Showing posts with label Global Housing Watch. Show all posts

Friday, June 3, 2022

Housing View – June 3, 2022

On cross-country:

- Will global property prices continue to remain frothy? – BFM

- Financial stability amid Russia’s war in Ukraine – European Central Bank

- Impact of final Basel III on the EU mortgage sector – Copenhagen Economics

- New Housing Supply: Empirical and Theoretical Studies – SSRN

On the US:

- US For-Sale Homes Rise in First Since 2019, Realtor.com Shows – Bloomberg

- U.S. house price inflation to cool as buyers sidelined by higher rates: Reuters poll – Reuters

- Lumber Is the Cheapest in Seven Months as Housing Markets Soften. Futures may sink to as low as $400 per 1,000 board feet, says analyst – Bloomberg

- A recession could throw cold water on the housing market — but that doesn’t mean it’s going to get any easier to buy a home – Business Insider

- Moving From Opportunity: The High Cost of Restrictions on Land Use – Marginal Revolution

- Big U.S. Cities Lost More Residents as Covid-19 Pandemic Stretched On. San Francisco and Chicago population totals are near 2010 levels – Wall Street Journal

- Fed Fears Hit Mortgage Bonds, Attracting Investors. Mortgage REIT Annaly Capital has raised about $3 billion in recent weeks to buy into the battered mortgage-bond market – Wall Street Journal

- County Where It Took 50 Years To Approve New Subdivision Bans New Airbnbs. Officials in Marin County, California, argue a temporary moratorium on new short-term rentals in western portions of the county is necessary to preserve the area’s limited housing stock. – Reason

- Homeownership Remains the American Dream, Despite Challenges. A new survey reveals that nearly three-quarters of Americans place owning a home above career, family and college as a sign of prosperity. – New York Times

- Biden-Harris Administration Launches Initiative to Modernize Building Codes, Improve Climate Resilience, and Reduce Energy Costs – White House

On other countries:

- [Canada] Canada housing boom to halt next year on higher mortgage rates – Reuters poll – Reuters

- [Canada] Ontario needs new housing – and whatever the parties say, it won’t come easy – Globe and Mail

- [New Zealand] New Zealand house prices to sink 9.0% this year, another 2% in 2023 – Reuters

- [Saudi Arabia] Mortgage boom as Saudis queue up to buy first homes. Jump in lending and purchases reflects government push and drive to win support among youth – FT

- [Singapore] Singapore’s sovereign wealth fund swoops for £3.3bn UK student housing deal. Transaction signals confidence in UK rental market despite gloomy economic outlook – FT

- [Singapore] There’s a ‘massive gap’ between housing demand and supply in Singapore, PropertyGuru CEO says – CNBC

- [United Arab Emirates] Foreign demand to keep Dubai property prices on steady upward course: Reuters poll – Reuters

- [United Kingdom] BoE’s Cunliffe seeing evidence of slowdown in housing market – Reuters

- [United Kingdom] Mortgage reform is key to unlocking UK home ownership. The country is a global outlier in managing credit risk – FT

- [United Kingdom] Bringing It Home: Raising Home Ownership by Reforming Mortgage Finance – Tony Blair Institute for Global Change

- [United Kingdom] UK housing market starts to slow as more sellers cut prices. Data from portal Zoopla also indicates average time to sell a home is lengthening – FT

- [United Kingdom] UK mortgage approvals slide to lowest level in two years. Analysts forecast housing market will cool in 2022 but believe large price falls are unlikely – FT

- [United Kingdom] Renters squeezed by higher housing costs and utility bills. Owner-occupiers have more elbow room to reduce their spending to cope with rising inflation, analysis suggests – FT

On cross-country:

- Will global property prices continue to remain frothy? – BFM

- Financial stability amid Russia’s war in Ukraine – European Central Bank

- Impact of final Basel III on the EU mortgage sector – Copenhagen Economics

- New Housing Supply: Empirical and Theoretical Studies – SSRN

On the US:

- US For-Sale Homes Rise in First Since 2019,

Posted by at 5:00 AM

Labels: Global Housing Watch

Thursday, June 2, 2022

Moving From Opportunity: The High Cost of Restrictions on Land Use

From Marginal Revolution:

“People are more productive in cities. As a result, people move to cities to earn higher wages but some of their productivity and wages is eaten up by land prices. How much? In a new paper Philip G. Hoxie, Daniel Shoag, and Stan Veuger show that net wages (that is wages after housing costs) used to increase in cities for all workers but since around 2000 net wages actually fall when low-wage workers move to cities. The key figure is at right.

