Showing posts with label Global Housing Watch. Show all posts

Tuesday, January 18, 2022

Fraud and the financial crisis

From a paper by John M. Griffin:

“From the very start of the 2008 housing and financial crisis, close observers suspected widespread fraud lay behind the rapid meltdown in the US mortgage market. But even a decade after the fact, there was little consensus among economists as to whether that was the root cause.

In a paper in the Journal of Economic Literature, author John M. Griffin synthesizes the broad array of literature on the role of residential mortgage-backed securities (RMBS) securitization and finds that conflicts of interest among banks, ratings agencies, and other key players were a key driving force behind the financial crisis.

Griffin says that the process of creating and selling complex financial assets based on home loans was closely linked to the housing bubble—and shot through with malfeasance.

In the run-up to the crisis, underwriters facilitated wide-scale fraud by knowingly misreporting key loan characteristics, credit rating agencies catered to investment banks by inflating their ratings on both mortgage-backed securities and collateralized debt obligations, originators engaged in mortgage fraud to increase market share, and real estate appraisers inflated their appraisals in order to gain business.

As credit was extended to those who could not afford loans, house prices boomed and subsequently crashed when homeowners started defaulting. However, this supply of fraudulent credit was not uniform across US zip codes.

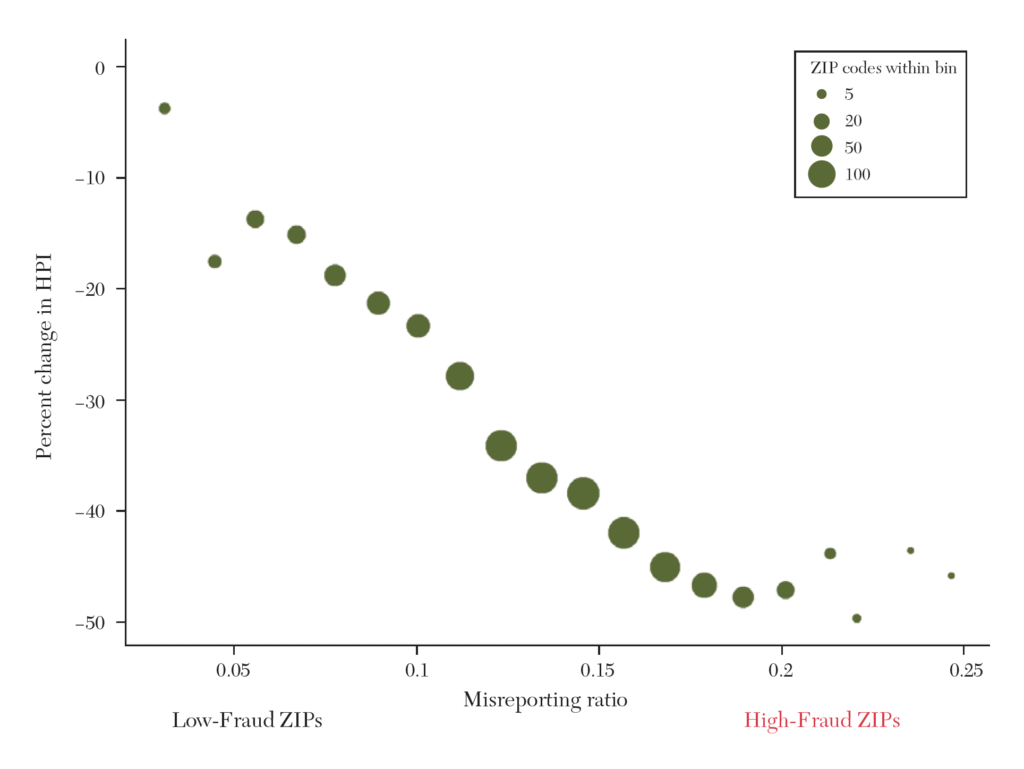

Griffin illustrated variation in mortgage fraud using zip code data from California, which had the greatest number of mortgage originations during the period. Figure 1 from his paper shows that the state’s housing prices decreased as loans from dubious originators increased.

