Saturday, December 31, 2011

In Memoriam: All Economists Great and Small

A brief remembrance of four economists who passed away in 2011: Anand Chandavarkar, Alan Stockman, David Aschauer and Ioannis Tokatlidis

- Anand Chandarvarkar was an illustrious Indian economist, known for his books on Keynes and on central banking in developing economies. My review of Anand’s book on Keynes gives you a flavor of Anand’s scholarship, but an excellent look back at his work and career can be found in a piece in the Economic & Political Weekly by his friend and noted economist Deena Khatkhate.

- Alan Stockman, one of my professors at Rochester, was a noted international economist and a wonderful teacher of introductory economics. I was one of the army of RAs for Alan’s principles of econ course. An obit and a nice tribute from Maury Obstfeld.

- David Aschauer was a classmate at Rochester. He and I went through the bonding experience of failing our macro qualifying exam together on our first try. He later got me into the Chicago Fed when I got tired of a being in a long-distance marriage and wanted to move from Florida to Chicago to be closer to my wife. The Boston Globe had a nice obit piece on David.

- Ioannis Tokatlidis (“Yannis”) was a colleague in the IMF’s Research Department. He served — with great distinction — several IMF chief economists, including Raghu Rajan (with whom he had co-authored some papers such as this one), Simon Johnson and Olivier Blanchard. Though a fine economist in his own right, Yannis devoted his life to making other people’s research better.

A brief remembrance of four economists who passed away in 2011: Anand Chandavarkar, Alan Stockman, David Aschauer and Ioannis Tokatlidis

- Anand Chandarvarkar was an illustrious Indian economist, known for his books on Keynes and on central banking in developing economies. My review of Anand’s book on Keynes gives you a flavor of Anand’s scholarship, but an excellent look back at his work and career can be found in a piece in the Economic &

Posted by at 1:19 AM

Labels: Profiles of Economists

Saturday, December 24, 2011

More Housing Woes on the Horizon?

As the United States continues to grapple with the fallout of its housing bubble and blow-up, recent research from the International Monetary Fund uncovers some startling statistics about other countries that could be headed toward their own U.S.-style housing crises.

While home prices have fallen in about half of the countries the IMF tracks, they’ve risen in the other half. Those trends coupled with data used to gauge the affordability of housing and whether homes are valued correctly seems to indicate prices have significant room to fall.

In other words, home values in many countries are inflating much like the run-up the U.S. saw in the early 2000s and could be headed for a correction.

Continue reading here.

Meg Handley of U.S. News writes

As the United States continues to grapple with the fallout of its housing bubble and blow-up, recent research from the International Monetary Fund uncovers some startling statistics about other countries that could be headed toward their own U.S.-style housing crises.

While home prices have fallen in about half of the countries the IMF tracks, they’ve risen in the other half.

