Wednesday, February 29, 2012

Fred Bergsten: will the euro survive?

Fred Bergsten is the founder of the world’s most influential think tank on international economics, the Peterson Institute. Fred recently announced that he would be stepping down as the Institute’s director. My interview with him covers Fred’s views on whether the euro will survive, but other topics as well—his proposal for a G-2 (a tacit economic club of the U.S. and China to go alongside the G-20), his early work predicting the rise and success of OPEC, and his Cold War with Henry Kissinger. Not many people would have the courage, as Fred did at the age of 30, to quit working for Kissinger telling him: “Henry, you do not seem to need—or deserve—the quality of the advice I am giving you.”

|

| Photo: Michael Spilotro/IMF |

Bergsten on the Euro crisis

The adoption of the euro was a singular event in world monetary history. But most U.S. economists have been skeptical of the euro’s success. Two U.S. economists have bucked the trend: Robert Mundell and Fred Bergsten. Has the euro crisis led Bergsten to change his mind about the euro’s successt?

BERGSTEN: Mundell actually waxed and waned. Sometimes he’s a fixed rate guy. Sometimes he’s a floating rate guy. Anyway, maybe with him as the other exception, I was about the only other American economist that really supported the euro right from the start.

The difference was methodological. The other American economists, including Mundell, based their views on optimal currency areas. They all concluded that Europe was not an optimal currency area and, therefore, the euro was a bad idea.

I came at it with a totally different perspective. This was a political economy perspective. In my jobs in government, but also from outside, I had been actually quite close to the European integration exercise really from the start. And what deeply impressed me was that every time Europe had a crisis, they not only overcame it, they came out stronger. As Monnet said impressively way back at the start, “Europe will be built by crises and it will move forward through crises, but it will always move forward.” And so far he’s been proven right.

And so when you get into this crisis, my mantra is “Watch what they do, not what they say.” And at every stage of this crisis, they have done enough to avoid a collapse — not enough to sway the market, but mind you that’s because they can’t say to the markets what they are going to do, because then that would take all the pressure off the other countries and it would be a moral hazard.

So they’re playing a risky game, but again, based on this political kind of motive, I say very strongly Germany will pay whatever it has to pay, both because of that continuing geo-strategic imperative, but also now because the euro is so hugely important to Germany’s economy. The ECB will discount to whatever extent it has to to avoid a collapse even though they can’t say that they’ll do it and, therefore, can’t give the markets the assurance they want.

So I’m actually quite confident still, despite all the rumor mills, that the euro will survive. There will be no widespread defaults. The Greeks might have to, but you might say they’ve already defaulted a lot.

And, even more importantly I’m convinced Europe will come out of it stronger When they created the so-called economic and monetary union they were pretty complete with the monetary union, but there was no economic union. So it was a half-way house, it had to be reconciled sometime. Either you had to forget about the euro or you had to create an economic union. And I’m convinced they will never, never, never let the euro just fail.

Therefore, they have to create an economic union, and I’m convinced that all the steps that they’re taking now — the EFSF, the successor mechanism, the economic governing systems they’re setting up, Merkel’s calls for a political union — I think all that’s leading toward a full economic union. And five years from now — I think it will take years and it it’ll take key Constitutional amendments — they’ll have it.

|

| Photo: Michael Spilotro/IMF |

**

Read the full interview here. The interview was conducted on December 22, 2011 for a profile of Fred that just appeared in the IMF’s magazine Finance & Development.

Fred Bergsten is the founder of the world’s most influential think tank on international economics, the Peterson Institute. Fred recently announced that he would be stepping down as the Institute’s director. My interview with him covers Fred’s views on whether the euro will survive, but other topics as well—his proposal for a G-2 (a tacit economic club of the U.S. and China to go alongside the G-20), his early work predicting the rise and success of OPEC,

Posted by at 5:57 PM

Labels: Profiles of Economists

Monday, February 13, 2012

BP’s Cheerful Energy Outlook for 2030

BP has a surprisingly cheerful energy outlook for 2030.

