Showing posts with label Global Housing Watch. Show all posts

Sunday, July 31, 2022

The Upside-Down Housing Market

From Joseph Politano (Apricitas Economics):

“America has an acute shortage of housing. Its largest and most prosperous cities impede, restrict, or forbid large amounts of construction, and since the Great Recession output of suburban single-family homes has remained depressed. Real rents increased at the fastest pace in history during the late 2010s, housing vacancy rates remain near historic lows, and record numbers of young Americans live with their parents due to housing unaffordability.

For the better part of the that last decade, home prices in America have been on a slow march upwards as higher wages and employment levels mixed with structural under-construction. The pandemic sent the housing market into overdrive—work from home supercharged demand for residential living spaces, changing migration patterns upended local housing markets, lower mortgage rates pushed up prices, and supply-chain issues impeded construction projects.

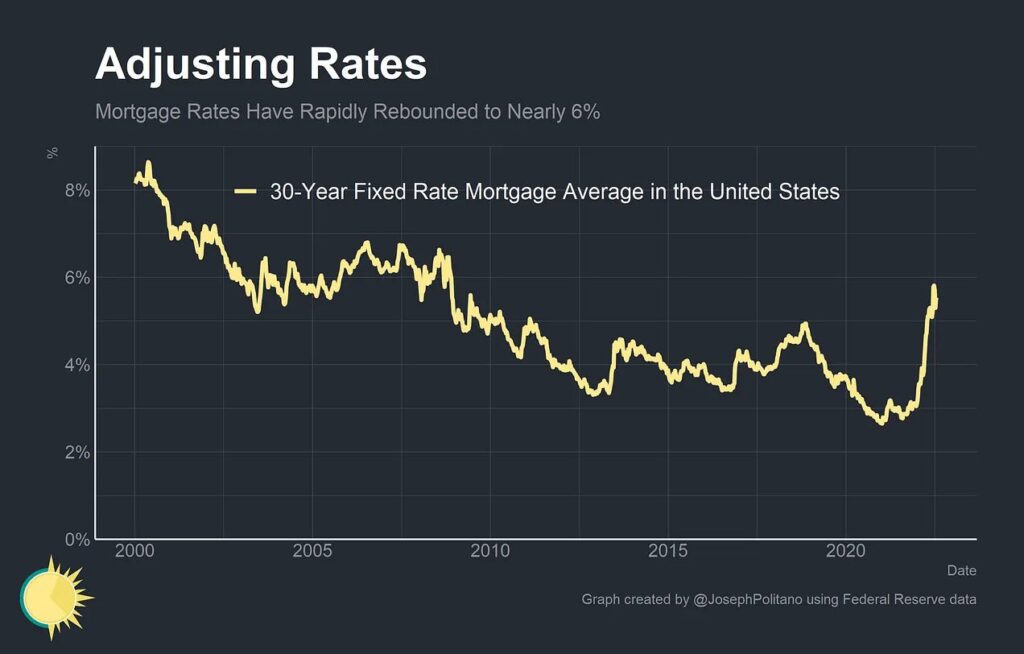

Now, the focus of the Federal Reserve is on constraining credit in order to combat inflation. That’s manifested in higher interest rates across the curve, including higher mortgage rates. In fact, mortgage rates are now higher than at any point since 2010, though they have pulled back a bit from their recent jump to almost 6%. Those higher mortgage rates are turning the housing market upside down—dropping mortgage applications, pulling down homebuilder sentiment, weighing on prices, and crushing housing starts. This mixture of higher rates, strong employment and wage growth, and supply deficiencies is unprecedented in the American housing market.

Mortgage Market Mayhem

Critically, the movements in mortgage rates are unique in modern American history for both their size and speed. After hitting an all time low of 2.6% in early 2021, the average 30-year fixed mortgage rate surged to 5.8% by January 2022 before sliding back to their current levels. Still, the last time mortgage rates were this high was late 2008.”

Continue reading here.

