Showing posts with label Global Housing Watch. Show all posts

Friday, January 10, 2020

Housing View – January 10, 2020

On cross-country:

- Asset Bubbles and Global Imbalances – Federal Reserve Bank of Richmond

On the US:

- Dominating Firms Can Depress House Prices as Well as Wages – Wall Street Journal

- Experts predict what the 2020 housing market will bring – Washington Post

- Trump Administration Plans Roll Back of Low-Income Housing Rules – Wall Street Journal

- Our cities don’t have enough affordable housing. Changing this policy will help – CNN

- New Trump Administration Regulations Say That Affordable Housing Is Fair Housing – Reason

- AEI Housing Market Indicators release on September 2019 data – American Enterprise Institute

- Pricey California Targeted in New Effort for Housing Density – Bloomberg

- Home Purchase Sentiment Index Caps Off Strong 2019 Near Its Survey High – Fannie Mae

- How Wealthy Towns Keep People With Housing Vouchers Out – ProPublica

- Opinion: Unintended consequences: How ‘green’ regulations exacerbate the housing crisis – Market Watch

- As Trump Ditches a Fair Housing Rule, New York City Doubles Down – Citylab

- California Governor Pushes $1.4 Billion Plan To Tackle Homelessness – NPR

- Why The Most Favorable Markets for Tech Expansion Aren’t Where You Might Think – Zillow

On other countries:

- [Brazil] Brazil’s house prices keep falling – Global Property Guide

- [Canada] Canada’s house price boom takes off – Global Property Guide

- [United Kingdom] London house prices link to earnings is ‘almost entirely dislocated’ – Financial Times

- [United Kingdom] UK house price affordability worsens over past decade – Financial Times

On cross-country:

- Asset Bubbles and Global Imbalances – Federal Reserve Bank of Richmond

On the US:

- Dominating Firms Can Depress House Prices as Well as Wages – Wall Street Journal

- Experts predict what the 2020 housing market will bring – Washington Post

- Trump Administration Plans Roll Back of Low-Income Housing Rules – Wall Street Journal

- Our cities don’t have enough affordable housing.

Posted by at 5:00 AM

Labels: Global Housing Watch

Thursday, January 2, 2020

Housing View – January 2, 2020 [2020 AEA Annual Meeting Special Edition]

Below is a preliminary list of papers that will presented at this year’s AEA Annual Meeting on January 3-5 in San Diego, California.

On housing and cycles

- Housing Cycles and Exchange Rates – Paper

- Is the Behavior of Sellers with Expected Gains and Losses Relevant to Cycles in House Prices? – Paper

- China’s Housing Bubble, Infrastructure Investment, and Economic Growth – Paper and Presentation

- Black-Cat Markets and the Value of Superstition: Evidence from Housing Prices in China – AEA

- Regional housing market risk – AEA

- ‘Memory’ in the Middle: Housing Price – Macroeconomic Interactions in the United States – Paper

- The Impact of Parental Wealth on College Enrollment & Degree Attainment: Evidence from the Housing Boom & Bust – AEA

- Villains or Scapegoats? The Role of Subprime Borrowers in Driving the United States Housing Boom – Paper

- Property Tax Limits and Female Labor Supply: Evidence from the Housing Boom and Bust – AEA

- Local House Price Comovements – Paper

- How Auctions Amplify House-Price Fluctuations – Paper

- Unemployment and the United States Housing Market during the Great Recession – AEA

On housing and credit

- Mortgage Credit and Housing Markets – Paper

- Mortgage Debt, Consumption, and Illiquid Housing Markets in the Great Recession – Paper

- The Geography of Mortgage Lending in Times of FinTech – Paper

- Credit Surface of Mortgage Loans: Lenders’ Belief of Housing Markets – AEA

- Concentration and Lending in Mortgage Markets – AEA

- Policy Uncertainty and Bank Mortgage Credit – Paper and Presentation

On housing policy

- The Macroprudential Toolkit: Effectiveness and Interactions – Paper

- Aggregate and Distributional Impacts of Housing Policy: China’s Experiment – Paper

- Unintended Consequences of LTV Limits on Credit and Housing Choices – Paper

- Sticky Expectations in the Housing Market: Evidence from the Housing Purchase Restriction Policy – AEA

- Harping on about HARP: Consequences of Ineligibility for the Home Affordable Refinance Program – Paper

