Showing posts with label Global Housing Watch. Show all posts

Friday, October 22, 2021

Housing View – October 22, 2021

On cross-country:

- IMF urges caution as house prices surge globally – Irish Examiner

- Creating Housing Markets in Emerging Market Economies – IFC

- Warning: Some Transaction Prices can be Detrimental to your House Price Index – University of Graz

On the US:

- RV Capital of America Tops WSJ/Realtor.com Housing Index in Third Quarter. Index ranks cities for appreciating housing markets and lifestyle amenities – Wall Street Journal

- Construction on new homes slows as supply-chain woes hit the housing market. The number of housing projects completed in September fell to the lowest level in over a year – Market Watch

- U.S. homebuilding stumbles as supply constraints mount – Reuters

- Another upward force on American inflation: the housing boom. Property could join energy, shipping, used cars and wages as a contributor to rising consumer prices – The Economist

- Immediate and Longer-Term Housing Market Effects of a Major U.S. Airport Closure – NBER

- Do Restrictive Land Use Regulations Make Housing More Expensive Everywhere? – Economic Development Quarterly

- Psychoanalyzing the Housing Frenzy With Redfin’s CEO. The emotional and financial stakes of buying a home have never been higher. – Curbed

On China

- China new home prices hit by first month-on-month fall since 2015. Data reveal price decline in big cities in September as weakness in real estate sector reverberates – FT

- Chinese developer Sinic defaults as Evergrande deadline looms. More companies miss debt payments as country’s real estate sector contracts in third quarter – FT

- Evergrande: concerns linger even as embattled developer’s Hengda unit makes interest payment on US$327 million onshore bond. – South China Morning Post

- Evergrande’s debt crisis sates appetite for risk, forcing 206 plots to withdraw from China’s land auctions since September – South China Morning Post

- Housing slowdown threatens China’s economic muscle – Axios

- China’s property and construction sectors contract in third quarter as Evergrande crisis and tougher regulation hit home – South China Morning Post

- In Tackling China’s Real-Estate Bubble, Xi Jinping Faces Resistance to Property-Tax Plan. After negative feedback from within the party, an initial proposal to test a property tax in some 30 cities has been significantly scaled down – Wall Street Journal

- Time for orderly resolution for Evergrande is running out. If the state has a grand plan, it will need to make it known soon – The Economist

On other countries:

- [New Zealand] New Zealand plans new housing density laws to tame red-hot property market – Reuters

- [New Zealand] Sweeping housing legislation could reshape New Zealand cities for decades to come. Housing campaigners welcome changes, saying they will boost businesses, lower emissions and enable better transport links – The Guardian

- [Turkey] Housing prices in emerging countries during COVID-19: evidence from Turkey – International Journal of Housing Markets and Analysis

- [United Kingdom] The problem with new-build property. It loses its premium over time, so mortgage providers are more reluctant to lend to those with small deposits – FT

On cross-country:

- IMF urges caution as house prices surge globally – Irish Examiner

- Creating Housing Markets in Emerging Market Economies – IFC

- Warning: Some Transaction Prices can be Detrimental to your House Price Index – University of Graz

On the US:

- RV Capital of America Tops WSJ/Realtor.com Housing Index in Third Quarter. Index ranks cities for appreciating housing markets and lifestyle amenities – Wall Street Journal

- Construction on new homes slows as supply-chain woes hit the housing market.

Posted by at 5:00 AM

Labels: Global Housing Watch

Friday, October 15, 2021

Housing View – October 15, 2021

On cross-country:

- Euro Area Housing Markets: Trends, Challenges & Policy Responses – European Commission

- Do Foreign Buyer Taxes Affect House Prices? – SSRN

On the US:

- 10th Annual Housing Conference – American Enterprise Institute

- Why the U.S. Housing Boom Isn’t a Bubble – Wharton

- Borrower Expectations and Mortgage Performance: Evidence from the COVID-19 Pandemic – FHFA

- This Year, Half as Many Metro Areas Are Affordable to Low-Income Homebuyers as Last Year – Harvard Joint Center for Housing Studies

- Maxine Waters ready to battle over potential cuts to housing aid. Waters, who proposed the funding as chair of the House Financial Services Committee, said in an interview that “I’m going to fight as hard as I can to keep as much housing as I can in the reconciliation bill.” – Politco

- Millennials Team Up to Fulfill the Dream of Homeownership. Burdened by debt and facing soaring home prices, first-time home buyers are pooling their finances with partners, friends or roommates – Wall Street Journal