From Joseph Politano (Apricitas Economics):

“America has an acute shortage of housing. Its largest and most prosperous cities impede, restrict, or forbid large amounts of construction, and since the Great Recession output of suburban single-family homes has remained depressed. Real rents increased at the fastest pace in history during the late 2010s, housing vacancy rates remain near historic lows, and record numbers of young Americans live with their parents due to housing unaffordability.

Posted by at 7:27 AM

Labels: Global Housing Watch

Friday, July 29, 2022

Housing View – July 29, 2022

On cross-country:

- How high property prices can damage the economy. A fresh strand of research studies the consequences, both in China and the rich world – The Economist

- The Housing Slowdown Could Become a Global Meltdown. Frothy prices in New Zealand, empty buildings in New York and a mortgage revolt in China have the capacity to make things much worse. – Bloomberg

- Neighbourhoods won’t be improved by banning the unemployed – VoxEU

On the US:

- Treasury Announces New Steps to Increase Affordable Housing Supply and Lower Long-Term Housing Costs for American Families – US Treasury

- U.S. Treasury to allow COVID funds for state, local affordable housing loans – Reuters

- We Need to Keep Building Houses, Even if No One Wants to Buy. Right now, builders have too many homes and not enough people to sell them to. In the long term, the United States has the opposite problem: Not enough houses for all the people who want them. – New York Times

- Can We Escape a Crash? The Housing Market Is Saying Yes. Rising mortgage rates crushed affordability and led to softening demand, but much-needed cost relief is allowing builders to sweeten the deal for buyers without destabilizing the broader economy. – Bloomberg

- Is Housing Market Becoming More Balanced? – Bloomberg

- U.S. housing cooldown is recession red flag for markets – Reuters

- Boise’s Housing Market Boomed Early in the Pandemic. Now It Is Cooling Fast. ‘Zoomtowns’ that drew remote workers are now expecting prices to fall as interest rates rise and companies call employees back to the office – Wall Street Journal

- Housing Affordability Crisis Increases Odds of Recession. A prolonged sales slump in the $4 trillion industry would ripple through the economy. – Bloomberg

- U.S. pending home sales tumble in June as mortgage rate soar – Reuters

- How Moderna’s Covid Vaccine Boosted Boston’s Real-Estate Market. The company’s hiring spree and soaring stock led to an uptick in luxury home purchases by employees during the pandemic – Wall Street Journal

- Rising rents mean no shelter for Americans from inflation storm. Double-digit cost boosts for housing are hampering the Fed’s efforts to contain consumer price increases – FT

- Why your house was so expensive. Material-cost inflation, anti-building rules, NIMBY attitudes, and barriers to innovation have created a housing-affordability crisis – The Atlantic

- Low-Cost Cities With Strong Economies Remain Attractive as Housing Market Slows. Remote workers willing to relocate help push small, affordable areas to the top of the latest WSJ/Realtor.com index – Wall Street Journal

- Summer 2022 Wall Street Journal/Realtor.com Emerging Housing Markets Index – Realtor

- This Housing Market Won’t Be Like Last Time. History Still Has Lessons. – Barron’s

- Real House Prices and Price-to-Rent Ratio in May – Calculated Risk

- Why We Need Social Housing. What Medicare for All is for health care, social housing is for shelter. – The American Prospect

On China:

- China’s central bank seeks to mobilise $148bn bailout for real estate projects. Heavily indebted sector to receive new loans to complete unfinished apartments owed to angry homebuyers – FT

- China’s Property Crisis Burns Middle Class Stuck With Huge Loans. Homeowners cut spending, postpone marriage, boycott mortgage. Housing market no longer seen as a sure bet as economy slows – Bloomberg

- Fresh woe for China’s property sector: mortgage boycotts. Homebuyers’ protests could push risk on to banks – The Economist

- Xi Wields Carrots and Sticks to Quash China Mortgage Boycotts. There are now at least 319 mortgage boycotts across nation. Granting concessions could encourage copycats, analysts say – Bloomberg