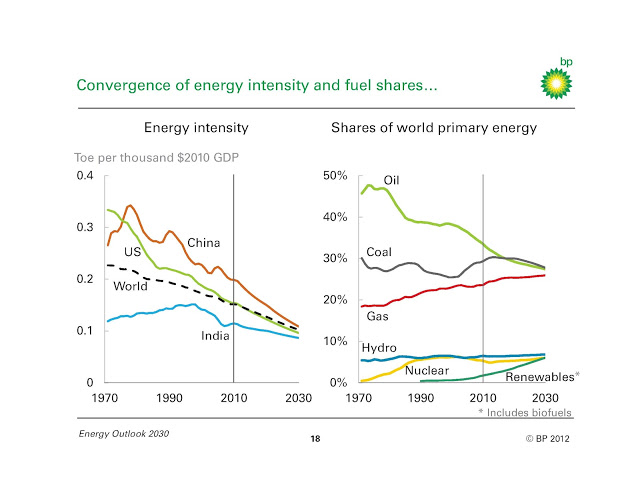

Energy intensity—the amount of energy it takes to produce a dollar of income—has been continuing a steady downward march for 40 years, and BP expects this to continue. By 2030, the major regions of the world—the U.S., China and India—will have the same energy intensity. Energy use will be diversified across sources: oil, coal, and gas will each have a 30% market share, with hydro, nuclear and renewables accounting for the remaining 10%.

Energy supply from the Americas—US and Brazilian biofuels, Canadian oil sands, Brazilian deepwater and US shale oil—will help in balancing supply and demand in 2030.

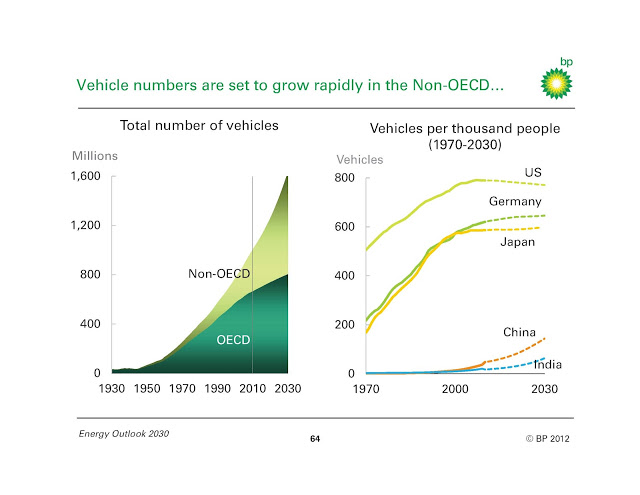

Vehicle ownership (per person) will hit saturation in the rich nations. And while it will grow in China and India, it will follow a slower path than seen historically in other countries.

If we could keep politics out of the picture, we could have an energy outlook by 2030 in which the America are largely energy self-sufficient, the FSU supplies nearby Europe, and the Mid-East and Africa take care of the needs of the Asia-Pacific.

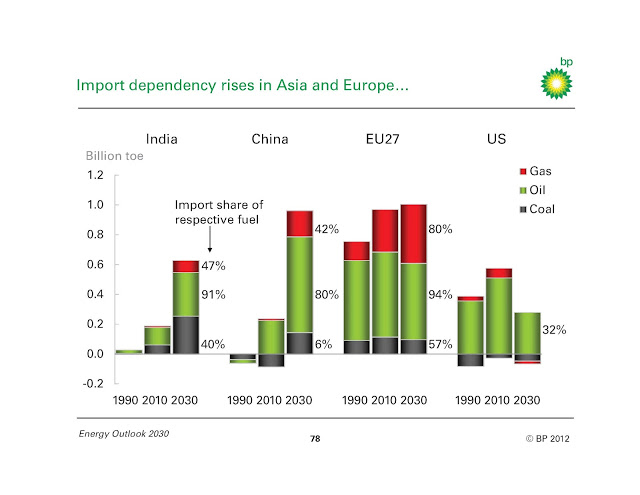

Import dependence in 2030 is projected to be higher than it is today for all major energy importers—Europe, China and India—but will decline for the United States. BP predicts that by 2030 “the import share of oil demand and the volume of oil imports in the US will fall below the 1990s levels, largely due to rising domestic shale oil production and ethanol displacing crude imports. The US will also become a net exporter of natural gas.”

BP has a surprisingly cheerful energy outlook for 2030.