- The Anatomy of the Transmission of Macroprudential Policies – Paper

- Comparing the PRA Program to Other Housing Options for People with Disabilities – AEA

- Targeting In-Kind Transfers through Market Design: A Revealed Preference Analysis of Public Housing Allocation – AEA

- Bank Capital Requirements and Asset Prices: Evidence from the Swiss Real Estate Market – Paper

On housing affordability

- (Why) Are Housing Costs Rising? – Paper

- Affordable Housing and City Welfare – Paper

- Do More Housing Units Reduce Nearby Rents? – AEA

- Procyclical Price-Rent Ratios: Theory and Implications – Paper

- Religion, Ideology, and Housing Affordability: Israeli Settlement of the West Bank – Paper

- Highly Disaggregated Land Unavailability – Paper

On housing and evictions

- Does Eviction Have Spillovers on Children? – AEA

- Housing Insecurity, Homelessness and Populism: Evidence from the UK – Paper

- Measuring Housing Stability with Consumer Reference Data – AEA

On housing, investors, and speculation

- Investors and Housing Affordability – Paper

- Fundamental and Speculative Demands for Housing – AEA

- S. Housing as Global Safe Haven Asset: Evidence from China Shocks – Paper

- Capital Flows, Asset Prices, and the Real Economy: A “China Shock” in the US Real Estate Market – AEA

- Capital Flows, Real Estate, and City Business Cycles: Micro Evidence from the German Boom – AEA

On housing and the sharing economy

- Does bike sharing increase house prices? Evidence from micro-level data in Shanghai – Paper and Presentation

- The Last Mile Matters: Impact of Dockless Bike Sharing on Subway Housing Price Premium – Paper

- Airbnb and Private Investment in Chicago Neighborhoods – Paper

On housing, the environment, and natural disasters

- Perception Versus Reality: The Noise Complaint Effect on Home Values – Paper

- How Much Does Nearby Blight Affect Real Estate Prices? The Case of Hurricane Sandy – Paper

- Dust Storms, Migration and Housing Markets – AEA

On housing and migration

- A Tale of Two Cities: The Impact of Cross-Border Migration on Hong Kong’s Housing Market – Paper and Presentation

- A World Divided: Refugee Centers, House Prices, and Household Preferences – Paper and Presentation

- The Real Estate Consequences of Immigration Shocks: Evidence from the United States’ Mexican Repatriation – AEA

- Residential Segregation and Ethnicity – AEA

- Immigration and Housing Rents: The 2015 Refugee Crisis in Germany – AEA

On housing and everything else

- The Role of Agents in Tax Evasion: Evidence from the Housing Market in China – Paper

- Inside Job: Evidence from the Chinese Housing Market – Paper

- On the Differential Impact of the Tax Cuts and Jobs Act on the Housing Market: Blue versus Red – Paper and Presentation

- Shifting House Price Gradients: Evidence Using Both Rental and Asset Prices – Paper

- Local Constant-Quality Housing Market Liquidity Indices – Paper

- Do Elderly Individuals Delay Claiming Social Security and Cash-out Home Equity When House Prices Appreciate? – Paper

- Street Name Fluency and Housing Prices – Paper and Presentation

- Picture and Playground: Valuing Coastal Amenities – Paper

- Endowments and Minority Homeownership – Paper

- Heterogeneous Households and Market Segmentation in a Hedonic Framework – Paper and Presentation

- Housing Search Frictions: Evidence from Detailed Search Data and a Field Experiment – AEA

- Housing Wealth, Bequests, and the Elderly – Paper

- Public Transport, Noise Complaints, and Housing: Evidence from Sentiment Analysis in Singapore – Paper and Presentation

- The Most Wonderful Time of the Year? Thin Markets, House Price Seasonality, and the December Discount – Paper

- Do School Shootings Erode Property Values? – Paper

- Collateral Value and Entrepreneurship: Evidence from a Property Tax Reform – Paper

- Tracing the Source of Liquidity for Distressed Housing Markets – Paper

- Neighborhood housing rent index construction and spatial discontinuity: a machine learning approach – Paper

- A Tale of Two Cities: The Impact of Cross-Border Migration on Hong Kong’s Housing Market – Paper and Presentation

*AEA indicates that neither the paper or presentation is available at the moment.

Below is a preliminary list of papers that will presented at this year’s AEA Annual Meeting on January 3-5 in San Diego, California.

