Showing posts with label Global Housing Watch. Show all posts

Tuesday, October 12, 2021

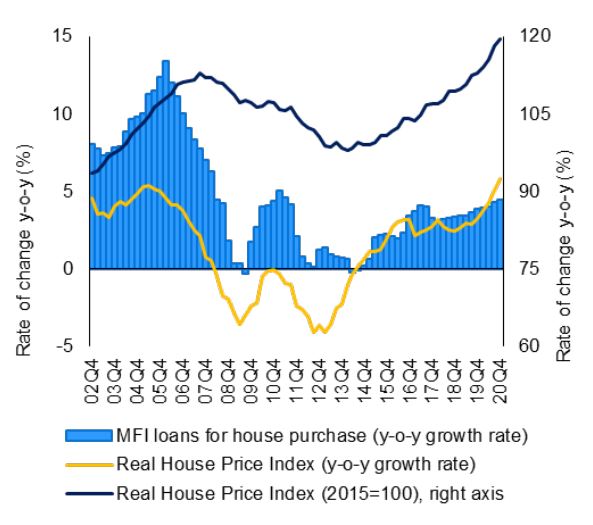

Euro Area Housing Markets: Trends, Challenges and Policy Responses

From a new paper by Vítor Martins, Alessandro Turrini, Bořek Vašíček, and Madalina Zamfir:

“The paper discusses the relevance of housing markets for macroeconomic developments from a euro area perspective, reviews trends in house prices and mortgage credit, and discusses policy approaches to prevent housing booms and deal with busts. After years of unsustainably strong house price growth in several Member States in a context of easing credit conditions, downward house price corrections took place after the 2008 financial crisis. A recovery in house prices started after 2013 under different conditions compared with the pre-financial crisis context. The house price recovery appeared to be driven to a greater extent by structural factors and to a lesser extent by buoyant household loans, as credit growth has been lagging behind house price growth in most countries. Prospects for house price growth after the COVID-19 outburst are clouded by uncertainty in light of the changing outlook when economic fundamentals and policy responses play in opposite directions. The current context is also different compared with the period before the global financial crisis because macro-prudential frameworks have been strengthened and macroprudential tools are increasingly used across the euro area. The effectiveness of policy tools needed to address risks linked to boom-bust dynamics in the real estate sector depends on their interaction, design and timely implementation. Policy composition and policy design also appear crucial in dealing with possible trade-offs among policy objectives, including between macro-financial stability and housing affordability.”

From a new paper by Vítor Martins, Alessandro Turrini, Bořek Vašíček, and Madalina Zamfir:

“The paper discusses the relevance of housing markets for macroeconomic developments from a euro area perspective, reviews trends in house prices and mortgage credit, and discusses policy approaches to prevent housing booms and deal with busts. After years of unsustainably strong house price growth in several Member States in a context of easing credit conditions, downward house price corrections took place after the 2008 financial crisis.

Posted by at 7:20 AM

Labels: Global Housing Watch

Friday, October 8, 2021

Housing View – October 8, 2021

On cross-country:

- City house prices outpace national markets. Predictions of ‘the death of the city’ now seem a distant memory as cities are now outpacing their national housing markets with prices rising by 9.8% on average in the year to Q2 2021. – Knight Frank

- Berliners Are Angry About Housing. And So Is Much of Europe. Soaring rents and out-of-reach prices have fueled property inequality – Bloomberg

- Sergei Gordeev: the Russian property tycoon betting on prefabricated blocks. Having netted billions of dollars from a housing boom, PIK’s chief executive wants to upend the sector – FT

On the US:

- It Shouldn’t Take 50 Meetings to Build Some Apartments – New York Times

- Why Isn’t There Enough Housing? Zoning And Homeowner Resistance – Forbes

- Eviction Record Expungement Can Remove Barriers to Stable Housing – Center for American Progress

- California’s Smart Plan to Let Homeowners Be Homebuilders. The way to blunt Nimby resistance to badly needed housing construction is to give single-family owners a path to profit from new development. – Bloomberg

- Why Democrats Would Be Fools to Slash Biden’s Housing Plan. Lawmakers will have to make tough decisions to reach a deal on reconciliation. But chopping historic housing investments isn’t the answer. – Politico