Energy intensity—the amount of energy it takes to produce a dollar of income—has been continuing a steady downward march for 40 years, and BP expects this to continue. By 2030, the major regions of the world—the U.S., China and India—will have the same energy intensity. Energy use will be diversified across sources: oil, coal, and gas will each have a 30% market share,

Posted by at 1:33 AM

Labels: Energy & Climate Change

Friday, February 10, 2012

House Prices in Singapore

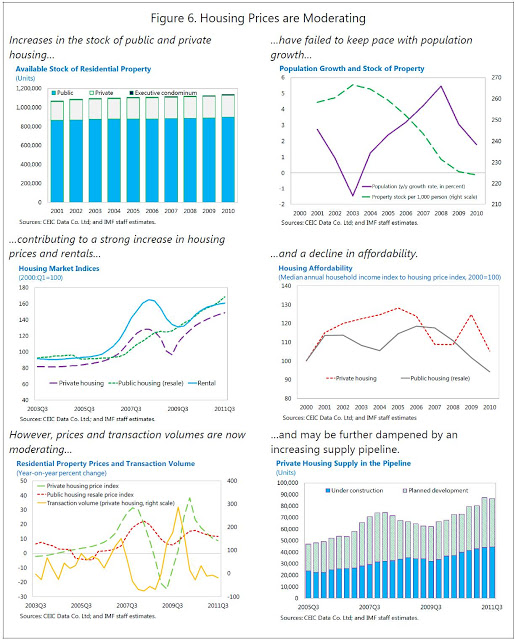

“Following a steep decline in 2008−09, private residential property prices rebounded strongly and are now above the previous peak. Public housing resale prices, which were more resilient during the crisis, are also growing rapidly, and this has allowed many owners to sell and upgrade into private housing, contributing to price pressures in that market. House prices have outpaced median household incomes, leading to a decline in home affordability, which has become a prominent social issue.

Property prices have been propelled by:

- A resurgent economy, which has buoyed incomes.

- Low interest rates. Real mortgage rates have been very low or negative for the past two years, leading to high housing credit growth rates.

- Supply constraints. Housing supply has not kept pace with population growth, which has been driven up by strong immigration.

- Demand by nonresidents. A booming economy and prospects of currency appreciation, along with Singapore’s strong investment climate, have lured foreign interest in the housing market.

Between September 2009 and January 2011, the authorities adopted four rounds of measures to contain demand, including the introduction (and subsequent tightening) of seller stamp duties, and lowering of LTV caps on private property loans. In a fifth round in December 2011, they introduced an additional buyer’s stamp duty, aimed at curbing investment demand, particularly from foreigners and corporate. The authorities have also undertaken measures to increase the supply of public and private housing

Staff analysis suggests that the measures undertaken by the authorities through January 2011 have helped contain prices and transaction volumes in the housing market, both of which are now moderating. Along with slower domestic growth, an uncertain outlook, and a significant supply pipeline of public and private housing projects (although residential construction activity is slowing), the housing market was already likely to cool further. The latest measures in December 2011 took markets by surprise and shifted the balance of risks further downward. Because these measures are residency˗based and focus on the housing market, they also carry some risk of pushing foreign demand over to commercial and industrial property markets (which are also experiencing price increases) or to other countries.”

The IMF report notes:

“Following a steep decline in 2008−09, private residential property prices rebounded strongly and are now above the previous peak. Public housing resale prices, which were more resilient during the crisis, are also growing rapidly, and this has allowed many owners to sell and upgrade into private housing, contributing to price pressures in that market. House prices have outpaced median household incomes, leading to a decline in home affordability, which has become a prominent social issue.

