Showing posts with label Macro Demystified. Show all posts

Thursday, January 17, 2019

Public Debt Through the Ages

From a new IMF working paper by Barry J. Eichengreen, Asmaa A ElGanainy, Rui Pedro Esteves, Kris James Mitchener:

“We consider public debt from a long-term historical perspective, showing how the purposes for which governments borrow have evolved over time. Periods when debt-to-GDP ratios rose explosively as a result of wars, depressions and financial crises also have a long history. Many of these episodes resulted in debt-management problems resolved through debasements and restructurings. Less widely appreciated are successful debt consolidation episodes, instances in which governments inheriting heavy debts ran primary surpluses for long periods in order to reduce those burdens to sustainable levels. We analyze the economic and political circumstances that made these successful debt consolidation episodes possible.”

From a new IMF working paper by Barry J. Eichengreen, Asmaa A ElGanainy, Rui Pedro Esteves, Kris James Mitchener:

“We consider public debt from a long-term historical perspective, showing how the purposes for which governments borrow have evolved over time. Periods when debt-to-GDP ratios rose explosively as a result of wars, depressions and financial crises also have a long history. Many of these episodes resulted in debt-management problems resolved through debasements and restructurings.

Posted by at 10:50 AM

Labels: Macro Demystified

Tuesday, January 15, 2019

Chart of the day…. or century?

Posted by at 10:36 AM

Labels: Macro Demystified

Friday, December 28, 2018

Top Ten Posts of 2018

As 2018 draws to a close, below is our list of the top ten blogs of the year.

- RIP Herman Stekler, A Forecasting Giant

- RIP Deena Khatkhate, far-sighted IMF and RBI economist

- How Well Do Economists Forecast Recessions? A Groundhog Day Update

- Economic Growth from Octavian to Obama

- Affordable Housing: Views from Albert Saiz

- The Distribution of Gains from Globalization

- Housing View – January 5, 2018 [2018 AEA Annual Meeting Special Edition]

- Household Credit, Global Financial Cycle, and Macroprudential Policies: Credit Register Evidence from an Emerging Country

- Understanding Singapore’s Housing Market

- Growth and well-being: policy should not be based on GDP alone

Photo by Colton Duke

As 2018 draws to a close, below is our list of the top ten blogs of the year.

