Showing posts with label Global Housing Watch. Show all posts

Friday, March 11, 2022

Housing View – March 11, 2022

On cross-country:

- What happened to global house prices in 2021? – Knight Frank

- Demographia International Housing Affordability 2022 – Demographia

On the US:

- The impact of Treasury’s pilot program on stemming the tide of dirty money into US real estate – Brookings

- Early signs of Russian pullback in real estate – Axios

- The Threat of Environmental Hazards to the Rental Stock – Harvard Joint Center for Housing Studies

- Home mortgage and insurance systems encourage development in climate-risky places, and we all pay the price – Brookings

- U.S. Housing Wealth Skewed Even More Toward Affluent Over Past Decade. From 2010 to 2020, about 71% of increase in housing wealth was gained by high-income households, says National Association of Realtors report – Wall Street Journal

- Stagflation Is Already Here in the Housing Market. Soaring prices and low inventory are causing headaches for homebuilders and buyers but benefiting owners — and therein lies the Fed’s predicament as it seeks to lower inflation. – Bloomberg

On China

- China’s Banking Regulator Welcomes Home Price Adjustments. Guo says current moves are good as long as not too volatile. Home prices have fallen for five months amid industry crisis – Bloomberg

- Shanghai homebuyers looking to capitalise on eased credit policies have to act fast amid expectations of price rise. Eased credit has prompted potential homebuyers to actively chase flats, property agent says. Average price of secondary homes sold last month was 0.5 per cent higher than in January, and 8.5 per cent higher year on year – South China Morning Post

On other countries:

- [Norway] Coming of Age: Renovation Premiums in Housing Markets – SSRN

- [Singapore] Pricey Singapore rents go through the roof even as population dips – Reuters

- [United Kingdom] Help to Buy’s legacy: higher prices and richer builders. Now is a good time to pick over the bones of the UK government’s controversial equity loan scheme – FT

- [United Kingdom] Goodbye Londongrad: Russian Oligarchs Put Pressure on U.K. Property Market. Russian oligarchs stormed London’s high-end property market. Now they are under pressure and so is the city’s real-estate sector. – Wall Street Journal

- [United Kingdom] Cost versus availability of loans: which matters more for mortgagors? – Bank of England

On cross-country:

- What happened to global house prices in 2021? – Knight Frank

- Demographia International Housing Affordability 2022 – Demographia

On the US:

- The impact of Treasury’s pilot program on stemming the tide of dirty money into US real estate – Brookings

- Early signs of Russian pullback in real estate – Axios

- The Threat of Environmental Hazards to the Rental Stock – Harvard Joint Center for Housing Studies

- Home mortgage and insurance systems encourage development in climate-risky places,

Posted by at 5:00 AM

Labels: Global Housing Watch

Thursday, March 10, 2022

Housing market risks in the wake of the pandemic

From a new paper by Deniz Igan, Emanuel Kohlscheen and Phurichai Rungcharoenkitkul:

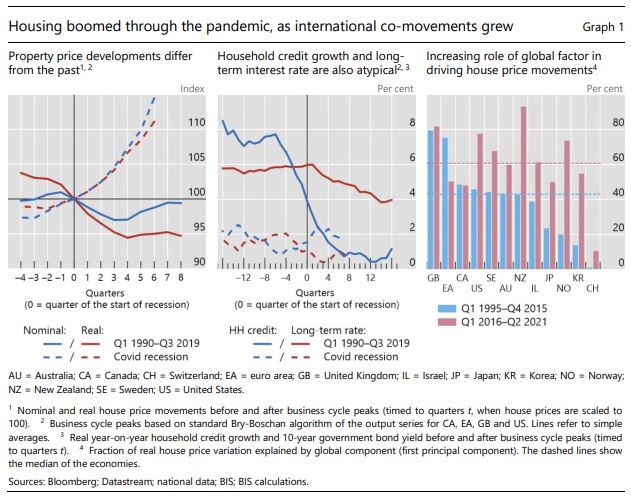

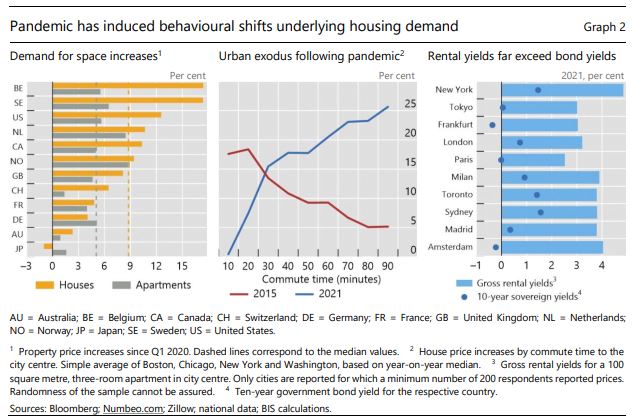

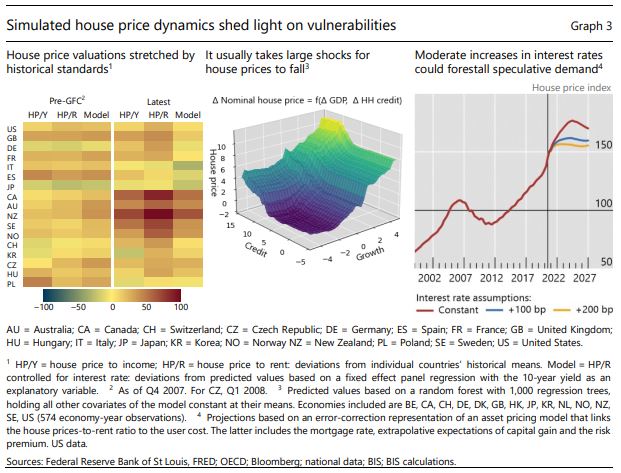

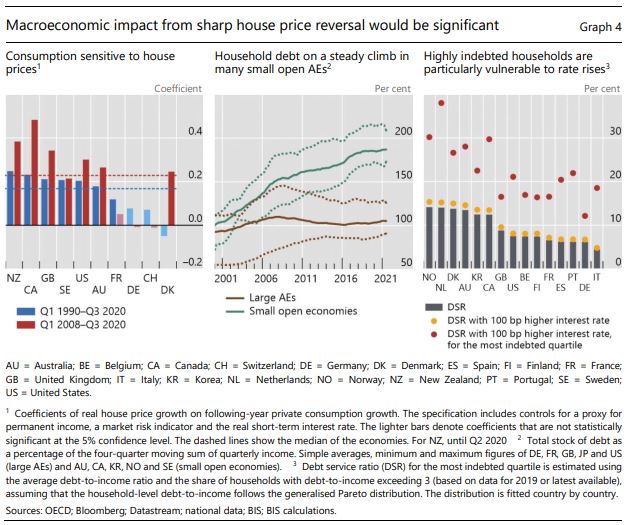

“House prices rose strongly in advanced economies during the pandemic, breaking with typical post-recession patterns. These developments support domestic demand in the short term but carry risks to the outlook if they reverse. Rapid economic recovery, fiscal support and high saving rates amid negative real interest rates explain part of the strong housing demand. Pandemic-induced demand for space, structural supply constraints and increased demand from investors provide additional support for house prices. The monetary policy response to inflationary pressures will be a relevant factor when assessing housing market risks. Moderate increases in interest rates could help forestall speculative demand.”

From a new paper by Deniz Igan, Emanuel Kohlscheen and Phurichai Rungcharoenkitkul:

“House prices rose strongly in advanced economies during the pandemic, breaking with typical post-recession patterns. These developments support domestic demand in the short term but carry risks to the outlook if they reverse. Rapid economic recovery, fiscal support and high saving rates amid negative real interest rates explain part of the strong housing demand. Pandemic-induced demand for space, structural supply constraints and increased demand from investors provide additional support for house prices.