Posted by at 12:38 AM

Labels: Global Housing Watch

Thursday, December 22, 2011

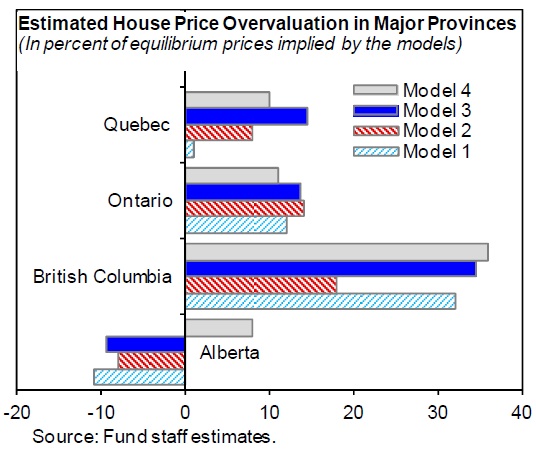

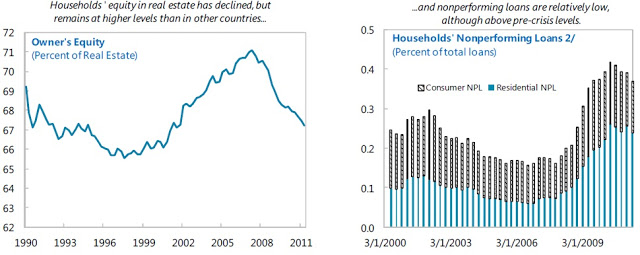

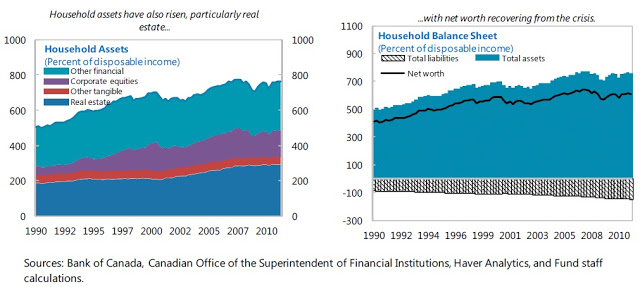

House Prices in Canada

What’s likely to happen to house prices in Canada? Are house prices more out of whack with fundamentals in British Columbia than in Ontario or Alberta? And what would the consequences be for the economy if house prices fell?

The IMF’s economic outlook for Canada has an extensive discussion of prospects for the Canadian housing market. IMF staff noted that “the [house] price-to-rent and [house] price-to-income ratios are 29 percent and 20 percent above their averages for the last decade, respectively”. My earlier post compares Canadian ratios to those in the U.S. and Europe.

IMF staff said that “while there are structural factors that can explain increases in such ratios, their elevated level and other empirical evidence suggest that house prices may be higher than justified by underlying fundamentals, at least in some provinces—staff estimates indicate an average price overvaluation of around 10 percent, with significant regional differences.”

A companion paper estimates “house prices in 2011 to be above the levels consistent with the current levels of fundamentals in British Columbia, with some signs of overvaluation also in Ontario, and to a lesser degree, in Quebec. By contrast, the estimated models suggest house prices to be mildly undervalued in Alberta.” Averaging these estimates (with weights based on provincial GDP levels), the paper suggests “that house prices in Canada are on average ten percent above the level consistent with current fundamentals.”

The companion paper also studied “the impact of a potential correction in house prices on consumption through household wealth effects.” The paper’s authors concluded that the “empirical estimates suggest that a ten percent decline in house prices would lead to a 1¼ percent decline in private consumption.”

The full report can be found here. In it, IMF staff noted that “to ensure the long-term stability of housing markets” the Canadian government has “increased public awareness of the risks and … tightened mortgage insurance standards several times since 2008.”

What’s likely to happen to house prices in Canada? Are house prices more out of whack with fundamentals in British Columbia than in Ontario or Alberta? And what would the consequences be for the economy if house prices fell?

The IMF’s economic outlook for Canada has an extensive discussion of prospects for the Canadian housing market. IMF staff noted that “the [house] price-to-rent and [house] price-to-income ratios are 29 percent and 20 percent above their averages for the last decade,

