Showing posts with label Macro Demystified. Show all posts

Monday, August 1, 2022

Is this a recession?

From Econbrowser:

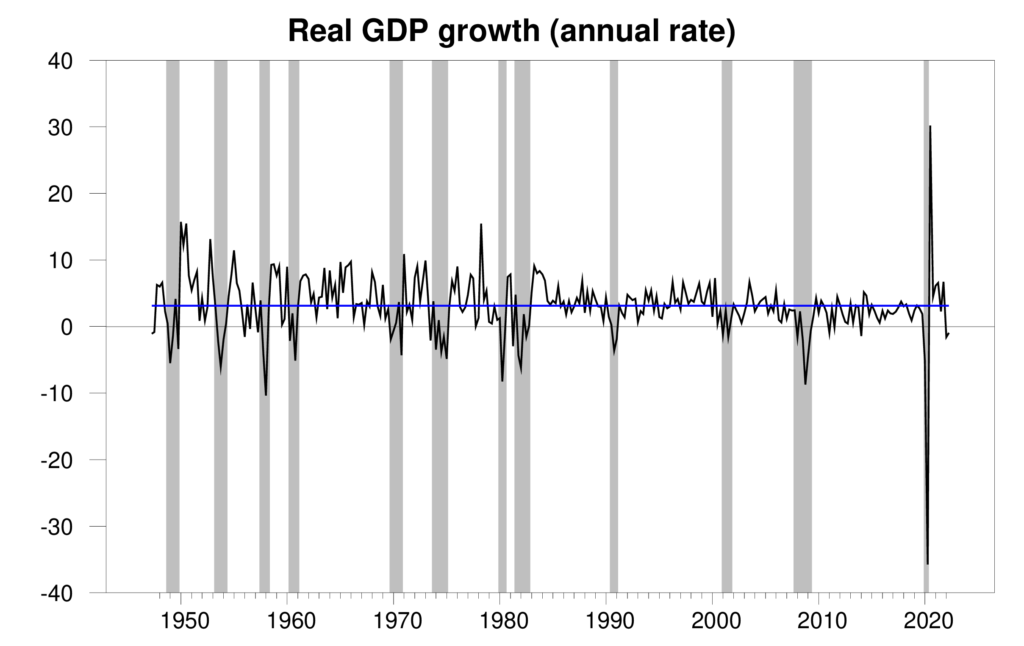

“The Bureau of Economic Analysis announced today that seasonally adjusted U.S. real GDP fell at a 0.9% annual rate in the first quarter. That makes two quarters in a row of falling real GDP, which is one rule of thumb for declaring the economy to be in a recession. The current economic weakness could certainly develop into a recession. But the evidence isn’t convincing that a recession is already under way.