- Is There a Relationship Between Regional Unemployment Rates and Older Adult Housing Stability? – Harvard Joint Center for Housing Studies

On other countries:

- [Australia] RBA Says Risks Remain for Excessive Borrowing, House Prices – Bloomberg

- [Australia] RBA Sees Financial Stability Risks From Record-Low Rates, Housing Boom – Wall Street Journal

- China’s Harbin lends hand to property firms; Morgan Stanley upgrades sector view – Reuters

- [United Kingdom] Return of the renters: price hikes, bidding wars and bribes. As cities relax pandemic restrictions and workers move back, competition for rented property is fierce – FT

- [United Kingdom] Boris Johnson’s Housing Headaches Aren’t Over Yet. His Conservative government has signaled it won’t be obsessed with building homes. That’s fine, but Britain still needs more affordable housing. – Bloomberg

- [United Kingdom] Michael Gove urged to address loss of half a million social homes in England. Campaigners challenge new housing secretary to help more than 1m families on waiting list – FT

On cross-country:

- Euro Area Housing Markets: Trends, Challenges & Policy Responses – European Commission

- Do Foreign Buyer Taxes Affect House Prices? – SSRN

On the US:

- 10th Annual Housing Conference – American Enterprise Institute

- Why the U.S. Housing Boom Isn’t a Bubble – Wharton

- Borrower Expectations and Mortgage Performance: Evidence from the COVID-19 Pandemic – FHFA

- This Year,

Posted by at 5:00 AM

Labels: Global Housing Watch

Wednesday, October 13, 2021

Why the U.S. Housing Boom Isn’t a Bubble

Wharton’s Benjamin Keys explains why the red-hot U.S. real estate market isn’t a bubble that’s ready to burst. Home prices are likely to stay high for years to come:

“In Philadelphia, the median home price has risen 48% in the last decade. In Atlanta, the median sale price of a metro home hit an all-time high in June of $372,500. Not to be outdone by big cities, Boise, Idaho, recently ranked as the nation’s most overvalued market, where homes are selling for nearly 81% more than they should.

While the red-hot real estate market is finally showing signs of cooling, its meteoric rise has many Americans wondering if housing prices are a bubble that is about to burst, much like the collapse that triggered the Great Recession.

Wharton real estate and finance professor Benjamin Keys says that’s not the case.

“I come down very strongly against that view. I don’t think that it’s likely that we’re going to see a bubble burst in the way that we saw in 2008, 2009, and 2010,” he said during an interview with Wharton Business Daily on SiriusXM. (Listen to the podcast above.)

Although the frenzied buying and inflated prices are reminiscent of the run-up to the recession, Keys said there are several factors that make the current market different. First, loan standards that were loosened during the bubble are much tighter now, with stringent requirements for good credit, complete documentation, and a sizeable down payment. In contrast, the pre-recession years were pocked with subprime mortgages, low teaser interest rates that ballooned, weak underwriting, negatively amortized construction, and other questionable practices.

Second, the boom of the early 2000s was also driven by a surge in home construction that led to abundant supply. But there’s been a building shortage over the last 10 years, especially in cities with high demand. The result is a supply-demand mismatch that can’t be resolved quickly or easily.

“I think there was a bit of a hangover coming out of that 2000 boom and bust, and we’re underbuilt in a lot of cities where there’s demand for jobs, where there’s demand for housing,” Keys said.”

Continue reading here.

Wharton’s Benjamin Keys explains why the red-hot U.S. real estate market isn’t a bubble that’s ready to burst. Home prices are likely to stay high for years to come:

“In Philadelphia, the median home price has risen 48% in the last decade. In Atlanta, the median sale price of a metro home hit an all-time high in June of $372,500. Not to be outdone by big cities, Boise, Idaho, recently ranked as the nation’s most overvalued market,