- Single-family Zoning: Can History be Reversed? – Harvard Joint Center for Housing Studies

- What Do Runaway Home Prices Mean for the US? – Harvard Joint Center for Housing Studies

- Mortgage Payments Are Getting More and More Unaffordable. Record growth in home prices is erasing savings typically delivered by low interest rates – Wall Street Journal

- The Housing Boom Is Not A Bubble – Forbes

- What’s Driving the Huge U.S. Rent Spike? Rent increases of 20% or more are making life difficult for low-income tenants in many cities, just as eviction bans and unemployment relief are running out. – Bloomberg

- If your rent is going up, this episode is for you – New York Times

On China

- Empty Buildings in China’s Provincial Cities Testify to Evergrande Debacle. The property giant borrowed heavily to develop in out-of-the way places like Lu’an – Wall Street Journal

- China property sector woes intensify after mid-sized developer defaults. Fantasia misses payment as Evergrande keeps investors hanging on share trading suspension – FT

- Beijing crackdown threatens to crush China’s love of London property. Thousands of high-end flats bankrolled by Chinese developers lie unfinished and unsold – FT

- The economic threats from China’s real estate bubble. Property’s great investment boom has reached its limit — the economy needs new drivers of demand – FT

On other countries:

- [Australia] RBA Remains Dovish, Warns on House Prices. The Australian central bank held the official cash rate at 0.1%, where it has stood since late 2020 – Wall Street Journal

- [Australia] Australia’s house price boom: what’s happening and how can it be brought under control? The property frenzy is locking young people out of the market and creating economic risks. Will anything stop it? – The Guardian

- [Australia] Banks given new borrowing rule as Australian house prices soar. Regulator Apra tells lenders to ensure new mortgagees can cope with three percentage point rise in interest rates – The Guardian

- [Australia] Australia’s flying house prices – a catch-22? – EY

- [Croatia] The effect of housing loan subsidies on affordability: Evidence from Croatia – Journal of Housing Economics

- [Hong Kong] Hong Kong’s Lam to Target Housing Crisis in Policy Address – Bloomberg

- [Hong Kong] Carrie Lam policy address: massive housing plan near Hong Kong’s border to play starring role in speech, but vision has its critics. Blueprint calls for expanding on existing plan for New Territories North and will be comparable in scale with Lantau Tomorrow Vision, sources say. Proposal could make it easier for villagers to sell ancestral land, releasing abandoned farmland and earmarking funds to buy private holdings – South China Morning Post

- [Hong Kong] Hong Kong’s Massive Land Reform Unlikely to Tame Prices for Now – Bloomberg

- [Hong Kong] Hong Kong Developers Surge on Lam’s Northern Metropolis Plan – Bloomberg

- [New Zealand] New Zealand raises rates to rein in property prices and inflation worries. Central bank increases lending rate to 0.5% despite Covid lockdown in Auckland – FT

- [United Arab Emirates] Behind the Sizzle of Dubai Home Boom, Key Vulnerability Persists – Bloomberg

- [United Kingdom] Displaced: The Human Cost of London’s Housing Crunch. The story of Davida Dawkins shows how London’s push to build more affordable housing may still not be enough for its most vulnerable residents. – Bloomberg

On cross-country:

- City house prices outpace national markets. Predictions of ‘the death of the city’ now seem a distant memory as cities are now outpacing their national housing markets with prices rising by 9.8% on average in the year to Q2 2021. – Knight Frank

- Berliners Are Angry About Housing. And So Is Much of Europe. Soaring rents and out-of-reach prices have fueled property inequality – Bloomberg

- Sergei Gordeev: the Russian property tycoon betting on prefabricated blocks.

Posted by at 4:53 AM

Labels: Global Housing Watch

Monday, October 4, 2021

Racial Disparities in Housing Returns

From a NBER working paper by Amir Kermani & Francis Wong:

“We document the existence of a racial gap in realized housing returns that is an order of magnitude larger than disparities arising from housing costs alone, and is driven almost entirely by differences in distressed home sales (i.e. foreclosures and short sales). Black and Hispanic homeowners are both more likely to experience a distressed sale and to live in neighborhoods where distressed sales erase more house value. Importantly, absent financial distress, houses owned by minorities do not appreciate at slower rates than houses owned by non-minorities. Racial differences in income stability and liquid wealth explain a large share of the differences in distress. We use quasi experimental variation in loan modifications to show that policies that restructure mortgages for distressed minorities can increase housing returns and reduce the racial wealth gap.”