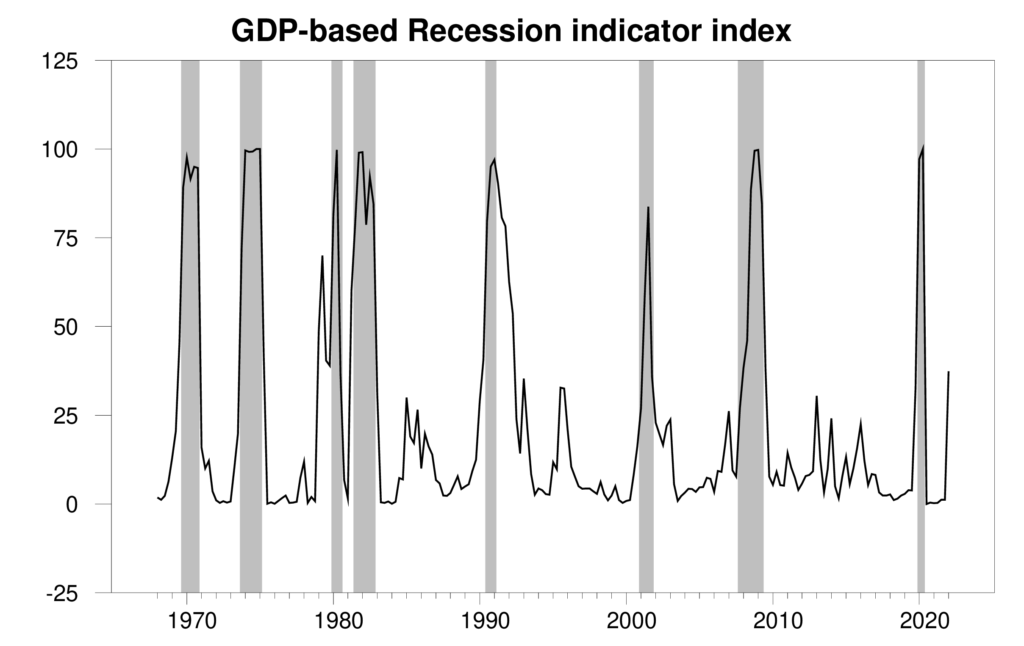

The new data raised the Econbrowser recession indicator index up to 37.4%, flashing a clear warning sign. This is an assessment of the situation of the economy in the previous quarter (namely 2022:Q1). The index takes into account the fact that we’ve now seen two consecutive quarters of falling GDP, but still finds the evidence inconclusive as to whether the U.S. economy started a recession in the first quarter. When Marcelle Chauvet and I first developed this index 17 years ago, we announced that we would only declare a recession to have started when the index rises to 65% (see pages 14-15 in our original paper). If the Q3 GDP report causes the index to rise above 65%, we would announce a recession at that time, and also use the full range of revised historical data available at that time to determine the date at which the recession likely started. Here at Econbrowser we’ve followed that procedure to the letter as the data unfolded in real time over the last 17 years, successfully dating in real time the beginning and end of the two recessions since we started this blog.”

Continue reading here.

From Econbrowser:

“The Bureau of Economic Analysis announced today that seasonally adjusted U.S. real GDP fell at a 0.9% annual rate in the first quarter. That makes two quarters in a row of falling real GDP, which is one rule of thumb for declaring the economy to be in a recession. The current economic weakness could certainly develop into a recession. But the evidence isn’t convincing that a recession is already under way.

Posted by at 8:22 AM

Labels: Macro Demystified

Wednesday, July 20, 2022

The end of privilege: A re-examination of the net foreign asset position of the US

A VoxEU article by Andy Atkeson, Jonathan Heathcote, Fabrizio Perri:

“The US net foreign asset position – measuring the difference between its foreign assets and liabilities – was negative, yet small, until 2007. This column shows that since then, it has deteriorated sharply to negative 40% of GDP, mostly as a result of changes in the market value of US-owned assets abroad and foreign-owned assets in the US. These valuation effects are explained by rising US equity values disproportionately benefitting foreign owners of US firms. Whether this is beneficial for depends on whether the profit rises are due to higher productivity or lower competition.

A country’s net foreign asset position measures the value of all the assets residents own abroad minus the value of assets foreigners own in the country. It is an important statistic, because all else equal, a higher net foreign asset position means a country can expect higher future net income from abroad, and can thus plan on running larger future trade deficits. One common way to decompose changes in the net foreign asset position is to recognise that the position can improve because a country, on net, acquires additional foreign assets – i.e. it runs a current account surplus – or because the market value of existing assets owned abroad increases relative to the value of foreign-owned assets in the country.

The US has long had a negative net foreign asset position. But until 2007 it was relatively small, never exceeding 20% of US GDP. In fact, the position was surprisingly small given the US history of large and persistent current account deficits. In influential papers, Gourinchas and Rey (2007, 2014) emphasised the importance of valuation effects in shaping the dynamics of the US net foreign asset position. At the time they were writing, these revaluations seemed to move consistently in favour of the US, especially during the mid-2000s. The net effect was that the US appeared to enjoy the special privilege of being consistently able to borrow without running up much debt. Gourinchas and Rey and others argued that this privilege reflected an asymmetry in cross-country portfolios, with Americans owning lots of direct investment and portfolio equity assets abroad – whose value tended to rise over time – while US liabilities consisted disproportionately of low return US government bonds.

