Showing posts with label Inclusive Growth. Show all posts

Tuesday, May 15, 2018

Fiscal Consolidation and Income Inequality in Latin America and the Caribbean

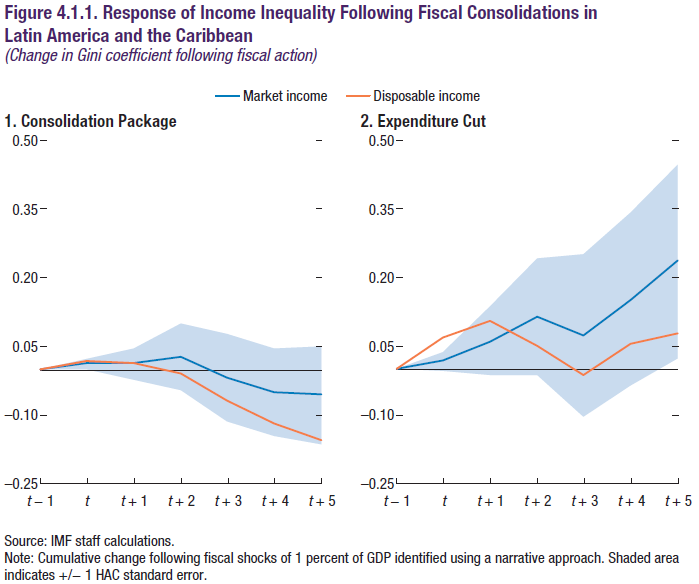

The new IMF Regional Economic Outlook finds that “Fiscal consolidations have very little effects on income inequality in LAC. Point estimates are positive but very small––the market Gini increases by 0.03 units after two years––and are not statistically significant (Figure 4.1.1, panel 1). This is despite a reduction in output of about 1 percent and an increase in unemployment of 0.3 of a percentage point, as demonstrated in the main text. Focusing on the distribution of disposable income does not affect these results, with the Gini coefficient being relatively insensitive to fiscal consolidation shocks.”

It also notes my previous works that “For advanced economies, there is evidence that fiscal consolidation tends to increase income inequality, with especially strong effects when the consolidation is spending-based (Ball and others 2013; Furceri, Jalles, and Loungani 2015; Woo and others 2017).”

Ball, Furceri, Leigh, and Loungani (2013) is available here. Furceri, Jalles, and Loungani (2015) is available here.

The new IMF Regional Economic Outlook finds that “Fiscal consolidations have very little effects on income inequality in LAC. Point estimates are positive but very small––the market Gini increases by 0.03 units after two years––and are not statistically significant (Figure 4.1.1, panel 1). This is despite a reduction in output of about 1 percent and an increase in unemployment of 0.3 of a percentage point, as demonstrated in the main text. Focusing on the distribution of disposable income does not affect these results,

Posted by at 2:48 PM

Labels: Inclusive Growth

The macroeconomic effects of fiscal consolidation in Latin America and the Caribbean

The new IMF Regional Economic Outlook finds that “fiscal multipliers in the region are estimated to lie between 0.5 and 1.1–suggesting that consolidation will be more contractionary than previously thought. Nevertheless, these estimates are small enough to suggest that consolidations will improve the region’s debt dynamics, even in the short run. Since expenditure multipliers vary according to the type of instrument used, consolidation plans should preserve public investment to support growth and employment.”

The new IMF Regional Economic Outlook finds that “fiscal multipliers in the region are estimated to lie between 0.5 and 1.1–suggesting that consolidation will be more contractionary than previously thought. Nevertheless, these estimates are small enough to suggest that consolidations will improve the region’s debt dynamics, even in the short run. Since expenditure multipliers vary according to the type of instrument used, consolidation plans should preserve public investment to support growth and employment.”

Posted by at 2:33 PM

Labels: Inclusive Growth

Strengthening natural disaster resilience a savings fund proposal

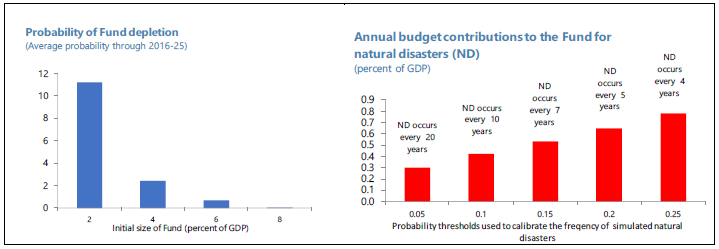

A new IMF country report says that “The Bahamas is disproportionately exposed to natural disasters – both in terms of frequency and associated costs. An appropriate disaster risk-management strategy should be wide ranging, from strengthening resilience through capital and infrastructure investments, having a multilayer disaster risk financing plan, and strengthening fiscal and external buffers. Along these lines, staff proposes the creation of a natural disaster savings fund of a target size of 2-4 percent of GDP.”

