Showing posts with label Macro Demystified. Show all posts

Tuesday, May 7, 2019

Globalization, Market Power, and the Natural Interest Rate

From a new IMF working paper by Jean-Marc Natal and Nicolas Stoffels:

“We argue that strong globalization forces have been an important determinant of global real interest rates over the last five decades, as they have been key drivers of changes in the natural real interest rate—i.e. the interest rate consistent with output at its potential and constant inflation. An important implication of our analysis is that increased competition in goods and labor market since the 1970s can help explain both the large increase in real interest rates up to the mid-1980s and—as globalization forces mature and may even go into reverse, leading to incrementally rising market power—its subsequent and protracted decline accompanied by lower inflation. The analysis has important implications for monetary policy and the optimal pace of normalization.”

From a new IMF working paper by Jean-Marc Natal and Nicolas Stoffels:

“We argue that strong globalization forces have been an important determinant of global real interest rates over the last five decades, as they have been key drivers of changes in the natural real interest rate—i.e. the interest rate consistent with output at its potential and constant inflation. An important implication of our analysis is that increased competition in goods and labor market since the 1970s can help explain both the large increase in real interest rates up to the mid-1980s and—as globalization forces mature and may even go into reverse,

Posted by at 11:11 AM

Labels: Macro Demystified

Wednesday, April 10, 2019

Rethinking the Phillips Curve: Inflation May Rise Modestly Next Year

From an article by Christopher G. Collins (PIIE) and Joseph E. Gagnon (PIIE):

“The US economy is running hot, with a record high rate of job vacancies and the lowest unemployment rate in nearly fifty years. Yet most forecasters predict no increase at all in inflation. This combination appears to challenge the validity of the Phillips curve, a popular economic model dating from the 1950s that predicts rising inflation when unemployment is low and falling inflation when unemployment is high. In a new paper, however, we show that the relationship between inflation and unemployment has shifted twice—in the late 1960s and in the mid-1990s. The paper replicates the findings of some other researchers, who find a very flat Phillips curve since the 1990s, implying that unemployment has little effect on inflation. But we also propose an alternative hypothesis: The Phillips curve is bent when inflation is low so that high unemployment has little downward effect on inflation, but low unemployment still pushes inflation up. If we are right, inflation is likely to rise modestly over the next couple of years. We will explore what this means for monetary policy in a subsequent post.

THE EVOLVING US PHILLIPS CURVE

Alban Phillips (1958) developed the original curve bearing his name. It related the rate of wage inflation to the unemployment rate in the United Kingdom over the period 1861–1913. Olivier Blanchard (2017, chapter 8) showed that a similar downward-sloping curve in terms of price inflation and unemployment was apparent in the United States in 1900–1960. Our paper confirms Blanchard’s finding that the rising inflation of the late 1960s led to the unmooring of expectations of inflation from the stable low levels that had prevailed before then and a shift in the Phillips curve to a relationship between the change in the rate of inflation and the unemployment rate. The return of inflation to a very low and stable level led to a second shift in the Phillips curve in the mid-1990s, back to a relationship between the level of inflation and the unemployment rate.

In addition to this shift in the persistence of inflation, many researchers have found that the Phillips curve has been very flat since the 1990s, so that changes in unemployment have little effect on inflation. This was most dramatically demonstrated in the aftermath of the Great Recession of 2008–09, when unemployment remained very high for years and yet inflation barely dipped. We show, however, that another hypothesis fits the data equally well: The Phillips curve may become bent when inflation is low, with a flat portion for high unemployment and a steeper portion for low unemployment.”

Continue reading here.

From an article by Christopher G. Collins (PIIE) and Joseph E. Gagnon (PIIE):

“The US economy is running hot, with a record high rate of job vacancies and the lowest unemployment rate in nearly fifty years. Yet most forecasters predict no increase at all in inflation. This combination appears to challenge the validity of the Phillips curve, a popular economic model dating from the 1950s that predicts rising inflation when unemployment is low and falling inflation when unemployment is high.