On housing and cycles

- Housing Cycles and Exchange Rates – Paper

- Is the Behavior of Sellers with Expected Gains and Losses Relevant to Cycles in House Prices? – Paper

- China’s Housing Bubble, Infrastructure Investment, and Economic Growth – Paper and Presentation

- Black-Cat Markets and the Value of Superstition: Evidence from Housing Prices in China –

Posted by at 2:00 AM

Labels: Global Housing Watch

Friday, December 13, 2019

Housing View – December 13, 2019

On cross-country:

- Q3 2019: The global house price boom continues strong, especially in Europe, but sharp slowdown in North America, the Middle East and some parts of Asia-Pacific – Global Property Guide

- Prime Global Cities Index Q3 2019 – Knight Frank

On the US:

- Bold Predictions for 2020: Shrinking Homes and a More Stable Market – Zillow

- These Housing Markets Could Heat Up (Podcast) – Bloomberg

- Fix California’s Housing Crisis, Activists Say. But Which One? – Citylab

- A Modest Proposal: How Even Minimal Densification Could Yield Millions of New Homes – Zillow

- Mapping America’s Metropolitan Growth: Islands of Density in a Sea of No Growth – Zillow

- Home Purchase Sentiment Rebounds in November, Re-Approaches Survey High – FannieMae

- Home Equity in Retirement – Philadelphia Fed

- Owner-Occupancy Fraud and Mortgage Performance – Philadelphia Fed

- Opinion: To solve the problem of unaffordable entry-level housing, abolish single-family zoning – MarketWatch

- Vouchers can help the poor find homes. But landlords often won’t accept them. – VOX

- Fannie and Freddie Need Fixing — Urgently: A Response to Joe Nocera – Cato Liberty

- Release: New Carpenter Index developed by AEI Housing Center – American Enterprise Institute

- “Decommodifying” Housing and Other Magical Thinking – E21

- Tenants are winners in Manhattan’s oversupplied luxury home market – Financial Times

On other countries:

- [China] China’s Housing Market Goes the WeWork Way—and Thousands Get Evicted – Wall Street Journal

- [Israel] Does Location Matter? Evidence on Differential Mortgage Pricing in Israel – Bank of Israel

- [Lithuania] Lithuania’s modest house prices increase – Global Property Guide

- [Netherlands] Netherlands’ house price growth slowly decreasing – Global Property Guide

- [Norway] Norway’s financial stability as risk from household debt, property prices -regulator – Reuters

*Please note that Housing View will be on hiatus for the next three weeks.

On cross-country:

- Q3 2019: The global house price boom continues strong, especially in Europe, but sharp slowdown in North America, the Middle East and some parts of Asia-Pacific – Global Property Guide

- Prime Global Cities Index Q3 2019 – Knight Frank

On the US:

Posted by at 5:00 AM

Labels: Global Housing Watch

Tuesday, December 10, 2019

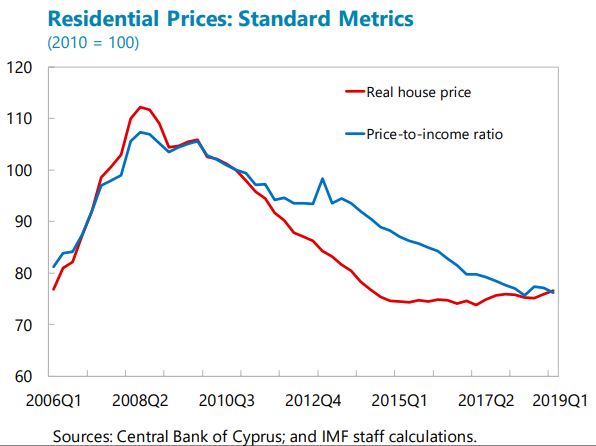

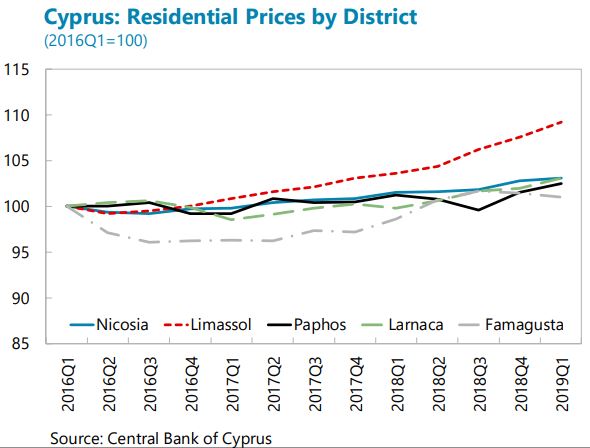

Housing Market in Cyprus

From the IMF’s latest report on Cyprus:

“Property prices are rising gradually but unevenly across markets (…). Rising demand for housing and business offices is being met with increasing supply from new construction, as evidenced by the rising issuance of building permits, and release of repossessed collateral properties by banks. Real estate holdings by banks, CACs and investment funds have also increased. Overall residential prices grew by 2.7 percent (yoy) in 2019:Q1 while sales transactions rose by nearly 6 percent during 2018.14 The property market remains highly segmented, however, with higher price increases observed primarily in a growing luxury segment in some coastal areas (e.g., Limassol), fueled by the CIP-linked demand from non-residents, with limited spillovers to other segments so far. Rents have been rising rapidly—17 percent in 2018— mainly driven by the growing demand from foreign students and lagging supply of rental property investments, prompting the authorities to increase rental and housing subsidies and a range of incentives for developers to increase supplies of affordable housing and rental properties.

Macro-financial risks from the property market appear limited now but warrant close monitoring. While the sales of repossessed collateral properties by banks and CACs could potentially depress prices, downward pressures from such sales have not been evident in any market segments. However, it is important to continue monitoring sectoral and regional real estate market developments, considering the segmented nature of the market. Macroprudential measures tailored to the market segment should be undertaken if warranted, e.g. if the luxury sales become associated with rapid credit growth or high loan-to-value ratios. On the supervisory front, continued monitoring is needed on the large holdings of repossessed real estate by banks and CACs, to discourage and limit the risk of excessive holding of foreclosed properties. Also, the increased real estate holding by investment funds warrants close monitoring to mitigate risks related to liquidity mismatches. Supervisory tools, in particular Pillar 2 requirements and explicit bank-specific objectives, should continue to be used to discourage excessive holding of foreclosed properties by banks.”

From the IMF’s latest report on Cyprus:

“Property prices are rising gradually but unevenly across markets (…). Rising demand for housing and business offices is being met with increasing supply from new construction, as evidenced by the rising issuance of building permits, and release of repossessed collateral properties by banks. Real estate holdings by banks, CACs and investment funds have also increased. Overall residential prices grew by 2.7 percent (yoy) in 2019:Q1 while sales transactions rose by nearly 6 percent during 2018.14 The property market remains highly segmented,

Posted by at 11:01 AM

Labels: Global Housing Watch

Monday, December 9, 2019

A Look at Housing Affordability in Asia

Global Housing Watch Newsletter: December 2019

In this interview, Matthias Helble talks about the state of housing affordability in Asia, the causes and consequences of worsening housing affordability, and policies to address housing affordability issues. Matthias is an Economist in the Economic Research and Regional Cooperation Department at the Asian Development Bank.

On the state of housing affordability

Hites Ahir: In the latest issue of the Asian Development Outlook, you talk about affordable housing in the region. What is the state of housing affordability?