Posted by at 10:02 PM

Labels: Global Housing Watch

House Prices in Lebanon

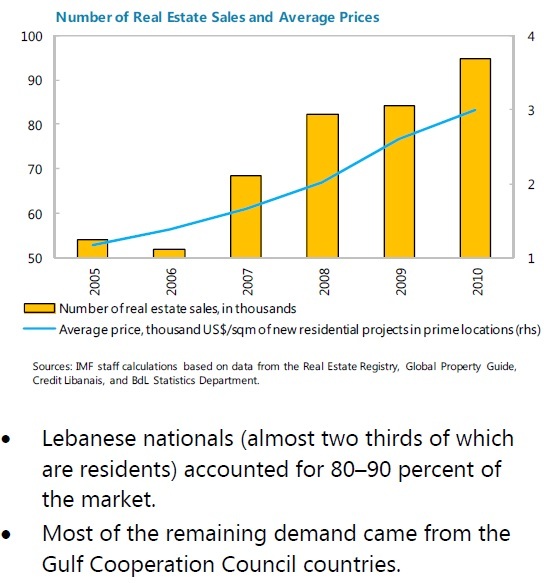

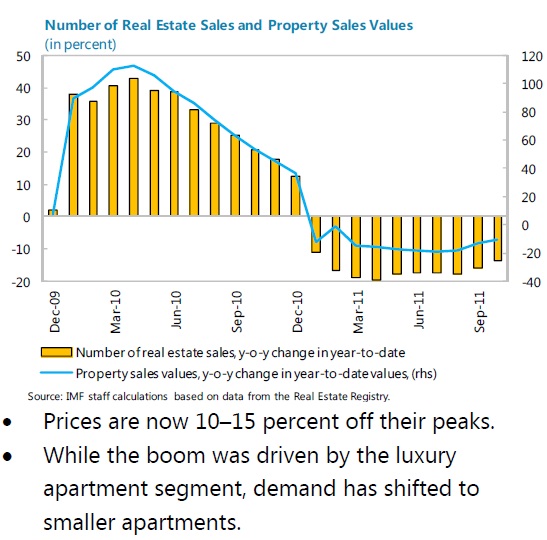

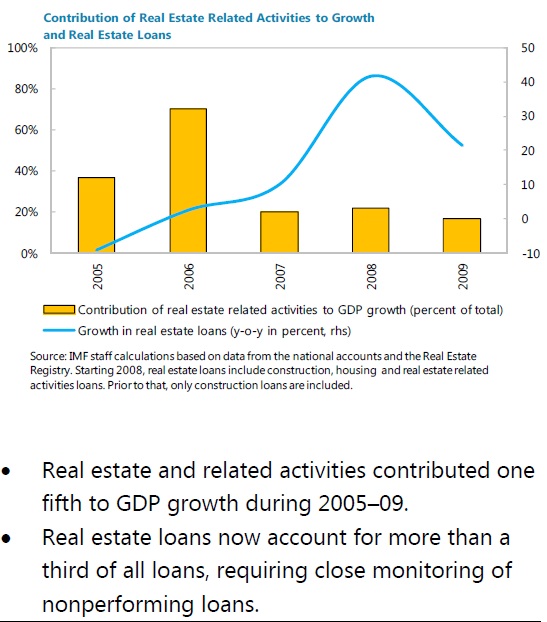

The IMF notes: “Real estate boomed during 2006-09, but the market started to correct in mid-2010. The correction is adversely affecting the economy, but could bring prices more in line with the region.”

The IMF notes: “Real estate boomed during 2006-09, but the market started to correct in mid-2010. The correction is adversely affecting the economy, but could bring prices more in line with the region.”

Posted by at 12:19 AM

Labels: Global Housing Watch

Thursday, February 2, 2012

House Prices in Norway

IMF staff report says:

- Over the last two years Norway has seen one of the most rapid paces of real house price appreciation in the OECD.

- Housing valuations continue to appear on the high side. Standard metrics, such as price-to-rent and price-to-income ratios, indicate a risk of overvaluation.

- The ratio of house prices to rents has risen sharply during the boom and is now nearly 70 percent above its historical average—the highest such deviation in any OECD country.

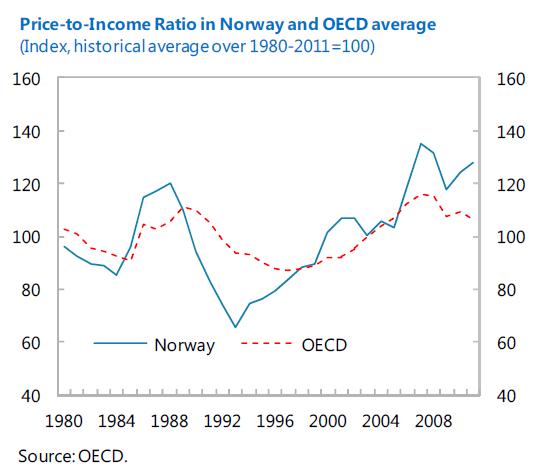

- The house price-to-income ratio has also been rising. This ratio is now 28 percent above its historical average—higher than the peak reached before the last major house price bust in Norway two decades ago.

