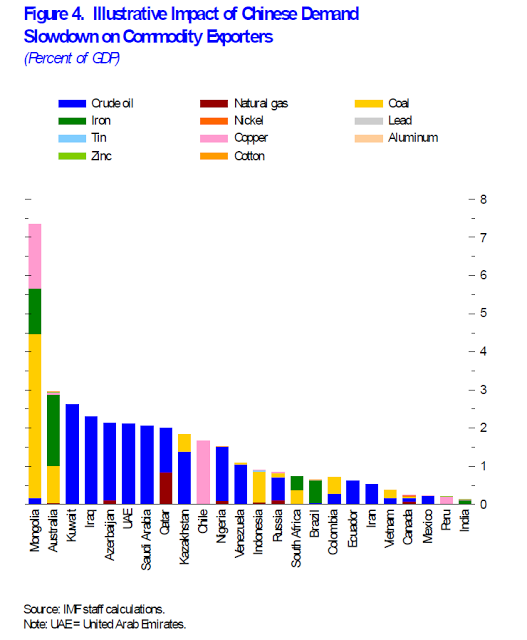

The ‘Shale Gale’ and the ‘China Chill’: the IMF’s Commodity Market Review

How will the shale revolution affect U.S. GDP and trade

balance? How would a growth slowdown in China affect commodity exporters?

Answers given in the IMF’s commodity markets review, released this morning as

part of the World Economic Outlook.

the unconventional energy revolution on U.S. prospects. The simulations of the

IMF’s large scale models suggest a modest impact: increases in unconventional

energy production of the magnitude currently forecast will raise U.S. real GDP

by only 1.2 percent at the end of 13 years and employment by 0.5 percent. The

main reason is the small share of energy in the U.S. economy, even after

factoring in the additional production.

China’s growth slows from an average of 10 percent over the past decade to an

average of 7 ½ percent over the coming decade? The IMF’s illustrative

calculations rank the countries that have benefitted the most from past Chinese

growth—and therefore the ones that could be vulnerable in the absence of

policy actions.

new analysis from my colleague Samya Beidas-Strom on the drivers of the

Brent-WTI differential

How will the shale revolution affect U.S. GDP and trade

balance? How would a growth slowdown in China affect commodity exporters?

Answers given in the IMF’s commodity markets review, released this morning as

part of the World Economic Outlook.

Shale Gale: There has been some euphoria about the impact of

the unconventional energy revolution on U.S. prospects. The simulations of the

IMF’s large scale models suggest a modest impact: increases in unconventional

energy production of the magnitude currently forecast will raise U.S. Read the full article…

Posted by at 1:00 PM

Labels: Energy & Climate Change

Subscribe to: Posts