Showing posts with label Macro Demystified. Show all posts

Thursday, October 24, 2019

The Phillips curve: Dead or alive

From VOX post by Peter Hooper, Frederic S. Mishkin, Amir Sufi:

“The apparent flattening of the Phillips curve has led some to claim that it is dead. The column uses data from US states and metropolitan areas to suggest a steeper slope, with non-linearities in tight labour markets. We have been here before – in the 1960s, similar low and stable inflation expectations led to the great inflation of the 1970s.

At a ‘Fed Listens’ event on 26 September 2019, Richard Clarida, vice chair of the Federal Reserve Board, observed that the flattening of the Phillips curve in recent decades is central to the Fed’s review of policy strategy (Clarida 2019). Price inflation has become much less responsive to resource slack, permitting the Fed to support employment during economic downturns more aggressively than it has in the past.

A flat Phillips curve reduces the chances of a breakout of inflation. This is especially important because the Fed considers the benefits of running a high-pressure economy, and of adopting a policy strategy that makes up for inflation misses to the downside by aiming for subsequent overshoots. Many participants in financial markets go even further than the Fed, believing that the Phillips curve is dead – in other words, excessive inflation is no longer a risk.

Recent experience in the US, Europe, and Japan appears to support this view. Major central banks struggle to get inflation to return to (or even move towards their objectives), even after labour markets have tightened. The US labour market has been running at or beyond estimates of full employment for the past two years, and inflation is still significantly below the Fed’s 2% target.

Indeed, measures of inflation expectations have been drifting lower, not higher as the Phillips curve model would predict. So is this model really dead, or just dormant? If not dead, how can we explain the flattening of the Phillips curve? What might reverse this trend, leading to a resurgence of inflation?

A lot of empirical research has been devoted to these questions over the past decade, for example Yellen (2015), Kiley (2015) Blanchard (2016), Nalewaik (2016), Powell (2018), and Hooper et al. (2019). We know that the Phillips curve was alive and well during the 1950s through the 1970s, and into the 1980s at the national level. Prices and wages showed significant sensitivity to movements in unemployment during this period. These sensitivities increased when the labour market tightened beyond full employment, indicating a nonlinear relationship. Policymakers allowed the labour market to tighten well beyond full employment levels for a sustained period during the 1960s and, at first, inflation remained low and stable. But several years of tight labour markets resulted in the great inflation of the 1970s.

Since the late 1980s, however, there has been only weak evidence of the sensitivity and nonlinearity of the response of inflation to labour market tightening. Efforts to estimate statistically significant price Phillips curve models using national data have generally failed.

Is the Phillips curve dead?

In a recent paper (Hooper et al. 2019), we argue that there are three reasons why the evidence for a dead Phillips curve is weak.”

Continue reading here.

From VOX post by Peter Hooper, Frederic S. Mishkin, Amir Sufi:

“The apparent flattening of the Phillips curve has led some to claim that it is dead. The column uses data from US states and metropolitan areas to suggest a steeper slope, with non-linearities in tight labour markets. We have been here before – in the 1960s, similar low and stable inflation expectations led to the great inflation of the 1970s.

Posted by at 10:00 AM

Labels: Macro Demystified

Saturday, September 28, 2019

The Phillips Curve: a Relation between Real Exchange Rate Growth and Unemployment

From a working paper by François Geerolf:

“The negative relationship between inflation and unemployment (also known as the Phillips curve) has been repeatedly challenged in the last decades: missing inflation in 2013-2019, missing deflation in 2007-2010, missing inflation in the late 1990s, stagflation in the 1970s, contrasting with always strong regional Phillips curves. Using data from multiple sources, this paper helps to solve many empirical puzzles by distinguishing between fixed and flexible exchange rate regimes: in fixed exchange rate regimes, inflation is negatively correlated with unemployment but this relationship does not hold in flexible regimes. By contrast, there is a negative correlation between real exchange rate appreciation and unemployment, which remains consistent in both fixed and flexible regimes. These crucial observations have important implications for identifying the source of business cycle fluctuations, for normative analysis, and imply a significant departure from rational-expectation-based solutions to Phillips curve puzzles.”

