Tuesday, April 16, 2013

Why is the Global Recovery So Weak?

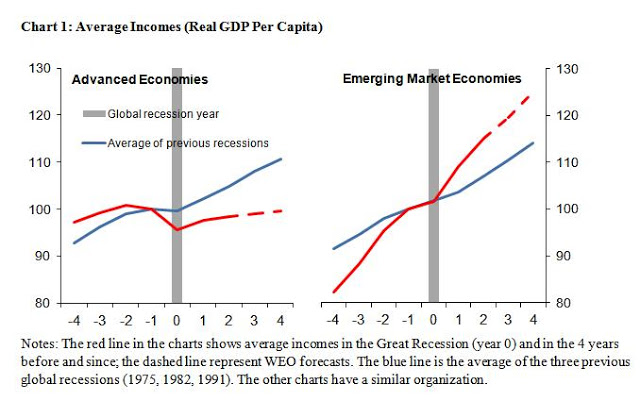

The Great Recession has been followed by the Not-So-Great Recovery. The IMF’s World Economic Outlook (WEO) shows that average incomes in advanced economies are rising, and are projected to rise, at a much slower rate than in past global recoveries. In contrast, incomes in emerging markets are growing at a much faster pace than during past recoveries—see chart 1. The WEO discusses several reasons for this divergence in fortunes.

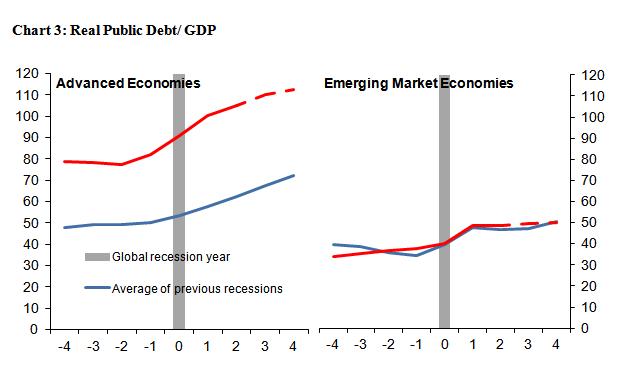

Caution about fiscal stimulus in advanced countries likely reflects the fact that they entered the Great Recession with much higher levels of debt than in the past—see Chart 3.

Box 1.1 does not get into an “an assessment of whether the different policy mix in this recession and recovery was appropriate. The response of policies may have been reasonable given the respective room available for fiscal and monetary policies in advanced economies. But there are also concerns. Even though monetary policy has been effective, policymakers had to resort to unconventional measures. Even with these measures, the zero bound on interest rates and the extent of financial disruption during the crisis have lowered the traction of monetary policy. This, together with the extent of slack in these economies, may have amplified the impact of contractionary fiscal policies. Four years into a weak recovery, policymakers may therefore need to worry about the risk of overburdening monetary policy because it is being relied on to deliver more than it has traditionally.”

Read Box 1.1 from the WEO here for the full analysis.

The Great Recession has been followed by the Not-So-Great Recovery. The IMF’s World Economic Outlook (WEO) shows that average incomes in advanced economies are rising, and are projected to rise, at a much slower rate than in past global recoveries. In contrast, incomes in emerging markets are growing at a much faster pace than during past recoveries—see chart 1. The WEO discusses several reasons for this divergence in fortunes.

Box 1.1 of the WEO notes the divergence in fiscal polices. Read the full article…

Posted by at 12:25 PM

Labels: Forecasting Forum

Thursday, April 4, 2013

IMF Urges Caution on Union Policy

A WSJ blog notes: Changing euro-zone labor-market institutions has been one of the main goals of the bailout programs managed by the International Monetary Fund and euro-zone authorities over the last three years.

The thinking is: Europe’s labor markets – particularly those in the euro-zone periphery – need overhauls to allow wages to keep pace with changes in productivity and economic circumstances. This sounds like dry stuff, but it’s been one of the fund’s more controversial bailout recommendations. Making labor markets more “flexible” has in practice meant reducing the role of labor unions in wage-setting across much of southern Europe, leaving unions none-too-pleased with their more limited powers.

In a paper published on Friday, IMF economists led by Olivier Blanchard took a somewhat soul-searching look at the fund’s labor-market advice over the last three years. One interesting finding: The fund should “tread carefully” in its recommendations on collective bargaining, the paper suggests, since evidence about what kinds of bargaining arrangements work best is mixed. Read the full article here.

A WSJ blog notes: Changing euro-zone labor-market institutions has been one of the main goals of the bailout programs managed by the International Monetary Fund and euro-zone authorities over the last three years.