Posted by at 10:32 PM

Labels: Global Housing Watch

Tuesday, December 20, 2011

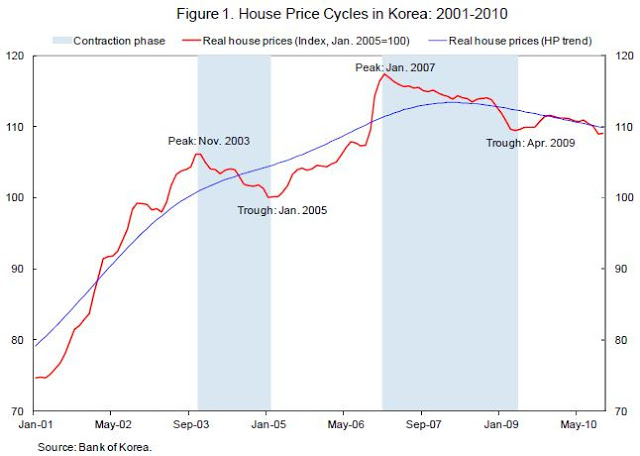

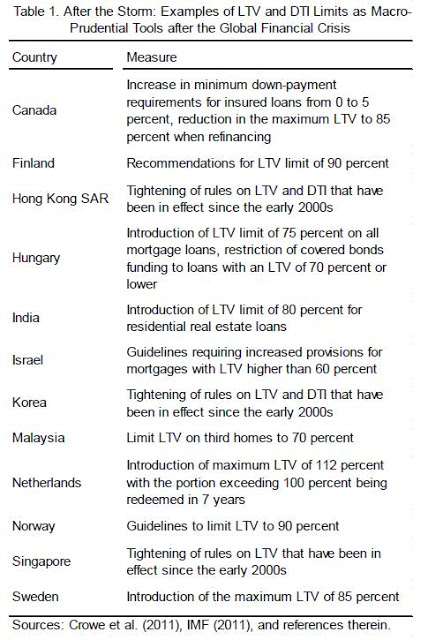

Housing Market in Korea

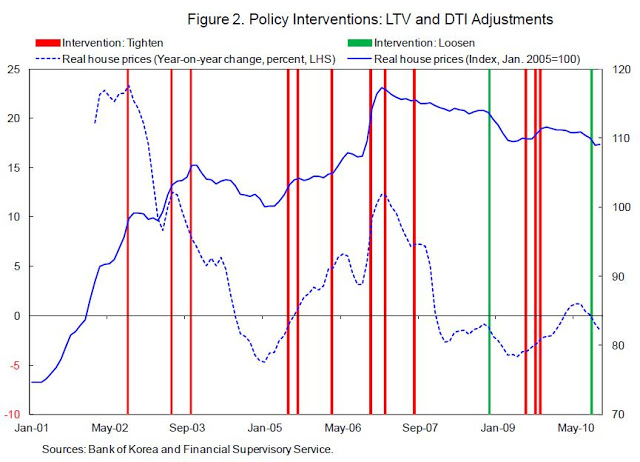

An interesting paper by my IMF colleagues Deniz Igan and Heedon Kang looks at how limits on loan-to-value ratios and debt-to-income ratios affect the housing market in Korea.

“Prior to the crisis, when it came to dealing with asset price booms, the widely-accepted tenet was one of ‘benign neglect’, namely, to wait for the bust and pick up the pieces (Bernanke and Gertler, 2001). Yet, the crisis and its formidable costs shifted the balance to the opposite camp favoring pre-emptive policy actions that could stop bubbles or, at least, could contain the damage to the financial sector and the broader economy when the bust comes. In other words, many policymakers now think that it is better to act than wait on the sidelines because the cost of inaction may greatly exceed the potential negative side effects of policy intervention. (…) In the quest to better design the policy toolkit to deal with real estate booms and busts, macroprudential tools such as maximum limits on loan-to-value ratios (LTV) and debt-to-income ratios (DTI) are heavily advocated. This has led several countries to recently adopt such limits or measures that would discourage high-LTV/DTI loans.”

Korea is one of a dozen countries that have adopted such limits.

“we know little about the impact of these measures that have become popular with many regulators after the crisis. Theoretically, limits on LTV and DTI can kill two birds with one stone: they can curb the feedback loop between mortgage credit availability and house price appreciation, and, by restraining household leverage, they can help reduce the incidence and loss given default of residential mortgage loan delinquencies.”

The paper asks two questions

“First, what happens when LTV/DTI limits are adjusted in response to developments perceived to be risky? Second, can we quantify the impact of LTV and DTI limits on housing and mortgage activity?”

What are their conclusions? Igan and Kang find that

“transaction activity drops significantly in the three-month period following the tightening of LTV/DTI regulations. Price appreciation slows down a bit later, in a six-month window rather than the three-month window. Moreover, price dynamics appear to be reined in more after LTV tightening rather than DTI tightening. [The authors provide evidence for what the] channel for the impact of the policy actions may be: expected house price increases in the future become lower after policy intervention and this is more prevalent among older households while plans to purchase of a home are more likely to be postponed by those who already own a property, i.e., potential speculators, but not by those who do not own a property, i.e., potential first-time home buyers. These findings suggest that tighter limits on loan eligibility criteria, especially on LTV, curb expectations and speculative incentives. Policy implications of our analysis are encouraging. In housing markets, expectations are key as they often facilitate the settling in of bubble dynamics. If, as suggested by the evidence presented here, limits on LTV curb expectations and discourage potential speculators, they can be effective tools to tame real estate booms and contain the associated risks.”

An interesting paper by my IMF colleagues Deniz Igan and Heedon Kang looks at how limits on loan-to-value ratios and debt-to-income ratios affect the housing market in Korea.