- RIP Herman Stekler, A Forecasting Giant

- RIP Deena Khatkhate, far-sighted IMF and RBI economist

- How Well Do Economists Forecast Recessions? A Groundhog Day Update

- Economic Growth from Octavian to Obama

- Affordable Housing: Views from Albert Saiz

- The Distribution of Gains from Globalization

- Housing View – January 5,

Posted by at 9:39 AM

Labels: Macro Demystified

Thursday, December 27, 2018

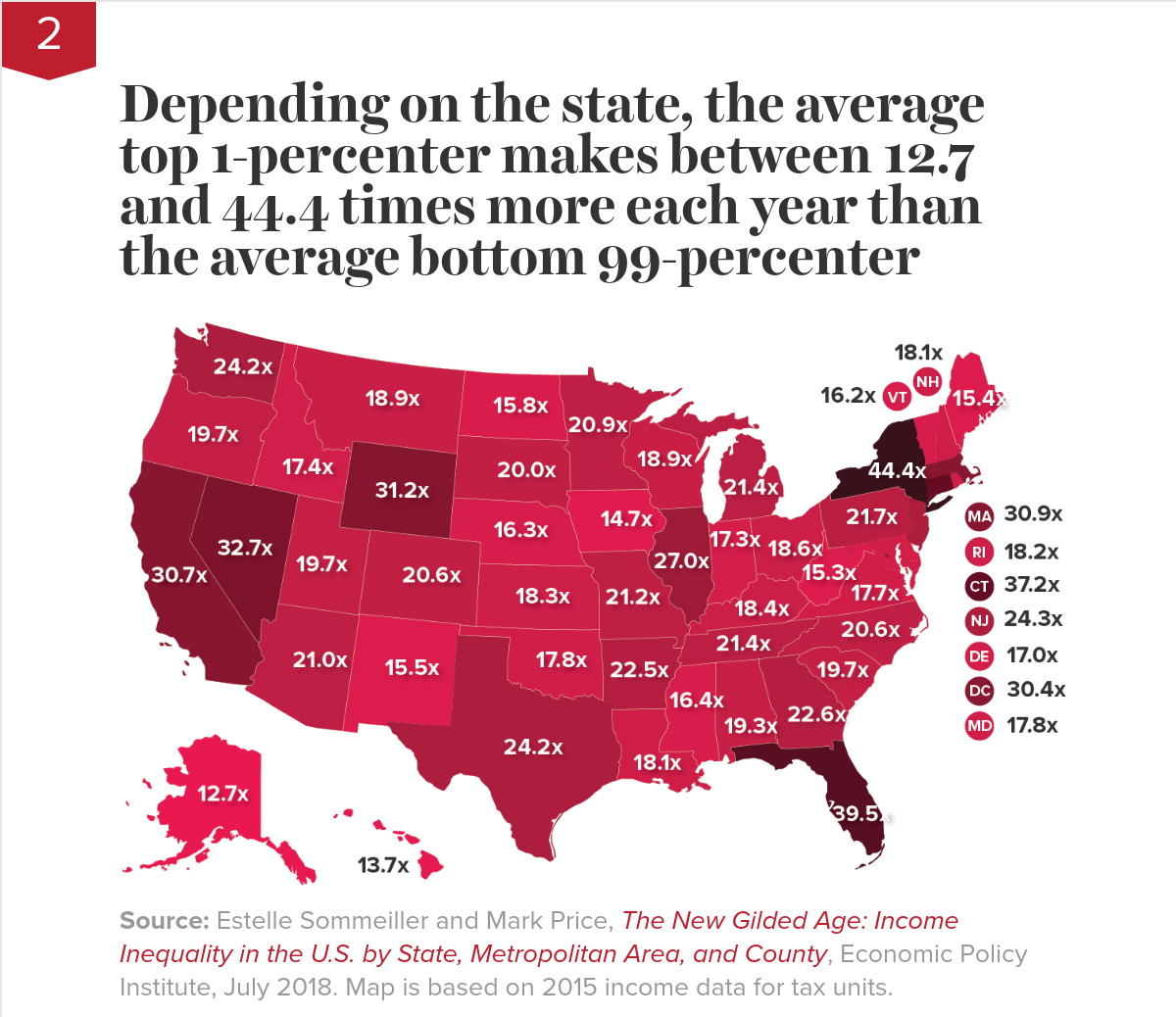

Top charts of 2018

From Economic Policy Institute:

“Twelve charts that show how policy could reduce inequality—but is making it worse instead

With the unemployment rate at 4 percent or below for eight consecutive months, 2018 appears to be the year when the economy finally became healthy again. But while low unemployment is good news, it doesn’t tell the whole story of how typical families are faring in the current economy.

As the economy normalizes following a long, slow recovery from the Great Recession, we are quickly resuming our prerecession course of rising inequality. The fruits of economic growth are bypassing typical families and going straight into the hands of the already-rich.

Our current policy trajectory is doing nothing to reverse the trend of inequality. But it’s doing plenty to widen it. This year’s edition of Top Charts highlights how policy choices continue to exacerbate inequality and how we can achieve more broadly shared prosperity through better policy choices.

Continue reading here.

From Economic Policy Institute:

“Twelve charts that show how policy could reduce inequality—but is making it worse instead

With the unemployment rate at 4 percent or below for eight consecutive months, 2018 appears to be the year when the economy finally became healthy again. But while low unemployment is good news, it doesn’t tell the whole story of how typical families are faring in the current economy.

As the economy normalizes following a long,

Posted by at 12:07 PM

Labels: Macro Demystified

Wednesday, December 12, 2018

China’s High Savings: Drivers, Prospects, and Policies

From a new IMF working paper by Longmei Zhang, Ray Brooks, Ding Ding, Haiyan Ding, Jing Lu, and Rui Mano:

“China’s high national savings rate—one of the highest in the world—is at the heart of its external/internal imbalances. High savings finance elevated investment when held domestically, or lead to large external imbalances when they flow abroad. Today, high savings mostly emanate from the household sector, resulting from demographic changes induced by the one-child policy and the transformation of the social safety net and job security that occured during the transition from planned to market economy. Housing reform and rising income inequality also contribute to higher savings. Moving forward, demographic changes will put downward pressure on savings. Policy efforts in strengthening the social safety net and reducing income inequality are also needed to reduce savings further and boost consumption.”

From a new IMF working paper by Longmei Zhang, Ray Brooks, Ding Ding, Haiyan Ding, Jing Lu, and Rui Mano:

“China’s high national savings rate—one of the highest in the world—is at the heart of its external/internal imbalances. High savings finance elevated investment when held domestically, or lead to large external imbalances when they flow abroad. Today, high savings mostly emanate from the household sector, resulting from demographic changes induced by the one-child policy and the transformation of the social safety net and job security that occured during the transition from planned to market economy.

Posted by at 7:15 AM

Labels: Macro Demystified

Subscribe to: Posts