Posted by at 1:50 PM

Labels: Global Housing Watch

Tuesday, March 8, 2022

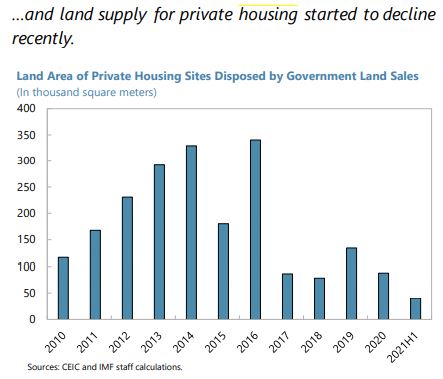

Housing Market in Hong Kong

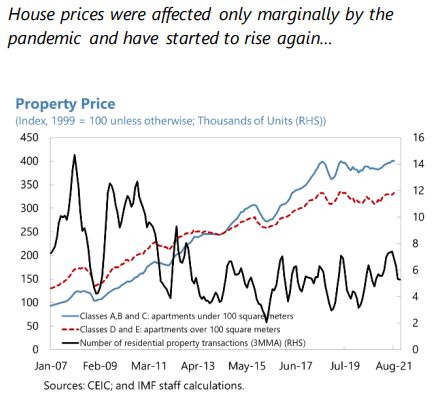

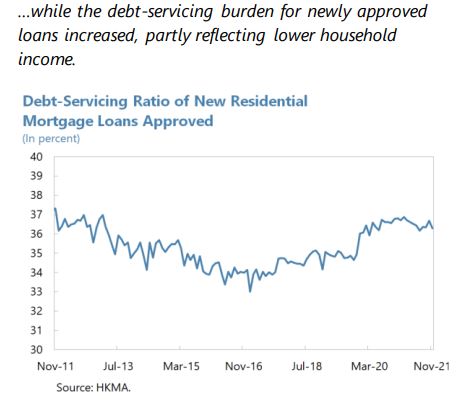

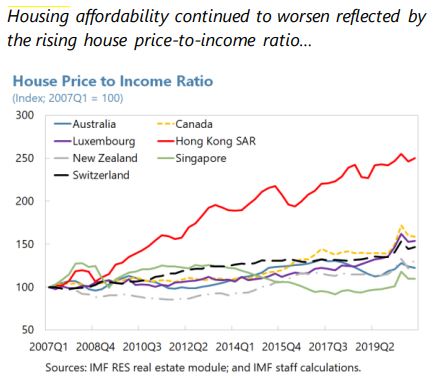

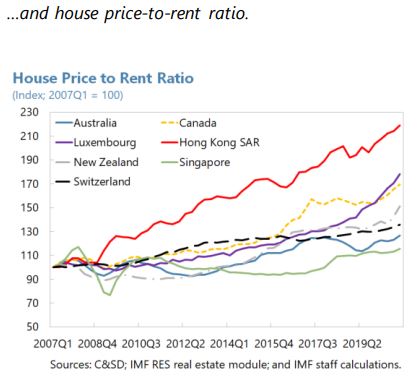

From the IMF’s latest report on Hong Kong:

“Residential house prices are on the rise again, contributing to a further increase in the already elevated level of household debt. The average debt-servicing ratio for new mortgages increased to 36.9 percent at its peak in February 2021 from 36.0 percent in December 2019, partly driven by the decline in household income. While household assets are large in aggregate—as reflected by the high household net worth-to-liabilities ratio of 11.2 times and safe assets-to-liabilities ratio of 2.9 times in 2019—the wealth distribution is skewed towards high-income households.

Given the stretched valuation, a disorderly adjustment in the property market could pose a risk to the economy. A sharp house price correction could trigger an adverse feedback loop between house prices, debt service capacity, household consumption, and growth, negatively affecting banks’ balance sheets. In addition, the FSAP analysis indicated that low-income households could be under significant financial stress when facing rising interest rates and falling income. To mitigate such risks, the authorities should continue to carefully monitor the household debt repayment capacity, particularly for low-income households.

The three-pronged approach to increasing housing affordability and containing housing market risks remains valid, but more efforts are needed to raise housing supply.

*Increasing housing supply is critical to resolve the structural supply-demand imbalance. Housing supply has increased on average since 2015 with the implementation of the government’s Long-term Housing Strategy and the Hong Kong 2030+ Strategy, but has fallen short of target by about 30 percent on average. Staff welcomes the identification of the land to provide 330,000 public housing units within the next ten years and urges the authorities to bring the actual public housing production back to the target without further delays. To this end, a comprehensive approach is urgently needed, including increasing land supply for housing production (e.g., land resumption, reclamation, and re-zoning) while expediting and streamlining the process for land identification and production (e.g., environmental, transport, and other relevant assessments). The recently announced Northern Metropolis development strategy could boost housing supply over the longer-term period.

**The macroprudential stance for property markets should be maintained to safeguard financial stability. A series of macroprudential policies that have been introduced and tightened since 2009—such as ceilings on loan-to-value (LTV) ratio, caps on debt service-to-income ratio (DSR), and stress testing of the DSR against interest rate increases—have helped contain vulnerabilities in the banking system (…). Given resilient house prices and mortgage growth, the existing residential property-related macroprudential policies should be kept unchanged for now and any changes should be data-dependent with due attention to the emerging risk of regulatory leakages. Moreover, the Council of Financial Regulators (CFR) should take the lead in strengthening the regular surveillance and data collection on lending by non-bank lenders (e.g., property developers and non-bank financial institutions), and the authorities should regularly reassess the need to expand the regulatory perimeter to mitigate the leakages in macroprudential policies.