Igan and Kang write

“Prior to the crisis, when it came to dealing with asset price booms, the widely-accepted tenet was one of ‘benign neglect’, namely, to wait for the bust and pick up the pieces (Bernanke and Gertler, 2001).

Posted by at 10:08 PM

Labels: Global Housing Watch

Thursday, December 15, 2011

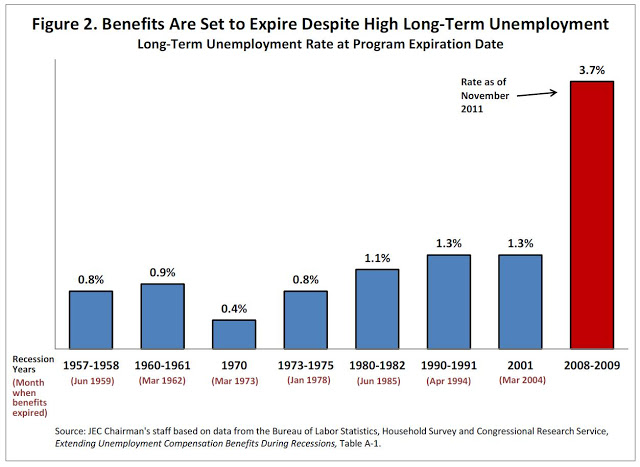

JEC Report Highlights Critical Role of Unemployment Insurance

A new report from the U.S. Congress Joint Economic Committee (JEC) finds that if federal UI benefits are allowed to expire, over 2 million long‐term unemployed workers stand to lose their benefits in early 2012. That number could grow to 5 million before the end of 2012.

Entitled “The Case for Maintaining Unemployment Insurance: Supporting Workers and Strengthening the Economy,” the report finds that at 3.7 percent, the current long-term unemployment rate is nearly three times higher than it has ever been when Congress let federal benefits expire.

“Unemployment benefits serve as a critical lifeline to workers and their families in the face of a sudden and severe drop in income,” said Senator Bob Casey, Chairman of the JEC. “These benefits help struggling families pay for their necessities such as food, housing, clothing, and utilities—obligations that continue even when a family member loses a job.”

On average these benefits only meet half of basic household expenditures but they kept over 3 million Americans out of poverty in 2010. Research shows that extending federal UI benefits during periods of high unemployment works to pull the economy back from a downward spiral whereby reduced consumer demand leads to further reductions in economic activity, and that in turn leads to more job losses.

“Continuing the current emergency federal UI programs is vital to the economic recovery. A temporary reauthorization would not only give millions of struggling long-term unemployed Americans a lifeline, it would bolster the economic recovery by generating jobs and accelerating economic growth. Washington must put aside partisan bickering and give American families the help they need to stay on their feet,” said Casey.

Report highlights include:

- Over 40 percent of the unemployed have been without a job for at least six months, and over 30 percent have been unemployed for at least one year. Letting emergency federal benefits expire now would be unprecedented and could derail the recovery.

- Even without lengthening the maximum allowable duration of benefits, continuing federal benefits could generate up to 400,000 jobs. The boost to the economy from additional spending on UI benefits is estimated to be as large as $1.90 for each dollar of assistance—the greatest “bang-for-the-buck” among a range of fiscal policies designed to boost gross domestic product (GDP) and create jobs, according to the non-partisan Congressional Budget Office (CBO).

- Claims that extended UI benefits deter unemployed workers from looking for work are unfounded. On the contrary, beneficiaries of federal UI benefits have spent more time searching for work than those who were ineligible for UI benefits. Studies find the impact of additional benefits on the unemployment rate to be small.

- Any increase in the unemployment rate because of federal UI benefits is most likely because the beneficiaries remain attached to the labor force and continue to search for work, not because they refuse employment or do not search for a job.

A new report from the U.S. Congress Joint Economic Committee (JEC) finds that if federal UI benefits are allowed to expire, over 2 million long‐term unemployed workers stand to lose their benefits in early 2012. That number could grow to 5 million before the end of 2012.

Entitled “The Case for Maintaining Unemployment Insurance: Supporting Workers and Strengthening the Economy,” the report finds that at 3.7 percent,

Posted by at 10:28 PM

Labels: Inclusive Growth

Subscribe to: Posts