The y-axis is the percent change in the Federal Housing Finance Agency house price index (HPI) per zip code from 2007 to 2010, and the x-axis is the fraction of misreported loans per zip code from 2003 to 2007. The size of each point represents the number of zip codes.

The chart shows a strong negative relationship between misreporting and the home price bust. California zip codes with more than 15 percent fraudulent origination experienced home price decreases of 44.6 percent on average, whereas zip codes with less than 3 percent fraudulent originators only experienced 5.4 percent price decreases.

While other factors such as excess credit and speculation could be drivers, Griffin says that numerous studies since the crisis point toward fraud as a central explanation.”

From a paper by John M. Griffin:

“From the very start of the 2008 housing and financial crisis, close observers suspected widespread fraud lay behind the rapid meltdown in the US mortgage market. But even a decade after the fact, there was little consensus among economists as to whether that was the root cause.

Posted by at 6:48 PM

Labels: Global Housing Watch

Working from home and corporate real estate

From a VoxEU post by Antonin Bergeaud, Jean Benoit Eymeoud, Thomas Garcia, and Dorian Henricot:

“As employers and employees established ways of working remotely to limit physical interaction during outbreaks of Covid-19, teleworking became increasingly routine. This column examines how corporate real-estate market participants adjusted to the growth of teleworking in France, and finds that it has already made a noticeable difference in office markets. In départements more exposed to telework, the pandemic prompted higher vacancy rates, less construction, and lower prices. Forward-looking indicators suggest that market participants believe the shift to teleworking will endure.

One of the primary hysteresis of the Covid-19 pandemic on the organisation of work is probably the dramatic take-off of telework. Forced by circumstances, employers and employees had to implement new ways of working remotely to limit physical interactions during the acute stages of the outbreak. This experience prompted companies to invest more in computer equipment and to adapt their management practices. Teleworking has thus already become a standard practice for many workers and is likely to endure (Barrero et al. 2021).

The polarisation of economic activity has led to a significant increase in real estate prices in dynamic areas. Office real estate is no exception, and the cost of corporate real estate is increasingly weighing on firms’ bottom lines (Bergeaud and Ray 2020). Companies taking advantage of teleworking to reduce office space demand could induce a structural downturn in the corporate real estate market. In the US, Bloom and Ramani (2021) show that the pandemic and the rise of telework is already having a substantial impact on the spatial dynamics of city real estate, producing a ‘doughnut effect’. In a recent study (Bergeaud et al. 2021), we look at the first signs of such an adjustment in France.

Local heterogeneity of the propensity to telework

We first define an index that measures exposure to the deployment of telework at the county (département) level. The index is the product of two components. First, we use the indicator constructed by Dingel and Neiman (2020) at the occupation level and apply it to the local composition of labour in France. We interpret it as a maximum potential for teleworking. However, this upper bound is unlikely to be reached in practice (Bartik et al. 2020). Also, we introduce frictions (quality of the internet infrastructure, average commuting time, number of families with children) that prevent the full use of the telework potential. We extract a principal component from these frictions and combine it with the maximum potential to construct a single index that measures the actual propensity of teleworking by county.”

Continue reading here.

From a VoxEU post by Antonin Bergeaud, Jean Benoit Eymeoud, Thomas Garcia, and Dorian Henricot:

“As employers and employees established ways of working remotely to limit physical interaction during outbreaks of Covid-19, teleworking became increasingly routine. This column examines how corporate real-estate market participants adjusted to the growth of teleworking in France, and finds that it has already made a noticeable difference in office markets. In départements more exposed to telework,

Posted by at 7:07 AM

Labels: Global Housing Watch

Monday, January 17, 2022

The Agglomeration of Urban Amenities: Evidence from Milan Restaurants

From a NBER paper by Marco Leonardi & Enrico Moretti:

“In many cities, restaurants and retail establishments are spatially concentrated. Economists have long recognized the presence of demand externalities that arise from spatial agglomeration as a possible explanation, but empirically identifying this type of spillovers has proven difficult. We test for the presence of agglomeration spillovers in Milan’s restaurant sector using the abolition of a unique regulation that until recently restricted where new restaurants could locate. Before 2005, Milan mandated a minimum distance between restaurants that kept the spatial distribution of restaurants artificially uniform. As a consequence, restaurants were evenly distributed across neighborhoods. The regulation was abolished in 2005 by a nationwide reform that allowed new restaurants to locate anywhere in the city. Using administrative data on the universe of restaurants and retail establishments in Milan between 2000 and 2012, we study how the spatial distribution of restaurants changed after the reform. Consistent with the existence of significant agglomeration externalities, we find that after 2005, the geographical concentration of restaurants increased sharply. By 2012, 7 years after the liberalization of restaurant entry, the city’s restaurants had agglomerated in some neighborhoods and deserted others. By contrast, not much happened to the spatial concentration of retail establishments or even retail establishments that sell food, which were never covered by the minimum distance regulations and therefore were not directly affected by its reform. We also find that in neighborhoods where the number of restaurants grew the most after the reform, restaurants reacted to the increased competition by becoming more differentiated based on price, quality and type of cuisine.”

From a NBER paper by Marco Leonardi & Enrico Moretti:

“In many cities, restaurants and retail establishments are spatially concentrated. Economists have long recognized the presence of demand externalities that arise from spatial agglomeration as a possible explanation, but empirically identifying this type of spillovers has proven difficult. We test for the presence of agglomeration spillovers in Milan’s restaurant sector using the abolition of a unique regulation that until recently restricted where new restaurants could locate.

Posted by at 7:44 AM

Labels: Global Housing Watch

Friday, January 14, 2022

Housing View – January 14, 2022

On cross-country:

- Cross-Country Comparison: Home Rent Growth – Core Logic

On the US:

- There Was No Housing Bubble in 2008 and There Isn’t One Now. Some smart economists are challenging the conventional wisdom that the Great Recession was triggered by out-of-control home prices. – Bloomberg

- Apartment Occupancy Just Hit a Historic High. Is That Good? There’s a silver lining to astronomic U.S. rent hikes: Most tenants won’t pay them, because they’re already locked into their leases. – Bloomberg

- Housing costs swell, hampering home buyers and pushing up rents – New York Times

- Call for Papers: The Mortgage Market Research Conference: Call for Papers – Federal Reserve Bank of Philadelphia

- Mortgage Rates Hit Highest Levels Since Spring 2020. Increase in cost comes after ultralow rates have fueled boom in home sales and prices – Wall Street Journal

- Wall Street Is Using Tech Firms Like Zillow to Eat Up Starter Homes. A business that’s touted as a convenience for home sellers has created a secret pipeline for big investors to buy properties, often in communities of color. – Bloomberg

- People Don’t Want to Move to Shrinking Cities. Slowing population growth could worsen America’s geographic divides, with home prices skyrocketing in some places and plummeting in others. – Bloomberg

- Rising sea levels threaten affordable housing – NPR

- ‘Magic’ Multigenerational Housing Aims to Alleviate Social Isolation. Two co-living communities set to break ground this year seek to address loneliness, as well as the caregiving and affordable-housing shortages, in the U.S. – Wall Street Journal

- U.S. mortgage interest rates surge by most in almost 2 years – Reuters

- Can You Game Your Way Out of American Housing Injustice? A new video game uses a choose-your-own adventure format to interrogate the illusion of choice in the U.S. housing system. – Bloomberg

- There’s Still No Amazon for Housing, But Fintech’s Working on It. Buying and selling a house is a large, complicated transaction, so companies are focusing on making small parts of it easier. – Bloomberg

On China

- China Plans Millions of Low-Cost Rental Homes in Equality Push – Bloomberg

On other countries:

- [Germany] Germany Fights Soaring Home Prices With Curbs on Mortgage Lending. As in the U.S. and other economies, pandemic financial support has sparked a surge in property investment and borrowing in the country – Wall Street Journal

