Thursday, August 29, 2013

Stan Fischer: A Class Act

In 2012, the magazine Global Finance gave Stanley Fischer, then central bank governor of Israel, an A for his handling of the economy during the financial crisis. It was the fourth year in a row that Fischer had received an A. It’s a grade the former professor—who taught both Federal Reserve Board Chairman Ben Bernanke and European Central Bank (ECB) President Mario Draghi—cherishes: “Those were some tough tests we faced in Israel.”

Fischer stepped down as central bank governor in June this year after eight years in the job, bringing the curtain down on an extraordinary third act of his career. The second act was as the IMF’s second-in-command during the tumultuous period of financial crises in emerging markets from 1994 to 2001. This role as policymaker came after a rousing opening act in the 1970s and 1980s, during which Fischer established himself as a preeminent macroeconomist, one who defined the contours of the field through his scholarly work and textbooks. It speaks to Fischer’s success that stints as the World Bank’s chief economist in the 1980s and as vice chairman at Citigroup in the 2000s—which would be crowning achievements of many a career—come across as interludes between the main acts. For the full profile, continue reading here.

In 2012, the magazine Global Finance gave Stanley Fischer, then central bank governor of Israel, an A for his handling of the economy during the financial crisis. It was the fourth year in a row that Fischer had received an A. It’s a grade the former professor—who taught both Federal Reserve Board Chairman Ben Bernanke and European Central Bank (ECB) President Mario Draghi—cherishes: “Those were some tough tests we faced in Israel.”

Fischer stepped down as central bank governor in June this year after eight years in the job,

Posted by at 9:54 PM

Labels: Profiles of Economists

Wednesday, August 28, 2013

Florida vs. Spain: Labor Mobility within Currency Unions

Paul Krugman has blogged extensively on how states within the US currency union have adjusted better than regions and countries within the European currency unions. My presentation at the European Regional Science Association today gives some background on this discussion and some new results.

Paul Krugman has blogged extensively on how states within the US currency union have adjusted better than regions and countries within the European currency unions. My presentation at the European Regional Science Association today gives some background on this discussion and some new results.

Posted by at 11:14 AM

Labels: Inclusive Growth

Thursday, August 22, 2013

The Driving Force behind Construction in Europe

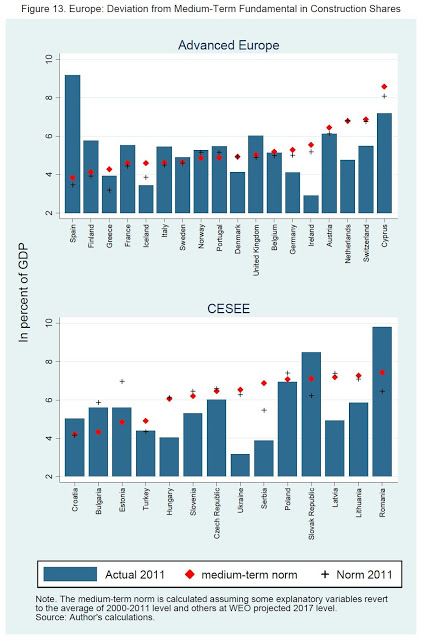

A new IMF working paper finds that a country’s geography, demographics, and economic conditions (e.g. income level, credit conditions, and stock market performance) are the driving forces behind the changes in construction shares. The results of the paper show that “During the boom, many countries overshoot the norm. After the crisis, the process has reversed and many countries have undershoot the norm. But for some countries, the adjustment has fallen short of the model’s predictions.” So, “when economic conditions normalize over the medium term, Greece, Iceland, and Ireland in advanced Europe, and Latvia, Lithuania, Hungary, and Ukraine in emerging Europe may see a recovery in their construction shares. But construction shares could decline further in Spain, the United Kingdom, Romania, and the Slovak Republic.”

A new IMF working paper finds that a country’s geography, demographics, and economic conditions (e.g. income level, credit conditions, and stock market performance) are the driving forces behind the changes in construction shares. The results of the paper show that “During the boom, many countries overshoot the norm. After the crisis, the process has reversed and many countries have undershoot the norm. But for some countries, the adjustment has fallen short of the model’s predictions.” So,

Posted by at 5:49 PM

Labels: Global Housing Watch

Friday, August 16, 2013

The Stock Market ‘Prediction Charade’

“The next time you are tempted to rely on forecasts of experts in making investment decisions, remember these words attributed to Prakash Loungani of the International Monetary Fund: “The record of failure to predict recessions is virtually unblemished.” Read the full story here.

“The next time you are tempted to rely on forecasts of experts in making investment decisions, remember these words attributed to Prakash Loungani of the International Monetary Fund: “The record of failure to predict recessions is virtually unblemished.” Read the full story here.

Posted by at 2:07 PM

Labels: Forecasting Forum

Thursday, August 15, 2013

Okun’s Law during the Great Recession: jobs and growth are still linked

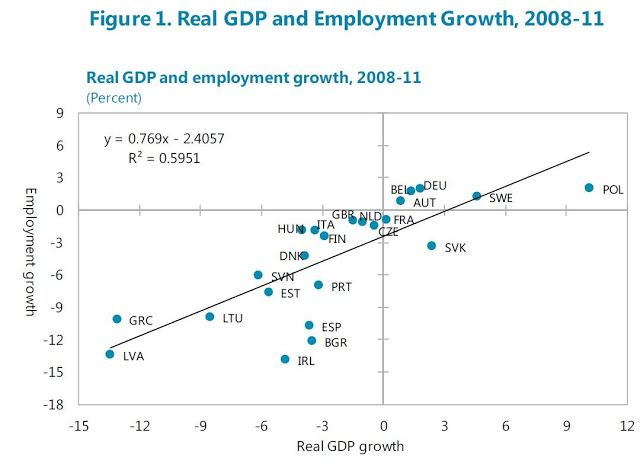

There is further evidence that employment growth is low because output growth is poor. According to a new IMF working paper, “Much of [the cross-country differences in employment growth] are the result of the differences in real GDP growth. A scatter chart of real GDP growth and employment growth between 2008 and 2011 shows a strong correlation between the two (Figure 1). Latvia, which had the largest decline in real GDP between 2008 and 2011, also experienced one of the largest reductions in employment. And Poland, which had the largest increase in real GDP during this time period, also had one of the best employment outcomes.”

Ball, Leigh, and Loungani also provide evidence on how well Okun’s Law has held up during the Great Recession.

There is further evidence that employment growth is low because output growth is poor. According to a new IMF working paper, “Much of [the cross-country differences in employment growth] are the result of the differences in real GDP growth. A scatter chart of real GDP growth and employment growth between 2008 and 2011 shows a strong correlation between the two (Figure 1). Latvia, which had the largest decline in real GDP between 2008 and 2011, also experienced one of the largest reductions in employment. And Poland,

Posted by at 8:50 PM

Labels: Inclusive Growth

Subscribe to: Posts