As I wrote earlier, it used to be that poor people moved to rich places. A janitor in New York, for example, used to earn more than a janitor in Alabama even after adjusting for housing costs. As a result, janitors moved from Alabama to New York, in the process raising their standard of living and reducing income inequality. Today, however, after taking into account housing costs, janitors in New York earn less than janitors in Alabama. As a result, poor people no longer move to rich places. Indeed, there is now a slight trend for poor people to move to poor places because even though wages are lower in poor places, housing prices are lower yet.

Ideally, we want labor and other resources to move from low productivity places to high productivity places–this dynamic reallocation of resources is one of the causes of rising productivity. But for low-skill workers the opposite is happening – housing prices are driving them from high productivity places to low productivity places. Furthermore, when low-skill workers end up in low-productivity places, wages are lower so there are fewer reasons to be employed and there aren’t high-wage jobs in the area so the incentives to increase human capital are dulled. The process of poverty becomes self-reinforcing.

Why has housing become so expensive in high-productivity places? It is true that there are geographic constraints (Manhattan isn’t getting any bigger) but zoning and other land use restrictions including historical and environmental “protection” are reducing the amount of land available for housing and how much building can be done on a given piece of land. As a result, in places with lots of restrictions on land use, increased demand for housing shows up mostly in house prices rather than in house quantities.“

Continue reading here.

From Marginal Revolution:

“People are more productive in cities. As a result, people move to cities to earn higher wages but some of their productivity and wages is eaten up by land prices. How much? In a new paper Philip G. Hoxie, Daniel Shoag, and Stan Veuger show that net wages (that is wages after housing costs) used to increase in cities for all workers but since around 2000 net wages actually fall when low-wage workers move to cities.

Posted by at 10:29 AM

Labels: Global Housing Watch

Friday, May 27, 2022

Housing View – May 27, 2022

On cross-country:

- Drivers of rising house prices and the risk of reversal – European Central Bank

- ECB warns a house price correction is looming as interest rates rise. Central bank says housing market reversal would hit low-income homes harder – FT

- Euro zone’s overpriced housing market may sag if rates rise, ECB says – Reuters

- Has COVID-19 Triggered an Urban Exodus? – OECD

- Asia’s advanced economies now have lower birth rates than Japan. The cost of housing may be the biggest factor – The Economist

- Housing policy and affordable housing – LSE

- Revisiting International House Price Convergence Using House Price Level Data – IDEAS

- Housing and the Labor Market – Oxford Research Encyclopedias

On the US:

- Conference: Housing & Urban Economics on September 7 – Stanford University

- Rising Interest Rates Concern Apartment-Building Owners, Renters. Returns fall below mortgage figures, with landlords needing higher rents to fill the gap – Wall Street Journal

- Housing Boom Is on Borrowed Time. Higher rates have only just begun to weigh on home sales and prices – Wall Street Journal

- The housing market boom has at least another year to run, Zillow economists predict – Fortune

- Fed Searches for the Magic Number to Cool a Red-Hot U.S. Housing Market. The central bank must decide on an interest rate that will cap sky-high price growth without triggering a painful economic slowdown – Wall Street Journal

- How Homeowners Can Lock in the Steep Rise in Home Values. For those who don’t want to sell, there are strategies to use to hedge against a future decline – Wall Street Journal

- In Battle for Workers, Companies Build Houses. Disney, meatpacker JBS and others launch plans to add affordable housing near job sites; a Vail, Colo., project draws opposition – Wall Street Journal

- April Rental Report: Sun Belt Metros Drive Sustained Growth in Nationwide Rents – Realtor

- Housing in America has become much harder to afford. High prices and soaring mortgage rates are putting some buyers off – The Economist

- Did the pandemic advance new suburbanization? – Brookings

- Effective Zoning Reform Isn’t as Simple as It Seems. The Biden administration’s housing plan will reward cities that change their land-use policies to promote density. But what kind of zoning reforms really work? – Bloomberg

- Fed Liquidity Facility Successfully Anchored Commercial Real Estate amid Pandemic – Dallas Fed

- Biden is doubling down on dense, affordable housing – Quartz

- Pandemic Housing Boom Hits a Wall With US Buyers Priced Out. Home values in the Sun Belt boomtowns spiked, but now rising mortgage rates, inflation, and recession fears are starting to pinch. – Bloomberg

- Amid a Housing Crunch, Homes Pop Up on the Fairway. With large expanses of grass and trees, former golf courses are being reconsidered for housing, but developers face challenges, including community resistance. – New York Times

- Housing and Access to Credit Are Two Sides of the Financial Inclusion Coin – San Francisco Fed

- The Household Mystery: Part II – Calculated Risk

- Wall Street’s housing grab continues. As rising rates deter families from buying, being a rentier looks as appealing as ever – The Economist

- US house prices never go down. I mean, they don’t, right? – FT

- Dissecting Housing Supply And Demand: Macro Man Podcast. Bloomberg’s Cameron Crise compares the current state of the housing market with the 2006 bubble peak and its aftermath. – Bloomberg