- [Germany] Germany asks banks to build buffers as property market heats up – Reuters

- [Hong Kong] Why Hong Kong housing and office markets are facing very different supply shocks – South China Morning Post

- [United Kingdom] U.K. House Prices Surged Last Year at Fastest Pace Since 2004 – Bloomberg

- [United Kingdom] Help to Buy has pushed up house prices in England, says report. Lords claim flagship £29bn policy would have been better spent on social housing – FT

- [United Kingdom] Letter: Britain must encourage more affordable housing – FT

- [United Kingdom] As the North Cotswolds Get Hipper, Home Values Soar. House prices in this section of the English countryside have risen thanks to the flurry of celebrity residents who have turned the north Cotswolds into the place to see and be seen – Wall Street Journal

On cross-country:

- Cross-Country Comparison: Home Rent Growth – Core Logic

On the US:

- There Was No Housing Bubble in 2008 and There Isn’t One Now. Some smart economists are challenging the conventional wisdom that the Great Recession was triggered by out-of-control home prices. – Bloomberg

- Apartment Occupancy Just Hit a Historic High. Is That Good? There’s a silver lining to astronomic U.S.

Posted by at 5:00 AM

Labels: Global Housing Watch

Tuesday, January 11, 2022

Bloomberg: There Was No Housing Bubble in 2008 and There Isn’t One Now

From Bloomberg:

“Housing markets are red hot, with prices up more than 18% from November 2020 to November 2021. That’s an acceleration over the previous two years, which saw increases of 4% and 8% each. It’s also a faster rate than the U.S. experienced during the housing boom of the 2000s that preceded the Great Recession.

That comparison is causing some heartburn. “Are we in another housing bubble?” asked Mark Zandi, chief economist at Moody’s. The consensus, shared by Zandi, is that the answer is no — or, at least, that today’s bubble is different and less dangerous than the last one. Lending standards are more strict than they were 15 years ago, for example, which ought to mean that fewer homeowners are at risk of defaulting if prices fall.

CNN, though, found a reason for pessimism in that optimism. “The good news is that few economists believe that the current run-up in housing prices is a bubble that’s about to burst, taking the economy down with it,” Chris Isidore of CNN Business wrote on Oct. 27, 2021 before adding ominously, “The bad news is that practically no one was worried about the housing bubble in 2007, either.”

But there’s another reason for sanguinity about the current housing boom: We may have misunderstood the last one all along.

The economists David Beckworth and Scott Sumner have argued that the timing of the last housing bust does not line up with the conventional wisdom that it played a central role in the recession that began in December 2007. The housing market peaked in early 2006, and sustained nearly two years of decline before the economy stopped growing as unemployment stayed low.

Kevin Erdmann — the author of a new book about housing, “Building from the Ground Up,” and a colleague of Beckworth and Sumner at George Mason University’s Mercatus Center — has more recently challenged the claim that the U.S. built too many houses back then. He points out that spending on housing didn’t grow any faster than spending on other consumption goods during the boom (or the preceding decades). The notion that the price increases of 2000-2007 were unsustainable, he points out, also doesn’t match the experience of other countries. The U.K. had a larger increase, a shorter and less severe decline, and a stronger rebound.

Erdmann does not deny that average home prices rose too much in some metropolitan areas during that period. But these spikes were a function of too little homebuilding, not too much. Prices rose fast in two types of cities: those with tight constraints on supply (including New York and San Francisco) and those that dealt with an influx of newcomers from those places (such as Phoenix and Miami). “

Read the full article here.

From Bloomberg:

“Housing markets are red hot, with prices up more than 18% from November 2020 to November 2021. That’s an acceleration over the previous two years, which saw increases of 4% and 8% each. It’s also a faster rate than the U.S. experienced during the housing boom of the 2000s that preceded the Great Recession.

That comparison is causing some heartburn.

Posted by at 10:07 AM

Labels: Global Housing Watch

Subscribe to: Posts