From a working paper by François Geerolf:

“The negative relationship between inflation and unemployment (also known as the Phillips curve) has been repeatedly challenged in the last decades: missing inflation in 2013-2019, missing deflation in 2007-2010, missing inflation in the late 1990s, stagflation in the 1970s, contrasting with always strong regional Phillips curves. Using data from multiple sources, this paper helps to solve many empirical puzzles by distinguishing between fixed and flexible exchange rate regimes: in fixed exchange rate regimes,

Posted by at 1:55 PM

Labels: Macro Demystified

Thursday, July 18, 2019

Why Is Inflation Low Globally?

From the Federal Reserve Bank of San Francisco:

“A hot economy eventually boosts inflation. Such is the simple wisdom of the Phillips curve. Yet inflation across developed countries has been remarkably weak since the 2008 global financial crisis, even though unemployment rates are near historical lows. What is behind this recent disconnect between inflation and unemployment? Contrasting the experiences of developed and developing economies before and after the financial crisis shows that broader factors than monetary policy are at play. Inflation has declined globally, and this trend preceded the financial crisis.

The world economies have mostly recovered from the 2008 financial crisis. In the United States, United Kingdom, and Germany, for example, the unemployment rate is now below 4%, lower than it has been in decades. Tight labor markets are usually a symptom of a healthy economy and thus a rising demand for goods and services. To satisfy such demand, businesses usually raise prices—the basic mechanism underlying the standard economic relationship known as the Phillips curve. Yet, 10 years after the financial crisis, inflation has held remarkably steady. Some researchers therefore argue that the Phillips curve is no longer a useful descriptor of inflation dynamics (Coibion and Gorodnichenko 2015).

In this Economic Letter, we investigate whether the financial crisis has changed the long-standing inner workings of the Phillips curve. We extend the analysis in our previous Economic Letter (Jordà et al. 2019) to include developing economies and analyze three components of the Phillips curve to assess where the links appear to be broken.

Our analysis suggests that news of the death of the Phillips curve in developed economies appears premature. Fluctuations in labor market conditions have been largely offset with appropriate interest rate changes by central banks. Under such conditions, the influence of past inflation has faded, and expectations for future inflation have gravitated toward the central bank’s stated target. On the surface, inflation appears stable at all levels of labor market slack, and the Phillips curve link appears broken. Underneath, however, the Phillips curve could still be at work. The inflation dynamics that we observe could also be explained by a central bank that successfully offsets fluctuations in slack to keep inflation at the target. In less developed economies, central banks often operate under constraints that prevent full monetary policy offsets, which has given a bigger role to feedback from past inflation. That said, inflation has been trending down for the past two decades across developed and developing economies alike. The inevitable conclusion is that there are global forces putting downward pressure on inflation, and it is not just the result of better monetary policy.”

Figure 1

Phillips curve across OECD countries by decade

Continue reading here.

From the Federal Reserve Bank of San Francisco:

“A hot economy eventually boosts inflation. Such is the simple wisdom of the Phillips curve. Yet inflation across developed countries has been remarkably weak since the 2008 global financial crisis, even though unemployment rates are near historical lows. What is behind this recent disconnect between inflation and unemployment? Contrasting the experiences of developed and developing economies before and after the financial crisis shows that broader factors than monetary policy are at play.

Posted by at 10:37 AM

Labels: Macro Demystified

Friday, July 12, 2019

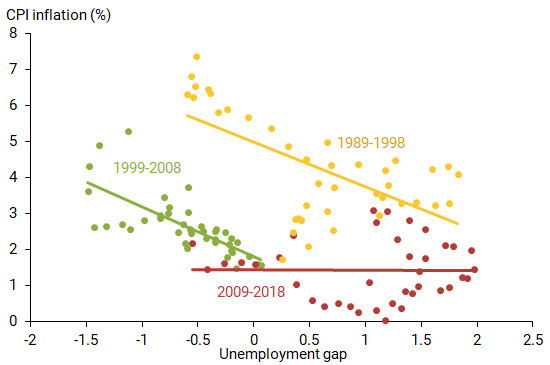

Is There a Relationship between Inflation and Unemployment?