- Could China Be Headed for a Lehman-Style Crisis? This Property Bust Is Different. – Barron’s

- See the Full Rankings for WSJ/Realtor.com’s Summer Emerging Housing Markets Index. How metro areas across America stack up in the newly updated summer 2022 rankings – Wall Street Journal

On other countries:

- [Canada] ‘Historic’ Correction Grips Canada’s Housing Market, RBC Says. Bank expects housing prices to decrease 12% from previous peak. Home sales are also expected to fall 42% from early 2021 – Bloomberg

- [Canada] Nowhere to live: Rents in Canada surge as home prices fall – Reuters

- [Canada] Canada’s Housing Investors Are Heading For the Exits as Rates Rise. Home prices in the once-hot market could slide even further as investors choose to sell. – Bloomberg

- [Indonesia] Indonesia’s housing market remains sluggish – Global Property Guide

- [Switzerland] Switzerland’s housing market gradually cooling – Global Property Guide

- [United Kingdom] Housebuilders criticise plans to boost supply in polluted areas of England. More action is needed to tackle ‘very real issue of polluted rivers’, town planners warn – FT

- [United Kingdom] UK Says House Prices Are More Unaffordable Than Ever for Buyers. London housing cost 40 times income for lowest paid families. Property in the North East of England was most affordable – Bloomberg

- [United Kingdom] UK’s Biggest Mortgage Lender Expects Housing Market to Slow. Lloyds thinks house prices will start to decline next year. British borrowing costs to rise along with interest rates – Bloomberg

On cross-country:

- How high property prices can damage the economy. A fresh strand of research studies the consequences, both in China and the rich world – The Economist

- The Housing Slowdown Could Become a Global Meltdown. Frothy prices in New Zealand, empty buildings in New York and a mortgage revolt in China have the capacity to make things much worse. – Bloomberg

- Neighbourhoods won’t be improved by banning the unemployed – VoxEU

On the US:

- Treasury Announces New Steps to Increase Affordable Housing Supply and Lower Long-Term Housing Costs for American Families – US Treasury

- U.S.