The thinking is: Europe’s labor markets – particularly those in the euro-zone periphery – need overhauls to allow wages to keep pace with changes in productivity and economic circumstances. This sounds like dry stuff, but it’s been one of the fund’s more controversial bailout recommendations.

Posted by at 9:26 PM

Labels: Inclusive Growth

Tuesday, April 2, 2013

How Labor Markets Can Support Workers, Economic Growth

IMF staff have taken a fresh look at how labor markets can support workers and growth.

The unemployment rate in advanced economies exceeds 8 percent, with much higher unemployment rates among the young. A third of all young unemployed have been without work for six months or longer.

Countries face the challenge of putting these millions of people back to work and getting the young started in their careers. A new IMF Staff Discussion Note—Labor Market Policies and IMF Advice in Advanced Economies during the Great Recession—reviews IMF advice to help countries meet this challenge

The paper was written by Olivier Blanchard, the IMF’s Economic Counselor and Research Department Director, along with his colleagues Florence Jaumotte and Prakash Loungani.

Weak demand

The IMF has diagnosed high unemployment to be a result primarily of weak aggregate demand, the paper notes. Hence, it has advised that monetary and fiscal policies support demand to the extent possible, alongside generous unemployment insurance to help people cope with the human costs of being out of work.

At the onset of the crisis, the IMF called for a coordinated global fiscal stimulus, which prevented “a much worse collapse in demand than actually took place.” Along with fiscal stimulus, the paper mentions the role of policies to promote work-sharing programs, particularly in Germany, and concludes that the positive experience “has led to a reassessment of such policies at the IMF and elsewhere.”

While in a number of countries high debt has now made fiscal consolidation unavoidable, the paper recommends that such consolidation should proceed as gradually as possible and be accompanied by supportive monetary policy.

While supportive macro policies are a central part of the IMF’s advice, the paper’s focus is on the design of labor market policies and institutions to reduce average unemployment rates and boost medium-run growth.

Micro flexibility

Productivity growth—the ultimate source of gains in incomes—requires reallocation of resources from low to high productivity jobs and firms. Labor markets must permit this “micro flexibility.”

Research strongly suggests that micro flexibility is better achieved by protecting workers through unemployment insurance than employment protection. Unemployment insurance, combined with support for job searchers, makes it easier for workers to move between jobs while safeguarding their welfare.

While there is an important role for employment protection, if excessive it impedes the necessary reallocation process. The authors also recommend that dual employment protection—where high employment protection for those on permanent contracts coexists with lighter regulation on temporary contracts—should be avoided. Such a system makes the burden of adjustment fall on those on temporary contracts, who are often the young. The concentration of unemployment among the youth in many countries is a result of this duality, the authors argue, noting that the IMF has advised reducing duality in Italy, Portugal, and Spain.

Macro flexibility

Labor market policies and institutions should allow economies to adjust to macroeconomic shocks while minimizing unemployment—this is “macro flexibility.” The paper suggests that to support this flexibility, a collective bargaining structure based on a combination of national and firm-level bargaining seems attractive.

While national agreements provide coordination and help wages and prices respond to macroeconomic shocks, firm-level agreements can help wages adjust to the circumstances that companies face. The authors recognize, however, that there are also examples of efficient bargaining at the sectoral level. What seems to be important in all cases is not so much the specific arrangements as trust among social partners.

For a number of euro area countries (the so-called “periphery” or “South”), the path to recovery is through enhanced competitiveness. The two options for doing so are increasing productivity and cutting relative wages. When this needs to be done urgently, the near-term burden often falls on wage cuts because raising productivity can take a long time.

While it would be best for governments, employers, and workers to agree on wage cuts, this typically has not happened. Absent such agreements, the IMF has suggested accelerating the adjustment through various options. These include making wages reflect productivity at the firm level and, in some cases, decreasing wages in the public sector.

Not all of the burden of adjustment should be borne by the “South.” The authors note that reversing the competitiveness gap in the euro area “implies accepting higher inflation in the North of the currency union than in the South”.

The start of a discussion?

As the title of the series suggests, IMF Staff Discussion Notes are published to elicit comments and further debate on topical issues. While the paper already reflects inputs from some international institutions and trade unions, there is a need for a fuller discussion on many open issues, particularly on collective bargaining.

From IMFSurvey Magazine

IMF staff have taken a fresh look at how labor markets can support workers and growth.

The unemployment rate in advanced economies exceeds 8 percent, with much higher unemployment rates among the young. A third of all young unemployed have been without work for six months or longer.

Countries face the challenge of putting these millions of people back to work and getting the young started in their careers.

Posted by at 5:56 PM

Labels: Inclusive Growth

Subscribe to: Posts