From a NBER working paper by Amir Kermani & Francis Wong:

“We document the existence of a racial gap in realized housing returns that is an order of magnitude larger than disparities arising from housing costs alone, and is driven almost entirely by differences in distressed home sales (i.e. foreclosures and short sales). Black and Hispanic homeowners are both more likely to experience a distressed sale and to live in neighborhoods where distressed sales erase more house value.

Posted by at 7:16 AM

Labels: Global Housing Watch

Friday, October 1, 2021

Housing View – October 1, 2021

On cross-country:

- Taking the Global Housing Market’s Temperature: Is It Running a Fever (Again)? – Dallas FED

- Can lending controls solve the problem of unaffordable housing? More central banks are tightening curbs on risky lending. But that is unlikely to make housing much cheaper – The Economist

- For Many Families World-Wide, a Dream Home Is Out of Reach. Calls for action gain support, but policy makers are worried about existing homeowners and the global recovery – Wall Street Journal

- America Risks an ‘Evergrande Moment’. Like China, most of the developed nations have relied too much on property to fuel growth. – Wall Street Journal

- When You’re Locked Out (or Priced Out) of Home – Bloomberg

- Russian Billionaire Behind Top Builder Wants to Disrupt Housing – Bloomberg

On the US:

- Beware the backlash as financiers muscle into rental property. As rents soar, so do the prospects of a regulatory crackdown – The Economist

- Building the future depends on building more housing – Axios

- Housing Vouchers in Economic Recovery Bill Would Sharply Cut Homelessness, Housing Instability – Center on Budget and Policy Priorities

- How Housing Industries Keeps Racism Alive – Bloomberg

On China:

- How a housing downturn could wreck China’s growth model. Evergrande’s woes expose the economy’s unhealthy dependence on property – The Economist

- China Tells Bankers to Support Property Market, Homebuyers – Bloomberg

- China’s Housing Sector Risks Falling Into Bear Market, Citi Says – Bloomberg

- China Oversees Evergrande Accounts to Ensure Housing Gets Built – Bloomberg

- Chinese cities seize Evergrande presales to block potential misuse of funds. State intervention gathers pace as second bond deadline looms for indebted property developer – FT

- PBOC Vows ‘Healthy’ Property Market Amid Evergrande Crisis – Bloomberg

- China’s Property Sector Has Bigger Problems Than Evergrande. Chinese economic troubles may come far faster than the markets expect. – Foreign Policy

On other countries:

- [Australia] Australian housing borrowing booms, regulators ready new lending rules – Reuters

- [United Kingdom] UK house prices forecast to rise by up to 3.5% a year between 2022 and 2024. Summer 2021 marked peak growth but race for space will continue, says estate agent Hamptons – The Guardian

On cross-country:

- Taking the Global Housing Market’s Temperature: Is It Running a Fever (Again)? – Dallas FED

- Can lending controls solve the problem of unaffordable housing? More central banks are tightening curbs on risky lending. But that is unlikely to make housing much cheaper – The Economist

- For Many Families World-Wide, a Dream Home Is Out of Reach. Calls for action gain support, but policy makers are worried about existing homeowners and the global recovery – Wall Street Journal

- America Risks an ‘Evergrande Moment’.

Posted by at 4:59 AM

Labels: Global Housing Watch

Friday, September 24, 2021

Housing View – September 24, 2021

On cross-country:

- The Global Housing Market Is Broken, and It’s Dividing Entire Countries. The dream of owning a home is increasingly out of reach. Democratic and authoritarian governments alike are struggling with the consequences. – Bloomberg

- House prices a persistent pressure on euro zone inflation, ECB study shows – Reuters

- Urban Resilience – NBER

- The role of macroprudential policies during economic crises – BIS

On the US:

- Housing Market Expected to Stay Stable as COVID-era Protections End – Zillow

- Hot U.S. Housing Market Cooled Some in August. Existing-home sales dropped 2% from the prior month as buyers pulled back, supply tightened and prices eased – Wall Street Journal