Posted by at 5:00 AM

Labels: Global Housing Watch

Friday, July 22, 2022

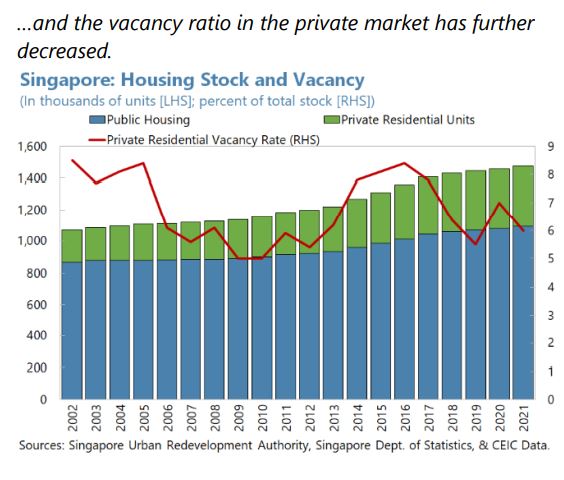

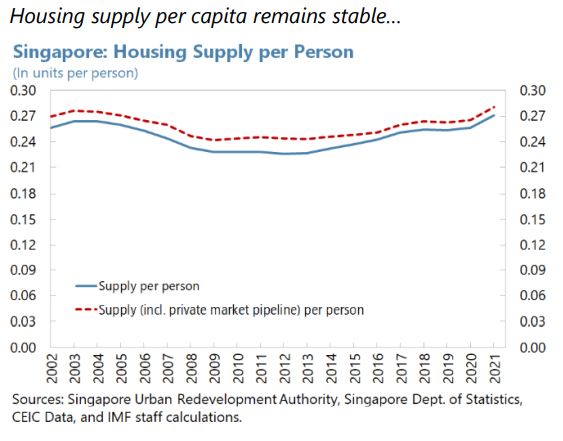

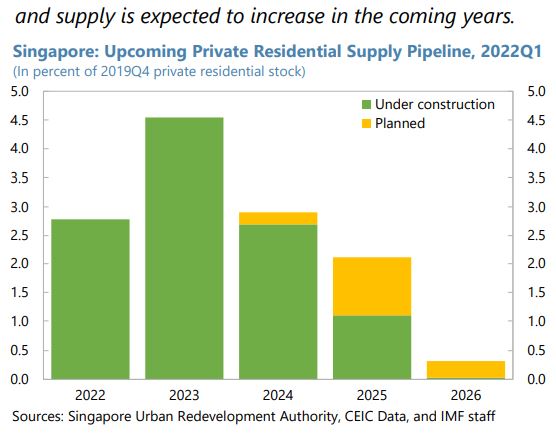

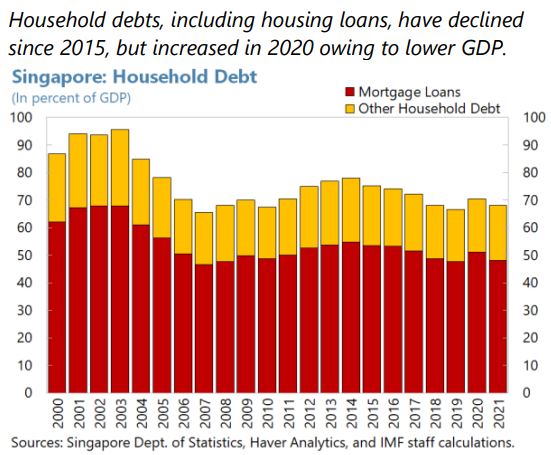

Housing Market in Singapore

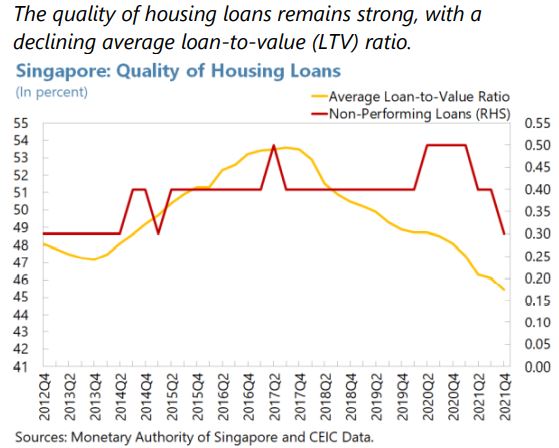

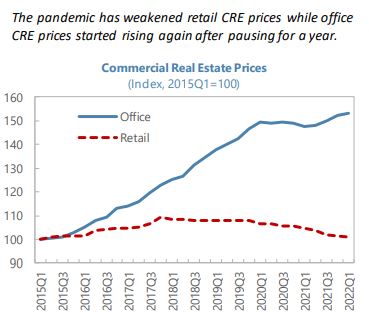

From the IMF’s latest report on Singapore:

