Showing posts with label Inclusive Growth. Show all posts

Sunday, May 8, 2022

Exploring the crypto-sustainability trade-off

Source: Project Syndicate

“The explosive growth of Bitcoin and other cryptocurrencies has opened up a new front in the broader climate crisis by threatening to offset the progress made in recent years toward decarbonization. For the technology to gain wider adoption over the long term, its proponents will have to get serious about reducing its energy usage“, writes Marion Laboure of Harvard University.

The extensive power requirements in the cryptocurrency mining process, especially of those currencies limited in supply like Bitcoin, have generated a global debate on the sustainability of the process. While China banned the mining of cryptocurrency in September 2021 amidst an already debilitating energy crisis, other countries like El Salvador have adopted other methods like establishing a crypto mining city near a volcano to power the process using geothermal energy. Clearly, the world is divided on the matter. This article explores the issue in greater detail, charts out the environment-revenue trade-off before economies, and explores potential solutions.

Read on to know more.

Source: Project Syndicate

“The explosive growth of Bitcoin and other cryptocurrencies has opened up a new front in the broader climate crisis by threatening to offset the progress made in recent years toward decarbonization. For the technology to gain wider adoption over the long term, its proponents will have to get serious about reducing its energy usage“, writes Marion Laboure of Harvard University.

The extensive power requirements in the cryptocurrency mining process,

Posted by at 2:07 PM

Labels: Energy & Climate Change, Inclusive Growth

Saturday, May 7, 2022

The US labor market could be cooling down now

Source: Peterson Institute of International Economics

While a lot of research conducted from 2021 until March of 2022 suggests that labor markets in the US reached record high levels of tightness as job openings and quits rose, recent evidence collected by the Peterson Institute indicates the possibility of a potential cool down. The underlying argument driving this idea is that the sharp spike in nominal wages in 2021 could have been a result of some post-pandemic factors that shaped expectations of longer-run inflation which ultimately got dragged until 2022. So even though labor force participation rates in the US in April 2022 remained at 3.6%, 0.1% higher than the corresponding pre-pandemic level, the authors argue that this shortfall in employment is driven by a labor supply shortage as demand is robust.

The article also touches upon related issues like rising nominal wages that are beginning to plateau now and a somewhat alarming drop in real wages.

Read the full article to know more.

Source: Peterson Institute of International Economics

While a lot of research conducted from 2021 until March of 2022 suggests that labor markets in the US reached record high levels of tightness as job openings and quits rose, recent evidence collected by the Peterson Institute indicates the possibility of a potential cool down. The underlying argument driving this idea is that the sharp spike in nominal wages in 2021 could have been a result of some post-pandemic factors that shaped expectations of longer-run inflation which ultimately got dragged until 2022.

Posted by at 10:49 AM

Labels: Inclusive Growth

Wednesday, March 23, 2022

Will COVID-19 Have Long-Lasting Effects on Inequality? Evidence from Past Pandemics

From a new paper by Davide Furceri, Prakash Loungani, Jonathan D. Ostry, and Pietro Pizzuto:

“This paper provides evidence on the impact of major epidemics from the past two decades on income distribution. The pandemics in our sample, even though much smaller in scale than COVID-19, have led to increases in the Gini coefficient, raised the income share of higher income deciles, and lowered the employment-to-population ratio for those with basic education compared to those with higher education. We provide some evidence that the distributional consequences from the current pandemic may be larger than those flowing from the historical pandemics in our sample, and larger than those following typical recessions and financial crises.”

From a new paper by Davide Furceri, Prakash Loungani, Jonathan D. Ostry, and Pietro Pizzuto:

“This paper provides evidence on the impact of major epidemics from the past two decades on income distribution. The pandemics in our sample, even though much smaller in scale than COVID-19, have led to increases in the Gini coefficient, raised the income share of higher income deciles, and lowered the employment-to-population ratio for those with basic education compared to those with higher education.