- Biden Is Trying to Make Housing More Affordable. Without State Action, It’s Not Enough. – Barron’s

- How a Hot Housing Market Exacerbates Inequality. Homeownership is becoming even less attainable as bidding wars, cash offers and racist ideas about buyers further disadvantage people of color. – Bloomberg

- A New Housing Regulator Could Make The American Dream More Accessible For Millions – NPR

- Vacant Homes Aren’t Making Cities Expensive. And vacancy taxes won’t make them affordable. – Reason

- Americans Haven’t Been This Down on Housing Market Since 1982 – Bloomberg

- Builder Confidence Steadies as Material and Labor Challenges Persist – National Association of Home Builders

- Supply and Labor Constraints Continue to Hinder Economic Growth, Home Sales. Rising Inflation Considered a Risk to Mortgage Rates, Housing Affordability – Fannie Mae

- FHFA Capital Rule Listening Session: Using Accessory Dwelling Units to Increase Housing Supply – American Enterprise Institute

- California’s New Housing Laws: Here’s What to Know. Gov. Gavin Newsom has signed two bills aimed at easing the state’s housing crisis. – New York Times

- Why The City Will Survive The Age Of Pandemics And Remote Work – NPR

On China

- Can China’s outsized real estate sector amplify a Delta-induced slowdown? – VoxEU

- China’s property slowdown sends chill through the economy. New homes have anchored growth for decades but Beijing is determined to rein in prices – FT

- The real risk from Evergrande. The main worry is growth, not contagion – FT

- What are the systemic risks of an Evergrande collapse? – The Economist

- Evergrande’s place in China’s house of cards – Atlantic Council

- How Beijing’s Debt Clampdown Shook the Foundation of a Real-Estate Colossus. China Evergrande’s looming collapse and its ripple effect on the economy will pose a test for the government’s campaign to keep housing affordable for the masses – Wall Street Journal

- ‘China’s Lehman Brothers moment’: Evergrande crisis rattles economy. President Xi Jinping faces serious test of his financial reforms as struggles of property giant send ripples through real-estate sector – The Guardian

- Understanding Evergrande, the Chinese Real Estate Conglomerate That’s Nearing Collapse. Can a real estate developer be too big to fail? – Bloomberg

- The knock-on effects of the Evergrande affair. Bringing the real estate sector down to size will slow China’s growth – FT

- China’s mom-and-pop investors, builders and homebuyers caught in Evergrande debt crisis – Reuters

- Evergrande and the end of China’s ‘build, build, build’ model. Valued at $41bn in 2020, the spectacular unravelling of the property group exposes deep flaws in Beijing’s growth strategy – FT

- Potential collapse of Chinese property developer Evergrande could hit Australian iron ore exports. Australian Strategic Policy Institute says Coalition should take pre-emptive action with global trade umpire in case demand for commodity dries up – The Guardian

- China and U.S. Housing Crises: Failures of Central Planning – Cato Institute

- China Macro Property data Update – August – Real Estate Foresight

On other countries:

- [Australia] The Housing Market and Financial Stability – Reserve Bank of Australia

- [Australia] Property Value at Risk in Australian Climate Hot Spots, RBA Says – Bloomberg

- [Australia] RBA Ramps Up Warnings About Soaring House Prices, Instability Risk. The warning comes as Australian house prices are expected to climb by more than 20% in 2021 – Wall Street Journal

- [Australia] Soaring housing debt a financial risk: Reserve Bank – The Sydney Morning Herald

- [New Zealand] Reserve Bank takes action over ‘unsustainable’ house prices. The Reserve Bank (RBNZ) has tightened loan-to-value restrictions in a renewed bid to cool the housing market. – RNZ

- [United Kingdom] U.K. House Prices Stabilize as New Listings to Sell Jump 14% – Bloomberg

On cross-country:

- The Global Housing Market Is Broken, and It’s Dividing Entire Countries. The dream of owning a home is increasingly out of reach. Democratic and authoritarian governments alike are struggling with the consequences. – Bloomberg

- House prices a persistent pressure on euro zone inflation, ECB study shows – Reuters

- Urban Resilience – NBER

- The role of macroprudential policies during economic crises – BIS

On the US:

Posted by at 5:00 AM

Labels: Global Housing Watch

Subscribe to: Posts