“The savings fund should be government by clear rules on inflows and outflows as well as transparency requirements. Clear objectives and disbursement rules and triggers based on verifiable criteria are critical. The fund should have prudent and transparent investment policies and should be consolidated with budgetary information to allow assessment of the overall fiscal situation. At a minimum, the fund balance should appear in financial statements, and drawdowns

should appear in budget execution reports.”

A new IMF country report says that “The Bahamas is disproportionately exposed to natural disasters – both in terms of frequency and associated costs. An appropriate disaster risk-management strategy should be wide ranging, from strengthening resilience through capital and infrastructure investments, having a multilayer disaster risk financing plan, and strengthening fiscal and external buffers. Along these lines, staff proposes the creation of a natural disaster savings fund of a target size of 2-4 percent of GDP.”

Posted by at 2:06 PM

Labels: Inclusive Growth

An overview of the Bahamian labor market

A new IMF country report says that “The Bahamas has experienced persistently high unemployment rates, averaging over 10 percent, in the past 2 decades. The youth unemployment rate has been stubbornly high, falling only to 22 percent in November 2017. […] It argues that labor market regulations do not appear to be the main culprit of high unemployment, whereas the narrow economic base, the insufficient skill sets among the young, and inefficient job placement services appear to be more important factors. Therefore, expanding vocational and apprenticeship programs should help reduce the youth unemployment rate. Improving skill databases and job placement services more generally should help improve the matching process between employers and job seekers. More broadly, enhancing the quality of general education should facilitate sustaining employment in the long term.”

A new IMF country report says that “The Bahamas has experienced persistently high unemployment rates, averaging over 10 percent, in the past 2 decades. The youth unemployment rate has been stubbornly high, falling only to 22 percent in November 2017. […] It argues that labor market regulations do not appear to be the main culprit of high unemployment, whereas the narrow economic base, the insufficient skill sets among the young, and inefficient job placement services appear to be more important factors.

Posted by at 2:01 PM

Labels: Inclusive Growth

Monday, May 14, 2018

IMF Global Debt Database

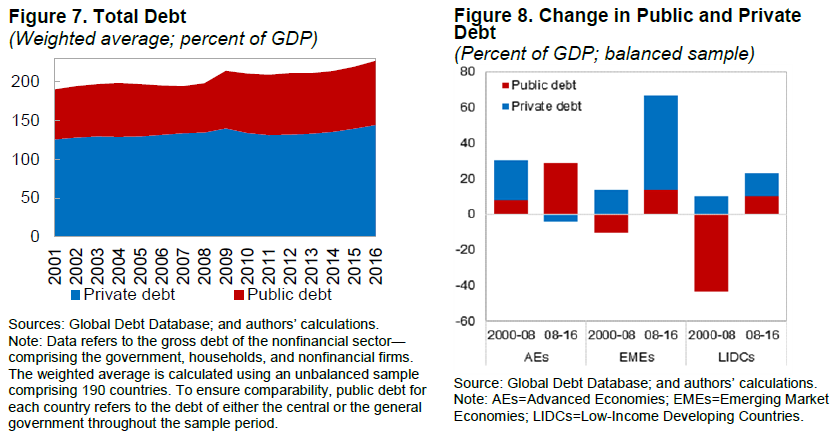

A new IMF working paper “describes the compilation of the Global Debt Database (GDD), a cutting-edge dataset covering private and public debt for virtually the entire world (190 countries) dating back to the 1950s. The GDD is the result of a multiyear investigative process that started with the October 2016 Fiscal Monitor, which pioneered the expansion of private debt series to a global sample. It differs from existing datasets in three major ways. First, it takes a fundamentally new approach to compiling historical data. Where most debt datasets either provide long series with a narrow and changing definition of debt or comprehensive debt concepts over a short period, the GDD adopts a multidimensional approach by offering multiple debt series with different coverages, thus ensuring consistency across time. Second, it more than doubles the cross-sectional dimension of existing private debt datasets. Finally, the integrity of the data has been checked through bilateral consultations with officials and IMF country desks of all countries in the sample, setting a higher data quality standard.

A new IMF working paper “describes the compilation of the Global Debt Database (GDD), a cutting-edge dataset covering private and public debt for virtually the entire world (190 countries) dating back to the 1950s. The GDD is the result of a multiyear investigative process that started with the October 2016 Fiscal Monitor, which pioneered the expansion of private debt series to a global sample. It differs from existing datasets in three major ways.

Posted by at 8:08 PM

Labels: Inclusive Growth

Subscribe to: Posts