Posted by at 12:24 PM

Labels: Inclusive Growth

Sunday, March 20, 2022

An assessment of US labor market rigidity

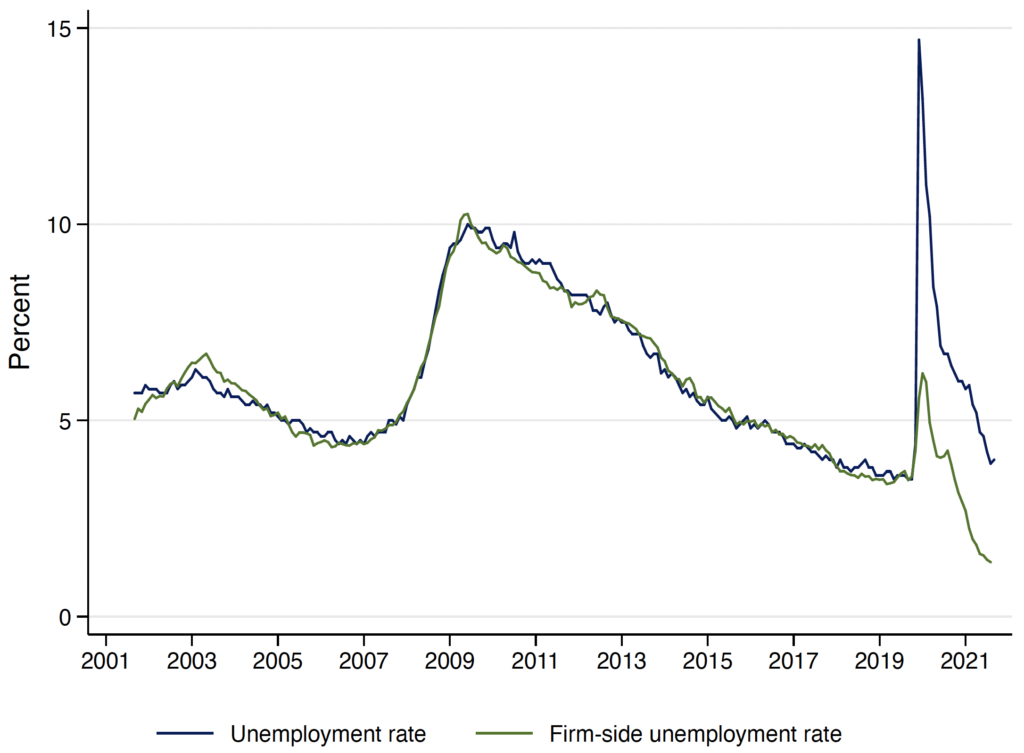

Source: VoxEU CEPR

Abstract: Since the beginning of the pandemic, labour market indicators have been sending different signals about the degree of slack in the US labour market. This column uses time-series and cross-section data to show that firm-side unemployment (figure underneath) – a measure that ties together the unemployment rate with the vacancy and quits rate – predicts wage inflation better than the unemployment rate or the employment ratio, and that firm-side unemployment currently experienced in the US corresponds to a degree of tightness previously associated with sub 2% unemployment. The findings suggest that labour markets in the US are extremely tight and will likely contribute to inflationary pressures for some time to come.

Figure: Actual unemployment rate versus firm-side estimated unemployment rate

Source: VoxEU CEPR

Abstract: Since the beginning of the pandemic, labour market indicators have been sending different signals about the degree of slack in the US labour market. This column uses time-series and cross-section data to show that firm-side unemployment (figure underneath) – a measure that ties together the unemployment rate with the vacancy and quits rate – predicts wage inflation better than the unemployment rate or the employment ratio,

Posted by at 10:58 AM

Labels: Inclusive Growth

Monday, March 14, 2022

Tackling Gender Gaps in Data

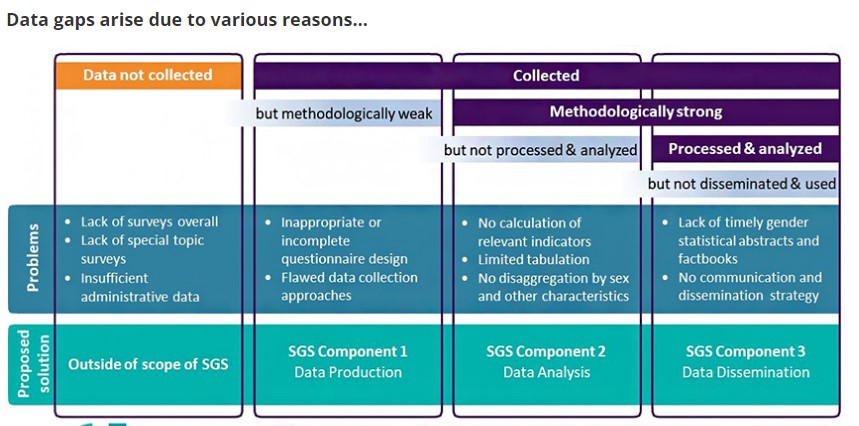

Ironically, in the big data age of today, a significant barrier to women’s inclusion in formal economies is made up of the lack of sex-disaggregated data at the high level. Within this, the lack of more granular data to base models and policies on, the lack of data on related services like internet access, use of bank accounts, feature phones and smartphones, or even inclusion in the national identification process is hard to come by.

In a recent blog detailing ideas for their new project, Strengthening Gender Statistics, officials from the World Bank Group write about challenges to accessing quality gendered data and how to tackle them. They try to understand the vast variety of challenges by grouping them into three categories- challenges to data production, analysis, and dissemination.

Read also:

Making Women and Girls Visible: Gender Data Gaps and Why They Matter (2018), UN Women

Closing gender data gaps in the world of work- role of the 19th ICLS standards (2020), ILO

Ironically, in the big data age of today, a significant barrier to women’s inclusion in formal economies is made up of the lack of sex-disaggregated data at the high level. Within this, the lack of more granular data to base models and policies on, the lack of data on related services like internet access, use of bank accounts, feature phones and smartphones, or even inclusion in the national identification process is hard to come by.

Posted by at 3:07 PM

Labels: Inclusive Growth

Subscribe to: Posts