Posted by at 8:55 AM

Labels: Macro Demystified

Wednesday, February 27, 2019

Macro reasons to loath protectionism

From a VoxEU post by Davide Furceri, Swarnali Ahmed Hannan, Jonathan D. Ostry, Andrew Rose:

“It seems an appropriate time to study what, if any, have been the macroeconomic consequences of tariffs in practice. Using a straightforward methodology to estimate flexible impulse response functions, and data that span several decades and 151 countries, this column finds that tariff increases have, on average, engendered adverse macroeconomic and distributional consequences: a fall in output and labour productivity, higher unemployment, higher inequality, and negligible effects on the trade balance (likely owing to real exchange rate appreciation when tariffs rise). The aversion of the economics profession to the deadweight loss caused by protectionism seems warranted.

One of the most pressing issues on the international agenda these days is protectionism. The US’ trade war with China has created international tension that is infecting stock markets worldwide, exacerbated by other disputes such as the renegotiation of NAFTA, Brexit, and US steel and aluminium tariffs. One ingredient curiously absent from this turbulence is disagreement among the experts on the merits (or lack thereof) on the underlying issue. Indeed, more than on any other issue, there is agreement amongst economists that international trade should be free.1

Economists have been aware of the senselessness of protectionism since at least Adam Smith. In general, economists believe that freely functioning markets best allocate resources, at least absent some distortion, externality or other market failure; competitive markets tend to maximise output by directing resources to their most productive uses. Of course, there are market imperfections, but tariffs – taxes on imports – are almost never the optimal solution to such problems. Tariffs encourage the deflection of trade to inefficient producers and smuggling to evade the tariffs; such distortions reduce productivity, income and welfare. Further, consumers lose more from a tariff than producers gain, so there is ‘deadweight loss’ as well as inequality (if production tends to be owned by the rich). The redistributions associated with tariffs tend to create vested interests, so harms tend to persist. Broad-based protectionism can also provoke retaliation which adds further costs. All these losses to output are exacerbated if inputs are protected, since this adds to production costs.

Discussions of market imperfections and the like are naturally microeconomic in nature (Grossman and Rogoff 1995). Accordingly, most analysis of trade barriers focuses on individual industries. International commercial policy tends not to be used as a macroeconomic tool, probably because of the availability of superior alternatives such as monetary and fiscal policy. In addition, there are strong theoretical reasons that economists abhor the use of protectionism as a macroeconomic policy; for instance, the broad imposition of tariffs may lead to offsetting changes in exchange rates (Dornbusch, 1974). And while the imposition of a tariff could reduce the flow of imports, it is unlikely to change the trade balance unless it fundamentally alters the balance of saving and investment. The findings of recent studies on the impact of trade would imply that tariffs could hurt output and productivity (Feyrer 2009, Alcala and Ciccone 2004). Further, economists think that protectionist policies helped precipitate the collapse of international trade in the early 1930s, and this trade shrinkage was a plausible seed of WWII. So, while protectionism has not been much used in practice as a macroeconomic policy (especially in advanced countries), most economists also agree that it should not be used as a macroeconomic policy.

The here and now

Times change. Some economies – notably the US – have recently begun to use commercial policy seemingly for macroeconomic objectives. So it seems an appropriate time to study what, if any, the macroeconomic consequences of tariffs have actually been in practice. Most of the predisposition of the economics profession against protectionism is based on evidence that is either a) theoretical, b) micro, or c) aggregate and dated. Accordingly, in our recent research (Furceri et al. 2018), we study empirically the macroeconomic effects of tariffs using recent aggregate data.”

Continue reading here.