On China

- China cuts mortgage lending rate by record as lockdowns hit economy. Five-year loan prime rate slashed by most since before pandemic as government steps up stimulus – FT

- China’s property market woes expected to worsen in 2022, Reuters poll shows – Reuters

- China property market slumps on developers’ debt crisis, weak buyer sentiment – Reuters

- China’s Real Estate Slump: Underlying Issues. Although the current approach will ease some major indicators, such as property sales and prices, they will not necessarily resolve the core issues. – The Diplomat

On other countries:

- [Australia] Housing in the Endemic Phase – Reserve Bank of Australia

- [Australia] Australia’s housing boom to deflate as mortgage rates rise – Reuters

- [Canada] One of the World’s Frothiest Housing Markets Turned Into a Seller’s Headache Overnight. House hunters from Toronto to small Ontario suburbs are changing how they navigate the tight housing landscape with interest rates heading higher. – Bloomberg

- [Canada] How much will Canada’s block on foreign buyers help its housing crisis? – NPR

- [Hong Kong] New Hong Kong Leader’s Vow to Fix Housing Crisis Draws Skeptics. John Lee will focus on national security in wake of protests. Lack of policy, business experience could also hamper ability – Bloomberg

- [New Zealand] New Zealand banks predict 20% drop in house prices over next year. Economists say tighter credit conditions, higher mortgage rates and increased housing supply behind sinking prices – The Guardian

- [United Kingdom] Nationwide warns inflation surge will hit house prices. Profits double at UK’s largest building society on back of mortgage growth and higher interest margins – FT

- [United Kingdom] Slowdown ahead for UK housing market. Gap between equity-rich house owners and first-time buyers set to widen as cost of living crisis hits – FT

- [United Kingdom] Bridging loans surge as UK buyers scramble for property. Brokers urge caution in volatile market – FT

On cross-country:

- Drivers of rising house prices and the risk of reversal – European Central Bank

- ECB warns a house price correction is looming as interest rates rise. Central bank says housing market reversal would hit low-income homes harder – FT

- Euro zone’s overpriced housing market may sag if rates rise, ECB says – Reuters

- Has COVID-19 Triggered an Urban Exodus?

Posted by at 5:00 AM

Labels: Global Housing Watch

Wednesday, May 25, 2022

Housing Market in Europe

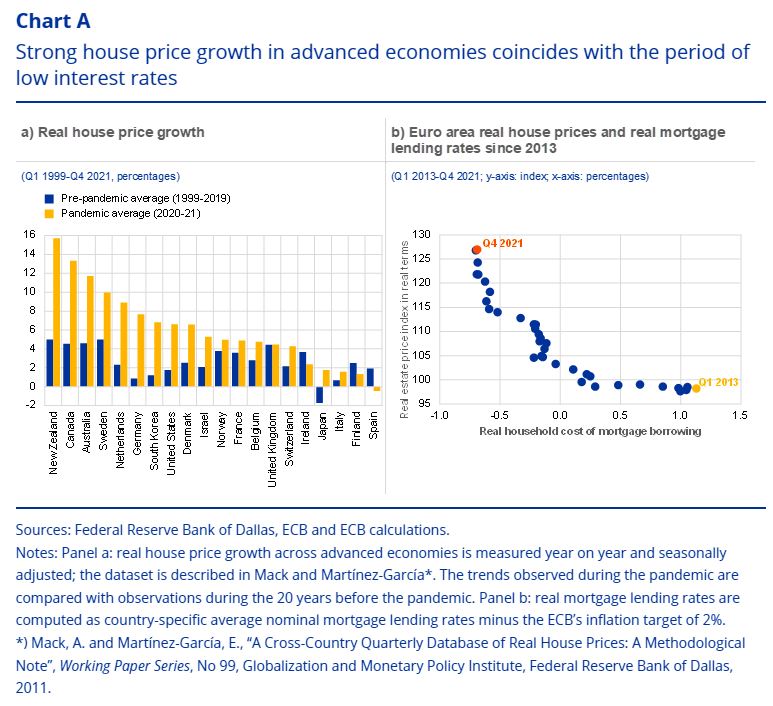

From the European Central Bank:

“House prices increased substantially during the pandemic, fuelling concerns about possible price reversals and their implications for financial stability. In many advanced economies, real house price growth exceeded 4% during the pandemic (Chart A, panel a), reaching 4.3% in the euro area in the fourth quarter of 2021[1] amid signs of exuberance in some countries.[2] At the same time, real mortgage lending rates in the euro area have fallen further to reach historic lows in the current low interest rate environment (Chart A, panel b).[3] Against this backdrop, this box discusses the main drivers of recent house price increases across advanced economies and in the euro area, and the associated risks of possible price reversals and the potential implications for financial stability.

