Saturday, December 29, 2012

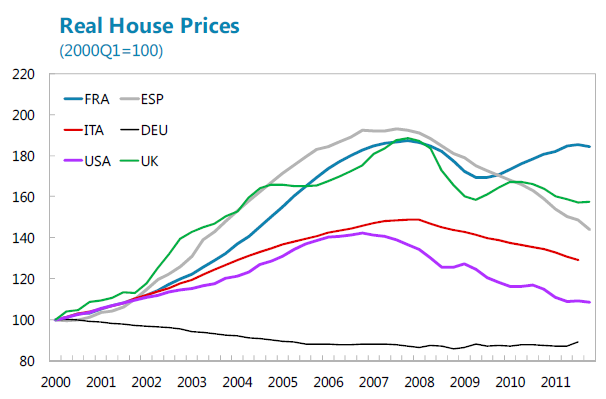

House Prices in France

According to a new report, “Macroeconomic risks related to a correction in real estate prices appear to be relatively contained. The increase in housing prices (over 100 percent in real terms since the mid 1990s) has been supported by stronger fundaments (higher population growth, relatively low supply of housing, and low household indebtedness) than in other countries with rising real estate prices, but also by tax incentives that have fueled demand without addressing underlying supply constraints. There is a perception of price overvaluation, especially in Paris (by 10-20 percent at end-2011 according to staff estimates). However, there is no housing glut or household debt overhang that could trigger a sudden price adjustment. Moreover, stress tests suggest that banks are well placed to absorb the impact of a possible sizable price adjustment owing to tight underwriting criteria (emphasizing sustainability of the borrower’s income, not collateral value) and the absence of nonrecourse loans. The impact of a possible price correction on private demand would also be contained reflecting weak evidence of wealth effects on consumption.”

According to a new report, “Macroeconomic risks related to a correction in real estate prices appear to be relatively contained. The increase in housing prices (over 100 percent in real terms since the mid 1990s) has been supported by stronger fundaments (higher population growth, relatively low supply of housing, and low household indebtedness) than in other countries with rising real estate prices, but also by tax incentives that have fueled demand without addressing underlying supply constraints.

Posted by at 10:25 PM

Labels: Global Housing Watch

Friday, December 28, 2012

Macroprudential Policies and Housing Prices

Several countries in Central, Eastern and Southeastern Europe used a rich set of prudential instruments in response to last decade’s credit and housing boom and bust cycles. A new paper collects detailed information on these policy measures in a comprehensive database covering 16 countries at a quarterly frequency. The authors use this database to investigate whether the policy measures had an impact on housing price inflation. Their evidence suggests that some—but not all—measures did have an impact. These measures were changes in the minimum CAR and non-standard liquidity measures (marginal reserve requirements on foreign funding, marginal reserve requirements linked to credit growth).

Several countries in Central, Eastern and Southeastern Europe used a rich set of prudential instruments in response to last decade’s credit and housing boom and bust cycles. A new paper collects detailed information on these policy measures in a comprehensive database covering 16 countries at a quarterly frequency. The authors use this database to investigate whether the policy measures had an impact on housing price inflation. Their evidence suggests that some—but not all—measures did have an impact.

Posted by at 12:43 AM

Labels: Global Housing Watch

Thursday, December 20, 2012

An assessment of the US jobless recovery through a non-linear Okun’s law

Following the recent financial crisis and its subsequent Great Recession, the issue of a sluggish US employment was raised by economic observers. In a previous post on Econbrowser, Menzie Chinn pointed out the usefulness of the Okun’s law in assessing the potential level of employment after the recession. Especially, Menzie shows that:

- If one does not account for the long-term relationship between GDP and employment (i.e.; if one focuses only on the relationship in differences), then the bounce-back in employment after the 2008-09 recession cannot be captured.

- A standard error-correction model (ECM) is able to reproduce the general evolutions, but misses a large part of the recovery after the end of the recession.

- Accounting for the US business cycle by incorporating a dummy variable that takes the value 1 during recessions and 0 otherwise, according to the NBER Dating Committee dating, enables a better reproduction of stylized facts.

From Econbrowser:

Following the recent financial crisis and its subsequent Great Recession, the issue of a sluggish US employment was raised by economic observers. In a previous post on Econbrowser, Menzie Chinn pointed out the usefulness of the Okun’s law in assessing the potential level of employment after the recession. Especially, Menzie shows that:

- If one does not account for the long-term relationship between GDP and employment (i.e.; if one focuses only on the relationship in differences),

Posted by at 12:34 PM

Labels: Inclusive Growth

Wednesday, December 19, 2012

How the IMF and the World Bank contribute to a job-rich global recovery?

Posted by at 1:23 PM

Labels: Inclusive Growth

Wednesday, December 12, 2012

Seven Questions on Turning Points of the Global Business Cycle

The depth and breadth of the worldwide recession that followed the 2007–09 financial crisis have led to intensive discussions about the phases of the global business cycle—global recessions and global recoveries. The fragile nature of the ensuing global recovery has added a new twist to these discussions because of widespread concerns about the possibility of a double-dip global recession. This article provides brief answers to seven commonly asked questions about the global recessions and recoveries. Read more.

The depth and breadth of the worldwide recession that followed the 2007–09 financial crisis have led to intensive discussions about the phases of the global business cycle—global recessions and global recoveries. The fragile nature of the ensuing global recovery has added a new twist to these discussions because of widespread concerns about the possibility of a double-dip global recession. This article provides brief answers to seven commonly asked questions about the global recessions and recoveries. Read more.

Posted by at 9:54 AM

Labels: Forecasting Forum

Subscribe to: Posts