From Econbrowser:

“Or, old fogey downloads data, finds a negative relationship, a.k.a. the Phillips Curve…

Much was made of the meeting of minds of AOC and Larry Kudlow regarding the Phillips Curve, to wit (from Bloomberg):

… Ocasio-Cortez said many economists are concerned that the formula “is no longer describing what is happening in today’s economy” — and Powell largely agreed.

“She got it right,” Kudlow told reporters at the White House later on Thursday. “He confirmed that the Phillips Curve is dead. The Fed is going to lower interest rates.”

Well, since I’ve been teaching the Phillips Curve for lo these thirty odd years, I thought I’d check to see if I’d missed something. First, it’s important to remember that while we talk about the negative relationship between inflation and unemployment, or the positive relationship between inflation and output, the actual model we use is the expectations augmented Phillips curve including input price shocks. My preferred specification is:

πt = πet + f(ut-4 – un,t-4) + θzt

Where π is 4 quarter inflation, πe is expected inflation, u is official unemployment rate, un is natural rate of unemployment [ so (u-un) is the unemployment gap], and z is an input price shock, in this case the 4 quarter inflation rate in import prices. Each of these series is available from FRED; using the FRED acronyms, PCEPI for the personal consumption expenditure deflator, MICH for University of Michigan’s 1 year inflation expectations, UNRATE for unemployment rate, NROU for natural rate of unemployment, and IR for import prices.

Estimate this relationship using OLS over the 1987-2019Q2 period (first two months of 2019Q2 used to proxy for Q2). This sample period, after accounting for lags, spans the “Great Moderation”.”

From Econbrowser:

“Or, old fogey downloads data, finds a negative relationship, a.k.a. the Phillips Curve…

Much was made of the meeting of minds of AOC and Larry Kudlow regarding the Phillips Curve, to wit (from Bloomberg):

… Ocasio-Cortez said many economists are concerned that the formula “is no longer describing what is happening in today’s economy” — and Powell largely agreed.

“She got it right,” Kudlow told reporters at the White House later on Thursday.