***Stamp duties have been effective in containing speculative activity and external demand. The government has introduced three types of stamp duties to curb excess demand by both residents and nonresidents. Although they have helped curb house price increases and contain household leverage and systemic risks, the New Residential Stamp Duty (NRSD) introduced since November 2016 (…) is a residency-based capital flow management measure and a macroprudential measure (CFM/MPM) levied at a higher rate on non-residents than on first-time resident home buyers. Therefore, staff recommends phasing it out once systemic risks from the non-resident inflow dissipate.

Authorities’ Views

The authorities agreed that increasing land supply remains the key to fundamentally resolving the structural imbalance between housing demand and supply. They emphasized that various measures had been taken to boost land supply for housing production, including by accelerating land resumption and expediting and streamlining the process of land production, and such efforts were starting to bear fruits. The authorities viewed the current tight macroprudential stance for housing market as appropriate given the elevated house prices, while noting that they will continue to closely monitor the housing market and stand ready to make necessary adjustments with a view to safeguarding financial stability. They noted that mortgage lending by non-banks has been closely monitored and has declined in recent years amid the authorities’ efforts to regulate banks’ lending to non-banks and the expansion in the mortgage insurance program.”

From the IMF’s latest report on Hong Kong:

“Residential house prices are on the rise again, contributing to a further increase in the already elevated level of household debt. The average debt-servicing ratio for new mortgages increased to 36.9 percent at its peak in February 2021 from 36.0 percent in December 2019, partly driven by the decline in household income. While household assets are large in aggregate—as reflected by the high household net worth-to-liabilities ratio of 11.2 times and safe assets-to-liabilities ratio of 2.9 times in 2019—the wealth distribution is skewed towards high-income households.

Posted by at 6:53 AM

Labels: Global Housing Watch

Friday, March 4, 2022

Housing markets in Austria and CESEE

From Austrian National Bank:

“The steep upward trend in residential property prices has continued – this was recently confirmed by the Oesterreichische Nationalbank (OeNB) in its Property Market Review Q1/22, which analyzes housing market trends, both in Austria and in Central, Eastern and Southeastern Europe (CESEE). In the fourth quarter of 2021, residential property prices in Austria recorded a year-on-year increase above 10% for the fifth time in a row. House prices in CESEE continued to grow steeply as well, with housing market dynamics raising concerns about financial stability risks in several CESEE countries.

Austria: clear uptrend in house prices continued for the fifth quarter in a row – both in and outside Vienna

In year-on-year terms, price growth remained above 10% in the fourth quarter of 2021 − both in Vienna and in the rest of Austria. In Vienna, prices increased by 11.3%, and prices in the other provinces rose by 13.9%. This means that, for Austria as a whole, house price growth reached a new peak at 12.6% (see table 1).

House prices in Austria increasingly misaligned with fundamentals

With a reading of 29.8% in the fourth quarter of 2021 − 7.6 percentage points higher than in the previous quarter − the OeNB’s fundamentals indicator for residential property prices in Austria showed the sharpest increase since the start of the series in 1989. The indicator for Vienna even came to 35.6%, showing an increase of 5.1 percentage points against the third quarter.

House prices in Central, Eastern and Southeastern Europe grew steeply with growth rates above EU average

In CESEE, house prices rose steeply in the second and third quarter of 2021, with growth remaining above the EU average. House price growth in CESEE was driven by several factors: On the demand side, the overall recovery can be seen as one of the key reasons explaining the house price dynamics observed in the second and third quarter of 2021. Moreover, partly generous government measures to support the purchase of residential property in several CESEE countries pushed up demand for housing. In terms of financing conditions, housing loan growth was supported by low interest rates. Rising construction costs and an overall shortage of input material have constrained the supply of new housing, eventually translating into additional pressure on house prices. Overall, housing market dynamics are raising concerns about financial stability risks in several CESEE countries.”

From Austrian National Bank:

“The steep upward trend in residential property prices has continued – this was recently confirmed by the Oesterreichische Nationalbank (OeNB) in its Property Market Review Q1/22, which analyzes housing market trends, both in Austria and in Central, Eastern and Southeastern Europe (CESEE). In the fourth quarter of 2021, residential property prices in Austria recorded a year-on-year increase above 10% for the fifth time in a row.

Posted by at 7:55 AM

Labels: Global Housing Watch

Tuesday, March 1, 2022

Around the World, Buying Is Costlier Than Renting

From the New York Times:

“A new study compares the costs of renting versus buying a three-bedroom home in 39 countries across the globe.”

From the New York Times:

“A new study compares the costs of renting versus buying a three-bedroom home in 39 countries across the globe.”

Posted by at 3:50 PM

Labels: Global Housing Watch

Subscribe to: Posts