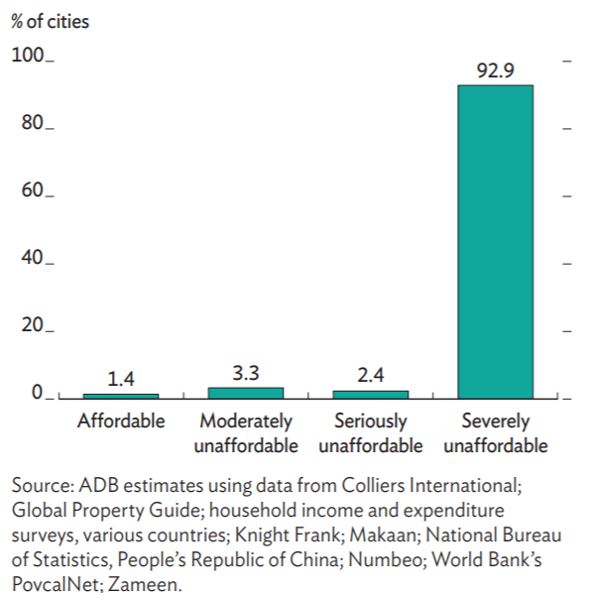

Matthias C. Helble: The state of housing affordability looks very dire. We collected detailed housing price data from public and private sources for 211 cities in 27 countries in developing Asia. Combining them with household income data, we calculated the price-to-income ratio (PIR) by city. Our results show that on average the PIR is 15.6, indicating that housing is severely unaffordable. The unaffordability is not only limited to large cities (with more than 5 million inhabitants), but also affects smaller cities (with less than 1 million inhabitants). Furthermore, we cannot see systematic differences across subregions in Asia. Cities in all subregions suffer equally, be it in Central Asia, East Asia, South East Asia, South Asia, or the Pacific. The housing unaffordability stretches from West to East, from Karachi, Kathmandu, Dhaka, and Bangkok to Dili (Timor-Leste), and from South to North starting from Jakarta, Ha Noi, and Vientiane, to Beijing and Ulaanbaatar.

Figure 1: Housing affordability in 211 cities in 27 countries in Asia

HA: How do you measure housing affordability?

MH: We measure housing affordability by the price-to-income ratio (PIR), which is probably the most commonly used indicator of housing affordability. It is the ratio of the housing unit price over the annual median household income. Demographia International suggests the following cut-offs: A PIR of below 3 is considered to indicate affordable housing. Housing is moderately unaffordable if the PIR is 3 to 4. For example, cities in developed countries have a PIR averaging 4.0. If the PIR is above 4.1, housing is considered seriously unaffordable, and a PIR above 5 indicates that housing is severely unaffordable. In our sample of 211 cities, we only found three cities (Hubli Dharwad in India, Khulna in Bangladesh, and Timphu in Bhutan) that have affordable housing.

HA: The level of income in a city tends to be higher than in the rest of the country. Do you think the results might be overstating the deterioration of housing affordability in the region?

MH: It is indeed a challenge to obtain household income data at the city-level. For several countries, we had access to household income and expenditure surveys (HIES) at the city-level (or a geographical unit that was dominated by a single city). We could thus control for the fact that the level of income is higher in cities. For the remaining countries in our sample, we made use of the positive relationship between city size and income and adjusted the national household income upward using a regression-based approach. Apart from the challenge of adjusting national household income to city size, the HIES data itself might not always accurately report the entire income of a household. An underreporting of household income would lead to an overstatement of the housing affordability problem. In order to test the sensitivity of our results, we developed various scenarios, for example assuming that the real household income was 25 percent higher. Running these tests, we found that housing remained severely unaffordable in most cities in our sample because the housing prices are simply very high.

On the causes and consequences

HA: What is driving the deterioration in housing affordability?

MH: The main driver is the rapid urbanization in Asia, alongside economic success. The demand for housing is thus increasing rapidly while the supply is lagging. Cities have been slow in expanding the availability of low-cost developable land with access to public amenities and transport. The land price of well-served and centrally located areas is thus spiraling. At the same time, we see a lot of unplanned, even chaotic, urban expansion. Another aggravating factor is that in Asia almost everybody aspires to become a homeowner and the rental market is still relatively small in most cities in developing Asia.

HA: What does the literature say about the consequences of a deterioration in housing affordability?

MH: The unaffordability of housing has severe consequences beyond the negative impact on the individual household. Housing unaffordability damages the economic competitiveness of cities and thus can undermine the growth prospects of the entire country. We have solid empirical evidence of three main channels through which housing unaffordability affects the economy:

- First, housing unaffordability results in a less flexible labor market and thus leads to labor misallocation.

- Second, as housing prices rise, firms tend to invest in real estate rather than in innovation and productivity enhancement. Furthermore, banks tend to lend more to firms that have real estate assets instead of the best business prospects, resulting in capital misallocation.

- Third, high housing prices deter people from moving to the city. Housing unaffordability thus slows the process of urbanization and thereby reduces agglomeration-induced productivity growth and aggregate welfare.

On the cures

HA: What policies have been implemented in Asia?

MH: A wide range of policies have been tried throughout Asia. The table below provides some examples. It is important not to expect that the same housing policy would work equally across countries. For example, an idle land tax boosted the construction of housing after the Second World War. The same policy today is not having much effect in the Philippines due to uncertain land titles.