Our paper (Atkeson et al. 2022) updates the history of the US net foreign asset position, using data assembled by the US Bureau of Economic Analysis and the US Treasury in the Financial Accounts of the United States. We find that a lot has changed in the last 15 years. First and most notably, the US net foreign asset position has deteriorated very sharply, from negative 5% of US GDP in 2007, to negative 65% of US GDP by the third quarter of 2021. Such a large negative net position is unprecedented. What has driven this decline? What are the welfare implications for Americans?”

Continue reading here.

A VoxEU article by Andy Atkeson, Jonathan Heathcote, Fabrizio Perri:

“The US net foreign asset position – measuring the difference between its foreign assets and liabilities – was negative, yet small, until 2007. This column shows that since then, it has deteriorated sharply to negative 40% of GDP, mostly as a result of changes in the market value of US-owned assets abroad and foreign-owned assets in the US. These valuation effects are explained by rising US equity values disproportionately benefitting foreign owners of US firms.

Posted by at 7:36 AM

Labels: Macro Demystified

Tuesday, July 12, 2022

Pandemic Policy: Support Jobs or Workers?

From Conversable Economist:

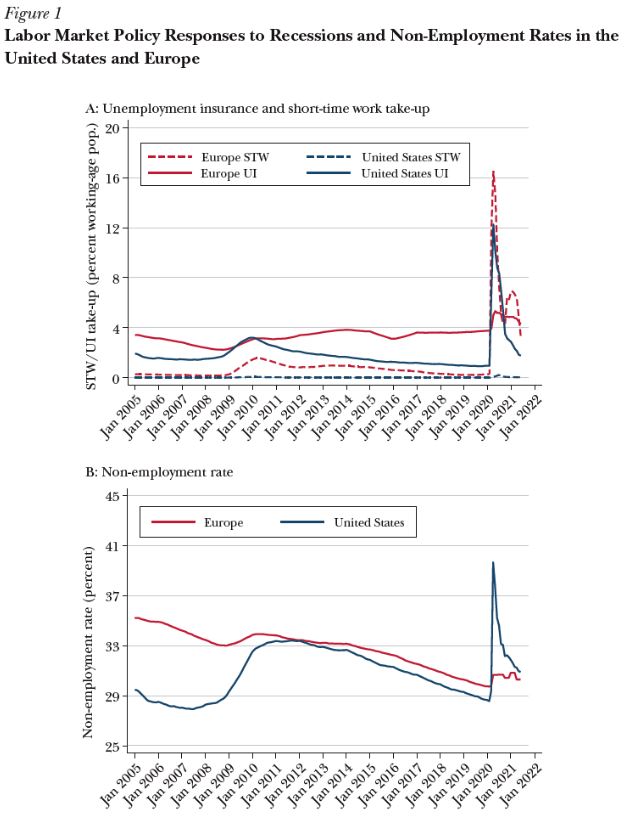

“The pandemic recession from March to April 2020 was a different creature from the previous post World-War II recessions: different in cause, length, depth, and the kinds of social and economic changes that happened. The appropriate economic policy response was also different. Instead of the standard anti-recession policy of stimulating the entire economy, it is more useful to think of pandemic recession policy as a form of social insurance. One key question is whether this social insurance should operated primarily by supporting the unemployed or by supporting jobs.

Lest this distinction sound like a word game, consider this real world difference. In the pandemic, most European countries responded with programs of “short-time work.” The idea the employer doesn’t need to fire or lay-off workers. Instead, it cuts their hours substantially, and the government makes up the difference. It’s a kind of partial unemployment, except that when the worst of short, sharp pandemic hit to the economy passed by, the workers were still employed at their previous jobs and employers could ramp up their hours again. In contrast, the US approach emphasized larger and longer unemployment payment aimed at those who were without jobs. US employers (with the exception of some small state-level programs) did not have option of switching to short-time work.