From a VoxEU post by Davide Furceri, Swarnali Ahmed Hannan, Jonathan D. Ostry, Andrew Rose:

“It seems an appropriate time to study what, if any, have been the macroeconomic consequences of tariffs in practice. Using a straightforward methodology to estimate flexible impulse response functions, and data that span several decades and 151 countries, this column finds that tariff increases have, on average, engendered adverse macroeconomic and distributional consequences: a fall in output and labour productivity,

Posted by at 10:18 AM

Labels: Macro Demystified

Sunday, February 3, 2019

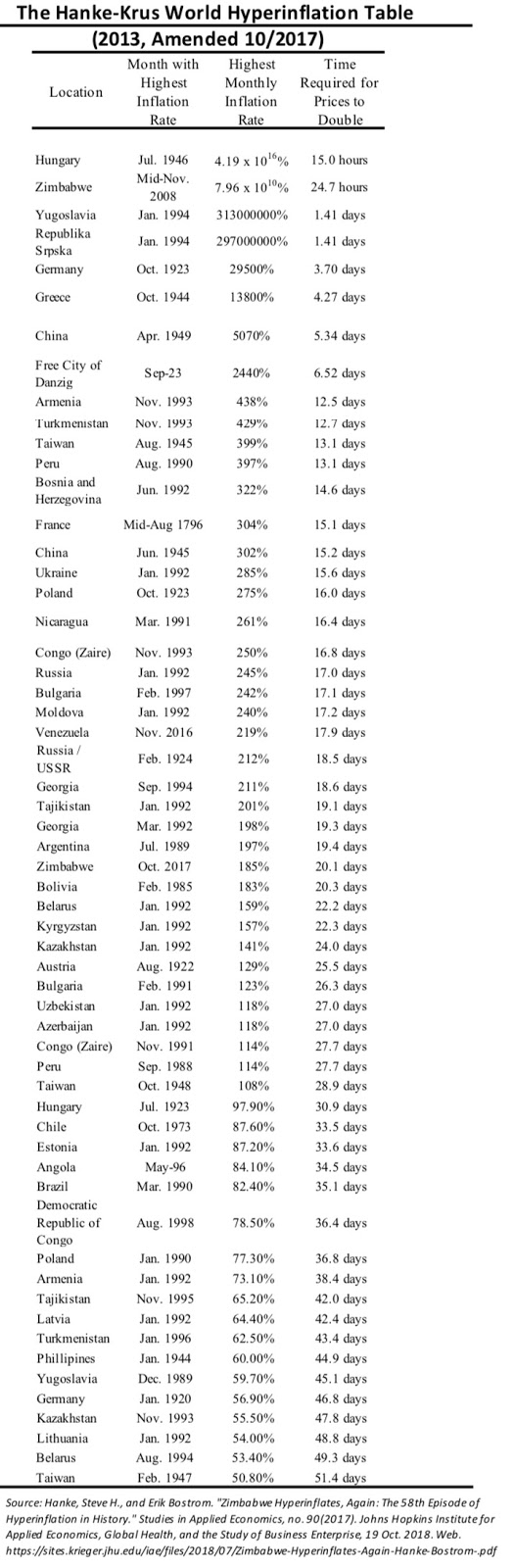

58 Episodes of Hyperinflation (Venezuela is #23)

From Conversable Economist:

“Steve Hanke has devoted considerable effort to building up data on hyperinflations during the last century or so. He offers a quick overview of this work in Forbes (January 20, 2019). Below is his list of hyperinflations. When it comes to Venezuela, he writes:

Now, let’s turn to the world’s only current hyperinflation: Venezuela. It ranks as the 23rd most severe. Today, the annual rate of inflation is 120,810%/yr. While this rate is modest by hyperinflation standards, the duration of Venezuela’s hyperinflation episode, as of today, is long: 27 months. Only four episodes of hyperinflation have been more long-lived.

Here’s the table of all 58 hyperinflations:”

From Conversable Economist:

“Steve Hanke has devoted considerable effort to building up data on hyperinflations during the last century or so. He offers a quick overview of this work in Forbes (January 20, 2019). Below is his list of hyperinflations. When it comes to Venezuela, he writes:

Now, let’s turn to the world’s only current hyperinflation: Venezuela. It ranks as the 23rd most severe.