Posted by at 10:03 AM

Labels: Macro Demystified

Thursday, May 9, 2019

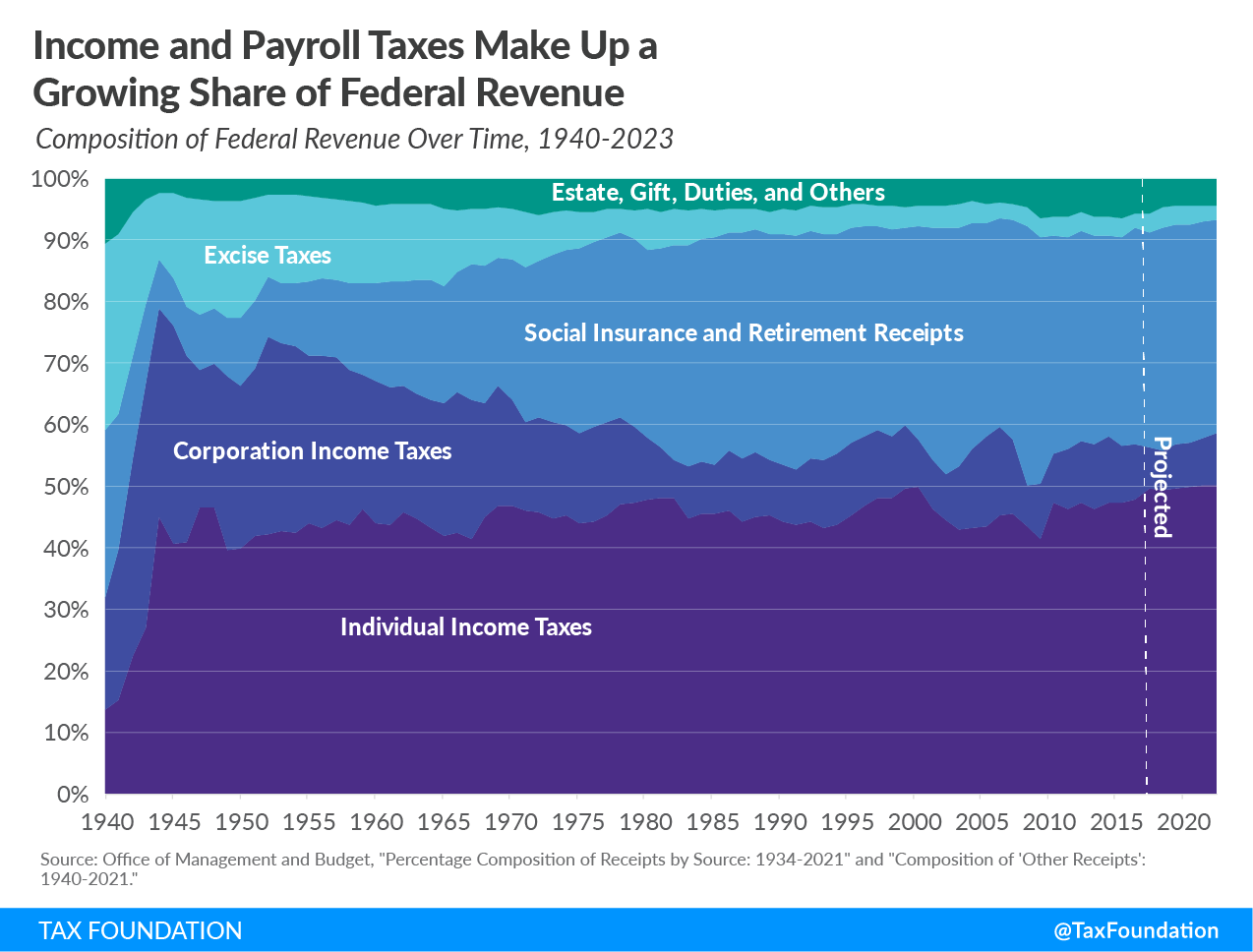

Snapshots of US Income Taxation Over Time

From Conversable Economist:

“As Americans recover from our annual April 15 deadline for filing income taxes, here are a series of figures about longer-term patterns of taxes in the US economy. They are drawn from a series of blog posts by the Tax Foundation over the last few months. The Tax Foundation is a nonpartisan group whose analysis typically leans toward side that taxes on those with high incomes are already high enough. However, the figures that follow are compiled from fairly standard data sources: IRS data, the Congressional Budget Office, and the like.

For example, here’s a figure showing what taxes are the main sources of federal income over time from Erica York. She writes: “Before 1941, excise taxes, such as gas and tobacco taxes, were the largest source of revenue for the federal government, comprising nearly one-third of government revenue in 1940. Excise taxes were followed by payroll taxes and then corporate income taxes. Today, payroll taxes remain the second largest source of revenue. However, other sources have shifted in relative importance. Specifically, individual income taxes have become a central pillar of the federal revenue system, now comprising nearly half of all revenue. Following an opposite trend, corporate income and excise taxes have decreased relative to other sources.”

From Conversable Economist:

“As Americans recover from our annual April 15 deadline for filing income taxes, here are a series of figures about longer-term patterns of taxes in the US economy. They are drawn from a series of blog posts by the Tax Foundation over the last few months. The Tax Foundation is a nonpartisan group whose analysis typically leans toward side that taxes on those with high incomes are already high enough.

Posted by at 9:14 AM

Labels: Macro Demystified

Subscribe to: Posts