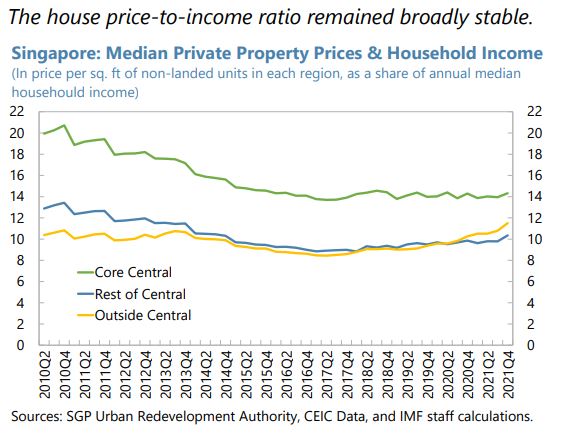

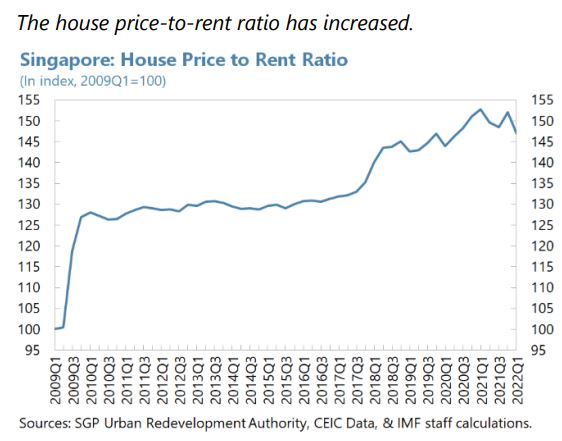

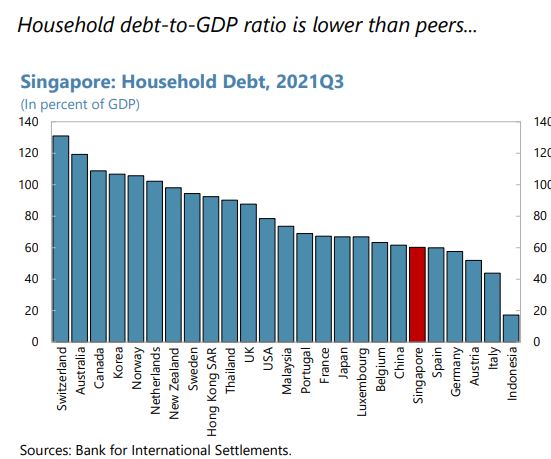

“Driven by strong demand, the private residential housing market runs the risk of diverging further from fundamentals, while commercial real estate is recovering following a few slow years due to the pandemic. House price inflation exceeding pre-COVID trends reflects strong dwelling demand driven by a shift to working from home, changes in domestic household formation with more single home households, increase in foreign demand, low real lending rates and constrained supply exacerbated by the pandemic. Some moderation in price growth occurred during the first quarter of 2022 (…). At close to 90 percent, Singapore already has one of the highest home ownership rates, implying that housing demand is principally being driven by non-residents and resident search for yield activity. Staff analysis suggests that private residential house prices are currently above long-term fundamentals. 13,14 Following a sharp decline in prices in 2020, commercial real estate showed signs of recovery in 2021, with prime office rents rising. However, prices in this segment remain below their pre-pandemic levels.