Posted by at 8:16 AM

Labels: Macro Demystified

Tuesday, January 29, 2019

Budget Deficits and Debt: Background and Tradeoffs

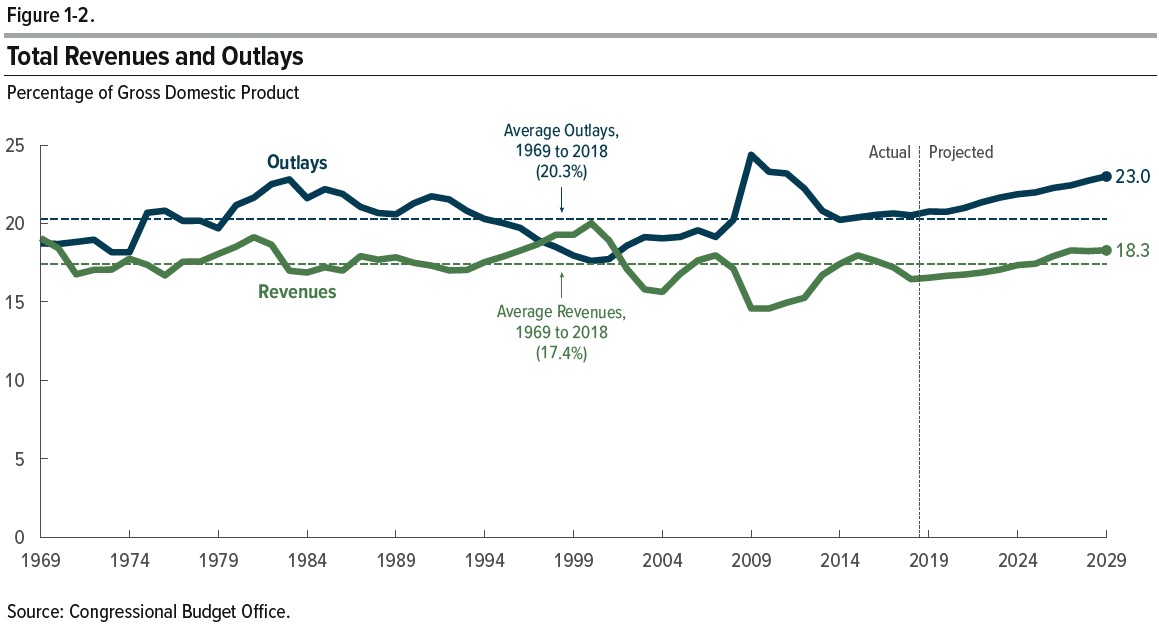

From Conversable Economist:

“Twice a year the Congressional Budget Office publishes a “just the facts” overview of the federal budget picture and the US economy. The latest version is “The Budget andEconomic Outlook:2019 to 2029 (January 2019). Here, I’ll focus on the US budget deficit and debt.

Here’s the pattern of US federal government spending and revenues in the last 50 years. Average outlays during that time were 20.7% of GDP. Average revenues were 17.4% of GDP. Contrary to the widespread belief that US government spending and taxes have over time surged ever higher, to me the more obvious pattern here over the half-century is one of stability. Sure, government spending is higher and taxes are lower than the historical averages during the Great Recession. But during boom times like the late 1990s, taxes are above their historical average while spending is below. When President Trump took office early in 2017, US government spending and taxes were–whether for better or worse–almost bang on their long-run averages.

But under the surface, two changes are going on–one medium-term and one longer-term. The medium-term change is that the usual pattern over time has been that when the US economy is proceeding strongly, with sustained growth and a relatively low unemployment rate, the budget deficits are usually lower, or in the late 1990s even turned into surpluses. But at present, the trajectory is a relatively healthy economy but with larger-than-usual budget deficits.

This CBO figures shows that if one looks back at years when the unemployment rate was below 6%, the average budget deficit has been 1.5% of GDP. But although the current unemployment rate has been substantially below 6% for several years, the projected budget deficits for the next decade are projected at 4.4% of GDP.

Continue reading here.

From Conversable Economist:

“Twice a year the Congressional Budget Office publishes a “just the facts” overview of the federal budget picture and the US economy. The latest version is “The Budget andEconomic Outlook:2019 to 2029 (January 2019). Here, I’ll focus on the US budget deficit and debt.

Here’s the pattern of US federal government spending and revenues in the last 50 years. Average outlays during that time were 20.7% of GDP.

Posted by at 9:34 AM

Labels: Macro Demystified

Subscribe to: Posts