- While fundamentals explain part of the boom, signs also point to risks of overvaluation. On balance, model based estimates from the IMF’s Early Warning Exercise (EWE), which take into account the key determinants of house prices, suggest that Norwegian residential property prices may be misaligned by 15-20 percent. However, there is admittedly a high amount of uncertainty around this estimate in both directions.

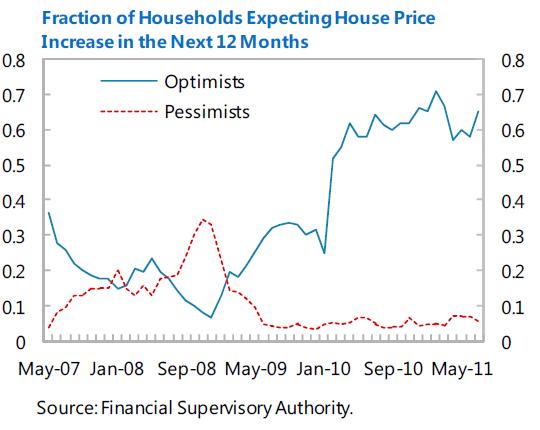

- Expectations of increasing prices may lead agents to buy for speculative motives. An increasing number of households believe that property prices will continue to appreciate. (…) Today, 70 percent of the survey respondents expect price to increase over the next 12 months.

- Another candidate for explaining the boom is loose credit conditions. (…) the share of mortgages with loan-to-value (LTV) ratios over 90 percent has been high since data were first collected in the late 1990s, after the boom was already underway. However, it is somewhat worrisome that the share of mortgages with LTVs over 90 percent has increased since 2010, despite the issuance of FSA guidelines recommending against allowing LTVs to exceed this level, other than in exceptional circumstances.

- About 95 percent of mortgages loans are adjustable-rate and interest payments are front-loaded, low interest rates have made mortgages cheaper and homes significantly more affordable.

- Total household mortgage debt as a fraction of disposable income has increased to 195 percent by end-2010.

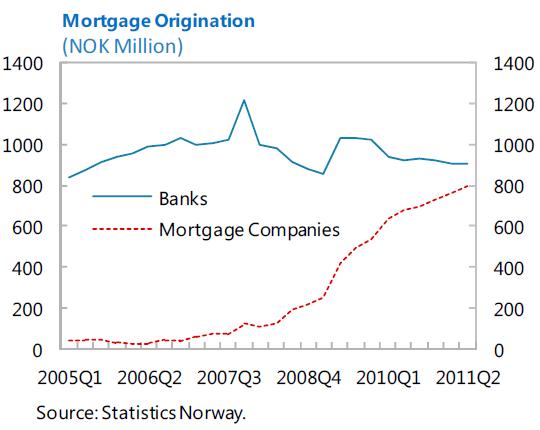

- The volume of secured loans issued by mortgage companies has picked up considerably since 2008. In 2011, loans from mortgage companies represented nearly 50 percent of new mortgages.

- Owner-occupied housing receives quite generous tax treatment in Norway.

- A house price bust would likely be associated with depressed economic activity and increased financial sector stress, especially given high levels of mortgage debt.

- The estimates suggest that a 10 per cent drop in real house prices in Norway is associated with roughly 1 percentage point lower GDP growth than otherwise. (…) A correction of 30 percent in house prices—as occurred during the crisis in the 90s—would exert a non-negligible effect to the real economy.

IMF staff report says:

- Over the last two years Norway has seen one of the most rapid paces of real house price appreciation in the OECD.

- Housing valuations continue to appear on the high side. Standard metrics, such as price-to-rent and price-to-income ratios, indicate a risk of overvaluation.

- The ratio of house prices to rents has risen sharply during the boom and is now nearly 70 percent above its historical average—the highest such deviation in any OECD country.

Posted by at 3:36 PM

Labels: Global Housing Watch

Subscribe to: Posts