Giulia Giupponi, Camille Landais, and Alice Lapeyre discuss the tradeoffs between tehse two approaches in “Should We Insure Workers or Jobs during Recessions?” (Spring 2022, Journal of Economic Perspectives, 36:2, 29-54). Here’s one of their figures. The solid lines show the share of population receiving unemployment insurance, with the blue line showing the US and the red line showing a weighted average for Germany, France, Italy, and the United Kingdom. Notice that the share of workers getting unemployment insurance in the pandemic spikes up in the US (solid blue line) but barely budges in the European countries (solid red line). Conversely, the share of workers on short-time work spikes up in the European countries (dashed red line) but barely budgets in the US (dashed blue line).”

From Conversable Economist:

“The pandemic recession from March to April 2020 was a different creature from the previous post World-War II recessions: different in cause, length, depth, and the kinds of social and economic changes that happened. The appropriate economic policy response was also different. Instead of the standard anti-recession policy of stimulating the entire economy, it is more useful to think of pandemic recession policy as a form of social insurance.

Posted by at 7:39 AM

Labels: Inclusive Growth, Macro Demystified

Sunday, July 3, 2022

How the World Became Rich: The Historical Origins of Economic Growth

From Economic History Association:

“Mark Koyama and Jared Rubin. How the World Became Rich: The Historical Origins of Economic Growth. Cambridge, UK: Polity Press. x + 259 pp. $24.95 (paperback), ISBN 978-1509540235.

Reviewed for EH.Net by Joel Mokyr, Departments of Economics and History, Northwestern University.

Any scholar teaching economic history and wishing for an up-to-date survey of a large and important literature will find it useful to read this book to bone up on the recent research listed in the long and encompassing list of references. Furthermore, they should seriously consider having their students read it for their class. The book is a wide-ranging yet remarkably complete and accessible survey of the Great Enrichment, the emergence of modern and prosperous economies that provide us with a material standard of living that our ancestors could not have dreamed of. How and why modern economic growth occurred when and where it did, and how economists have tried to understand this phenomenon, is the theme of this book. It is written by two of the finest young senior scholars in our field, both with important contributions to the subject matter of this book.

Many of the issues this book raises are highly contentious in our profession, and for good reason: these are hard questions on which learned scholars can disagree and interpret the evidence in different ways. How much did institutions really matter? What was the role of culture in economic growth? Was geography destiny? What was the role of craft guilds in the economic development of early modern Europe? How to think about the role of imperialism and slavery in the Industrial Revolution and the subsequent growth of industrial powers? Were high wages good or bad for technological progress? Was war a positive factor in economic growth? Was the European Marriage Pattern a positive factor in the economic development of the Continent?

The ecumenical and balanced approach the authors take to these questions is much like the Rabbi in a famous Jewish story. According to the legend, a rabbi is holding court in front of a large audience of his pupils. A husband and wife appear before the rabbi, to discuss their troubled domestic life. First the husband gets to lay out his case, and he lists all the sins and vices of his wife. The Rabbi listens carefully and pronounces his verdict: the husband is in the right. Then his pupils appeal to him: you should hear the wife’s case as well. The Rabbi consents and listens to the woman lays out her powerful case against her lazy and violent husband. He then announces his second verdict: the wife is in the right. His best pupil protests: but Rabbi, how can they both be in the right? The Rabbi listens and pronounces: the pupil is right too.

Rubin and Koyama present balanced and fair surveys of made in the literature, but they are reluctant to take strong positions. Such an ecumenical approach sets them apart from Clark’s Farewell to Alms and McCloskey’s Bourgeois Dignity, where the authors take up similar issues but in a much stronger opinionated mode. That thoughtful and measured approach of the survey, its elegant and crystal-clear style, and the authors’ impressive knowledge of a large and complex literature make this book nothing short of ideal for teaching advanced courses on global economic history to economics students.