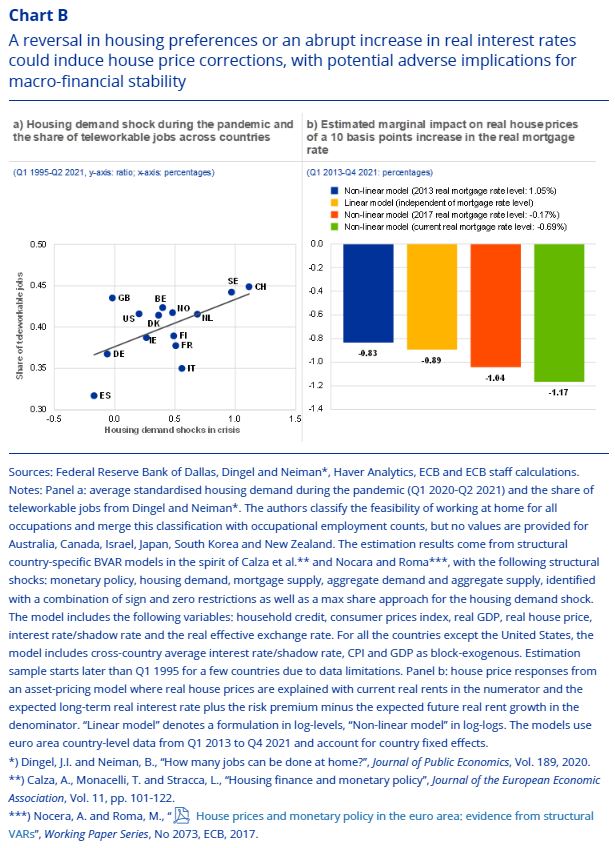

Shifts in housing preferences and low interest rates have been important drivers of recent strong house price growth across advanced economies. Estimates based on country-specific Bayesian vector autoregression (BVAR) models indicate that the house price increases across advanced economies during 2020-21 were mainly driven by increased demand for housing. There is a positive correlation between the magnitude of the estimated housing demand shock across countries and the share of teleworkable jobs, signalling that the housing demand shocks are related to a shift in housing preferences during the pandemic (Chart B, panel a), possibly reflecting a desire for more space coupled with less need for commuting.[4] Increased demand for housing could also be related to search-for-yield behaviour in the low-yield environment. In addition, monetary policy shocks combined with mortgage supply shocks contributed to the recent house price increases across advanced economies, including the euro area. Unlike housing demand shocks, monetary policy and mortgage supply shocks move interest rates and house prices in opposite directions.

In the current low interest rate environment, increased sensitivity of house price growth to changes in real interest rates makes substantial house price reversals more likely. Evidence for the euro area shows that a model with an interest rate-dependent sensitivity of real house prices to real interest rates outperforms a model with a constant sensitivity. Such a non-linear model is consistent with asset pricing theory and implies that the lower the level of the real interest rate, the larger should be the response of house prices for a given change in that rate.[5] Given the current low level of interest rates, therefore, potential reversals in residential real estate prices could be larger than several years ago, especially if interest rates increased sharply. In particular, the comparison between estimated linear and non-linear models (Chart B, panel b) for the euro area shows that the estimated house price response to a 0.1 percentage point increase in real mortgage rates from the current very low level is around 28 basis points stronger when accounting for non-linear relationships (Chart B, panel b).[6]

An abrupt repricing in the housing market – if the demand for housing were to go into reverse, for example, or real interest rates were to rise significantly – could produce spillovers to the wider financial system and economy. Such price reversals in housing markets could reflect a return to pre-pandemic work modalities or a strong increase in real interest rates. Other possible factors include a change in investor preferences for holding residential real estate assets, as well as a more general deterioration in risk sentiment related to an exacerbation of geopolitical risks or progressing climate change. The BVAR models described above indicate that a 1% drop in house prices due to a shift in housing demand could, on average across countries, generate a peak drop in real GDP of 0.2% after two years. However, the decline varies from country to country, with a fall of up to 0.9% in some advanced economies and wide uncertainty bands around these estimates. To cushion adverse financial stability implications of potential house price reversals, a tightening of macroprudential measures seems warranted in some countries, especially where strong house price growth has been accompanied by buoyant credit dynamics.[7]“

From the European Central Bank:

“House prices increased substantially during the pandemic, fuelling concerns about possible price reversals and their implications for financial stability. In many advanced economies, real house price growth exceeded 4% during the pandemic (Chart A, panel a), reaching 4.3% in the euro area in the fourth quarter of 2021[1] amid signs of exuberance in some countries.[2] At the same time,

Posted by at 11:00 AM

Labels: Global Housing Watch

Subscribe to: Posts