Table 1: Main policy options used in Asia toward affordable housing

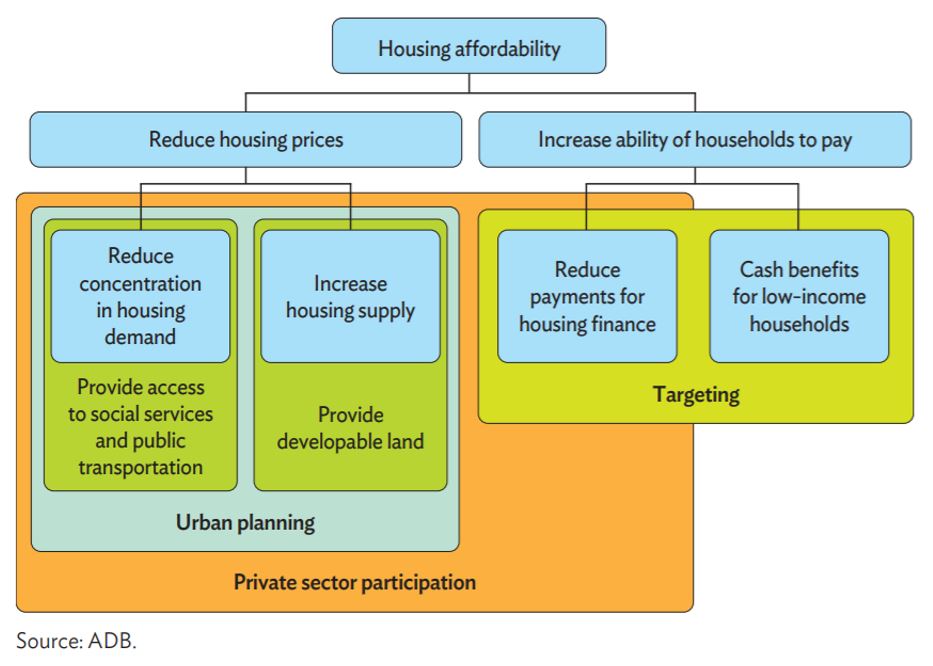

HA: Is there a framework that policymakers can use to address housing affordability issues?

MH: There is no specific framework, rather we have some recommendations.

- First, the housing unaffordability crisis cannot be solved by the public sector alone. The private sector needs to be part of the solution, notably through the provision of low-cost housing. Governments need to provide incentive schemes to encourage that.

- Second, the best housing policies will flounder if the policy implementation and enforcement is weak. This has been the case in many developing countries.

- Finally, we are living in an age in which an incredible amount of data on the housing market and related issues is becoming available. Collecting and analyzing the data and feeding the results into the policy process could greatly improve the effectiveness of housing policies.

Figure 2: Housing policy option tree

HA: Do you think that most of the discussion on affordable housing tends to be around “increasing housing supply” and not concentrating much on other important elements such as affordable transport, upgrading slums, and others? Please explain your opinion.

MH: Increasing housing supply alone will certainly not solve the problem. Similar to other policy areas, there is insufficient coordination between the line ministries responsible for housing and other ministries. Housing policies need to be well embedded into urban planning. Integrated neighborhoods need to be developed with access to social services, such as education and healthcare, as well as transport. Another problem is that we do not yet have enough sound evidence on many aspects of housing prices such as how access to transport affects housing prices in developing countries. Thanks to the emergence of big data, I am convinced that a lot of new interesting insights will soon be uncovered. At the Asian Development Bank, we are already working with big data to measure traffic congestion and travel time, for example.

HA: Is there a success story that you could share with us?

MH: A case that is often cited is Singapore. Yet there are other less well-known, but still very valuable, examples, such as in South Korea. Due to fast economic growth in the 1980s, South Korea witnessed a sharp increase in housing prices in its major cities. The government responded by announcing the “Two-Million Housing Drive,” promising to build 2 million new housing units within 5 years. It achieved the objective through a mix of public and private action. The government also introduced a successful policy of allocating housing units to target income groups according to their ability to pay. This approach improved housing conditions, both in terms of quantity and quality, and helped the middle class to build their wealth through house ownership. The country’s housing policy was also well integrated into urban planning so supply constraints were quickly removed. While certainly not without challenges, South Korea provides a useful example of how to tackle housing affordability.

Global Housing Watch Newsletter: December 2019

In this interview, Matthias Helble talks about the state of housing affordability in Asia, the causes and consequences of worsening housing affordability, and policies to address housing affordability issues. Matthias is an Economist in the Economic Research and Regional Cooperation Department at the Asian Development Bank.

On the state of housing affordability

Hites Ahir: In the latest issue of the Asian Development Outlook,

Posted by at 5:00 AM

Labels: Global Housing Watch

Subscribe to: Posts