It is especially refreshing to see a book such as this that pays explicit attention to institutions and culture, two themes that until not so long ago were taboo in our field but now seem to play increasingly central roles. The book contains full chapters on each, and while the discussion is naturally far from exhaustive, the authors do an excellent job summarizing some of the best work in these areas. What remains, of course, unsolved is why different nations develop different institutions and how and why such institutions change over time and how exactly cultural beliefs help determine the institutions that society ends up with.”

Continue reading here.

From Economic History Association:

“Mark Koyama and Jared Rubin. How the World Became Rich: The Historical Origins of Economic Growth. Cambridge, UK: Polity Press. x + 259 pp. $24.95 (paperback), ISBN 978-1509540235.

Reviewed for EH.Net by Joel Mokyr, Departments of Economics and History, Northwestern University.

Any scholar teaching economic history and wishing for an up-to-date survey of a large and important literature will find it useful to read this book to bone up on the recent research listed in the long and encompassing list of references.

Posted by at 9:32 AM

Labels: Book Reviews, Macro Demystified

Tuesday, June 14, 2022

Some Stock Market Benchmarks

From Conversable Economist:

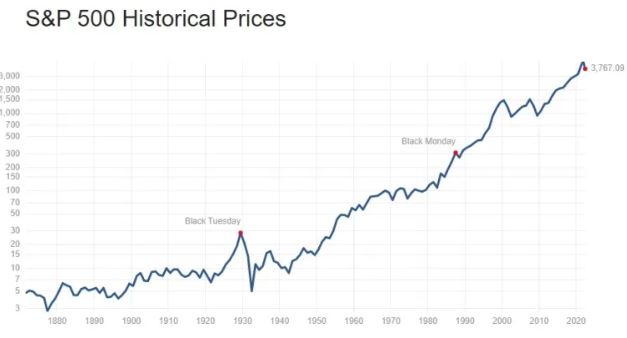

“When I get the quarterly announcements for what my retirement account is now worth, and a drop in the stock market has caused the total in the account to decline, I find myself looking at some of the long-run patterns in stock market prices.

To set the stage, here’s the historical pattern of the S&P stock index since back in the 19th century. In interpreting the figure, notice that the vertical axis is a logarithmic axis showing proportional changes; for example, the tripling from 10 to 30 is the same size as the tripling from 100 to 300 and the same as the tripling from 1000 to 3000. (Without using a log scale, all the smaller values–like the stock market crash of 1929, would just be a little squiggle what would look like a nearly flat line on the far left of the figure.) You can see some of the well-known changes in the stock market over time: the run-up of the 1920s, the crash of 1929, the run-up of the 1960s, the comparatively flat market of the 1970s, a big jump in the dot-com market of the 1990s, the run-up since 2009, and the recent decline. Of course, whenever you consider the possibility that the

For a slightly different view, here is the same set of data, this time adjusted for inflation. Again, the vertical axis shows proportional change. Again, the main well-known changes are pretty visible, but they don’t all look the same. For example, after adjusting for inflation, the Black Tuesday stock market decline in the 1920s looks even more striking, and during the high-inflation 1970s, the real value of the S&P 500 index is falling.

Of course, stock market values should be affected by expectations of corporate earnings. Thus, the standard price-earnings measure of the stock market looks at stock prices divided by corporate earnings over the previous 12 months. Notice that the logarithmic scales have now gone away. Corporate earnings will rise over the long run both because of inflation and along with overall growth in the economy. Thus, one might expect to see the P/E ratio be roughly the same over time, of course with some fluctuations as economic events and market trends interact. Indeed, when you try to find the 1929 stock market crash in this data, it’s barely apparent: after all, if both stock prices and corporate earnings collapse at about the same time, then the ratio of the two may not move in an especially dramatic way.”

From Conversable Economist:

“When I get the quarterly announcements for what my retirement account is now worth, and a drop in the stock market has caused the total in the account to decline, I find myself looking at some of the long-run patterns in stock market prices.

To set the stage, here’s the historical pattern of the S&P stock index since back in the 19th century.

Posted by at 8:10 AM

Labels: Macro Demystified

Subscribe to: Posts