Posted by at 10:03 AM

Labels: Global Housing Watch

Tuesday, October 12, 2021

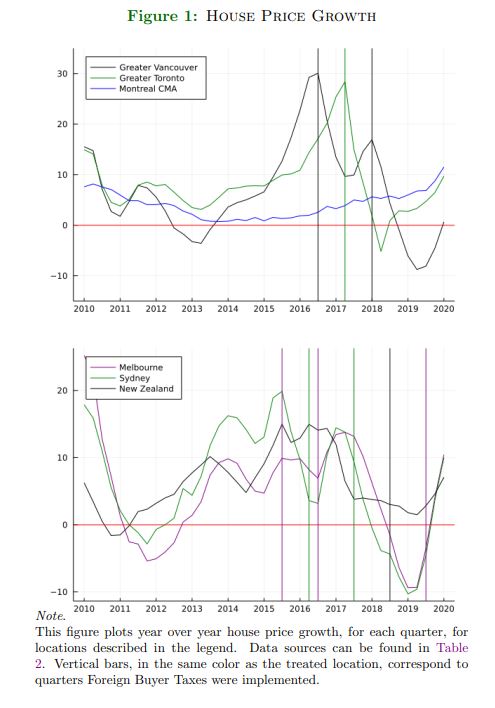

Do Foreign Buyer Taxes Affect House Prices?

From a new paper by Jonathan S. Hartley, Li Ma, Susan Wachter and Albert Alex Zevelev:

“This paper studies the impact of foreign buyer taxes on house prices using recent law changes in Canada, Australia, and New Zealand. Counterfactual house prices are estimated for each treated location combining prediction techniques from machine learning with inference methods from the Synthetic Control Method literature. In general, foreign buyer taxes have negative, large, and persistent effects on house price growth. We find bigger effects in locations with bigger taxes and with higher immigrant shares. Alternative outcome variables, including population growth, GDP growth, and unemployment rates were either unaffected or slightly affected in ways that do not confound our results.”

From a new paper by Jonathan S. Hartley, Li Ma, Susan Wachter and Albert Alex Zevelev:

“This paper studies the impact of foreign buyer taxes on house prices using recent law changes in Canada, Australia, and New Zealand. Counterfactual house prices are estimated for each treated location combining prediction techniques from machine learning with inference methods from the Synthetic Control Method literature. In general, foreign buyer taxes have negative, large, and persistent effects on house price growth.

Posted by at 8:19 PM

Labels: Global Housing Watch

House Prices and Consumer Price Inflation

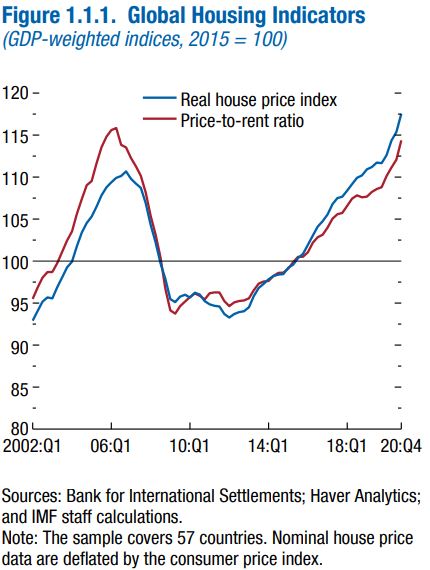

From new work by IMF Colleagues (Nina Biljanovska, Chenxu Fu, and Deniz Igan):

“Contrary to the expectation that house prices would decline during recessions (Igan and others 2011; Duca, Muellbauer, and Murphy, forthcoming), real house prices rose by 5.3 percent, on average, globally in 2020 as the pandemic-induced economic downturn took hold. Perhaps more strikingly, this was the highest annual growth rate observed in the past 15 years (Figure 1.1.1). While house price growth has breezed ahead, residential rents have grown at a slower rate, rising by 1.8 percent, on average, across countries over the same period.

Implications of a hot housing market for consumer prices

The house price surge comes at a time when questions are mounting over post-pandemic inflation dynamics (see Chapter 2). House prices matter for inflation because—through an asset pricing equation—they are linked to two measures of housing costs that could enter the CPI. One is the actual rent paid by tenants. The other is the imputed rent, or owner’s equivalent rent, which is an estimate of how much homeowners would need to pay were they to rent their own house. Overall, the rent component accounts, on average, for about 20 percent of the CPI.

How much of an increase in inflation is expected?“

Continue reading here.

From new work by IMF Colleagues (Nina Biljanovska, Chenxu Fu, and Deniz Igan):

“Contrary to the expectation that house prices would decline during recessions (Igan and others 2011; Duca, Muellbauer, and Murphy, forthcoming), real house prices rose by 5.3 percent, on average, globally in 2020 as the pandemic-induced economic downturn took hold. Perhaps more strikingly, this was the highest annual growth rate observed in the past 15 years (Figure 1.1.1). While house price growth has breezed ahead,

Posted by at 2:14 PM

Labels: Global Housing Watch

Subscribe to: Posts