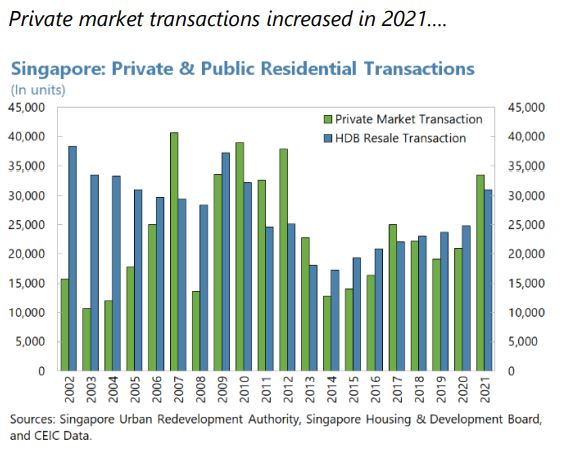

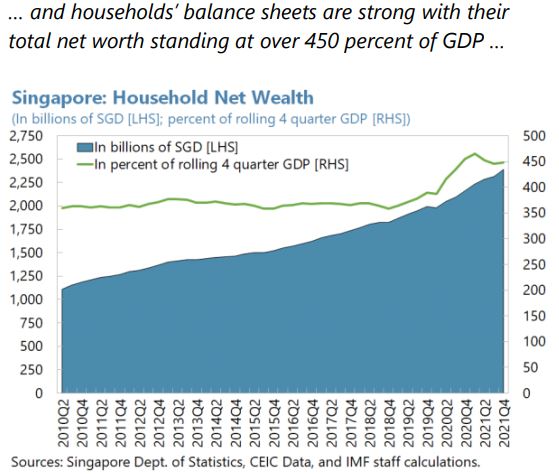

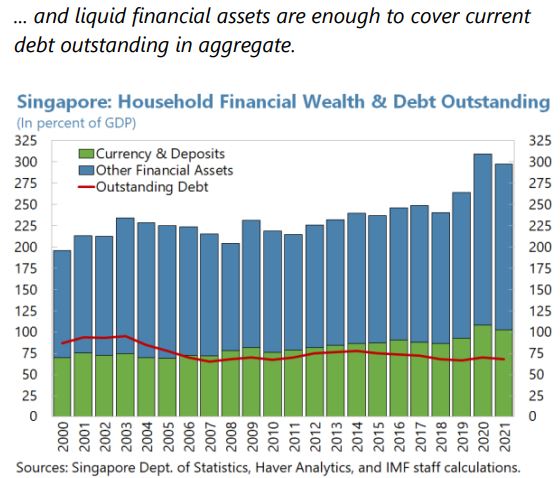

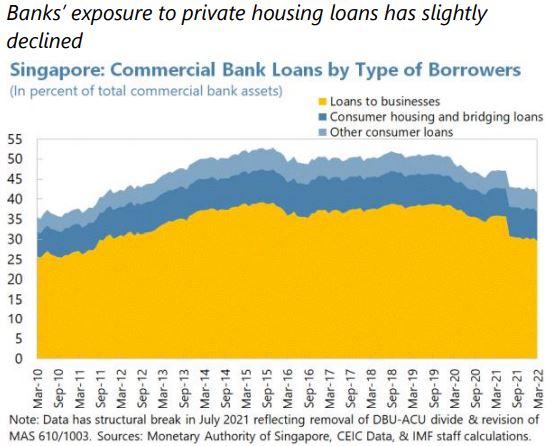

The authorities recently tightened macroprudential measures to cool buoyancy in private and public residential real estate markets, complemented by supply-side measures. Systemic risk is elevated but centered mostly in private residential real estate markets, with key macro-financial transmission channels operating through: (i) an elevated level of household debt, which peaked at 71 percent of GDP during the pandemic, about three quarters of which is secured against real estate; (ii) a high share of mortgages with fixed rates for 3 years or less before transitioning to floating rates; (iii) strong foreign demand sustaining private residential valuations; and (iv) property market related loans representing a third of banks’ total loans by end-2021. Stable average LTV and DS ratios, normally based on conservative interest rate assumptions, are mitigating factors. Recent measures to moderate residential property prices included (i) raising the Additional Buyer’s Stamp Duty (ABSD) rates (text table), (ii) tightening the total debt servicing ratio (TDSR) from 60 to 55 percent, and (iii) tightening the loan to value (LTV) limit for loans from HDB from 90 to 85 percent to encourage greater financial prudence. Based on MAS’ estimates, the resident credit-to-GDP gap was 10.6 percent in Q1 2021 but has since moderated to 0 percent. The authorities have also issued advisories urging prudence in new loan origination, particularly for property purchases. These and other measures complement plans to raise the supply of public and private housing with the Housing and Development Board targeting to raise public flat supply by 35 percent in 2022 and 2023.”

From the IMF’s latest report on Singapore:

“Driven by strong demand, the private residential housing market runs the risk of diverging further from fundamentals, while commercial real estate is recovering following a few slow years due to the pandemic. House price inflation exceeding pre-COVID trends reflects strong dwelling demand driven by a shift to working from home, changes in domestic household formation with more single home households, increase in foreign demand,

Posted by at 8:14 AM

Labels: Global Housing Watch

Housing View – July 22, 2022

On cross-country:

- World’s Frothiest Housing Market Cools in Global Warning Signal. New Zealand’s home sales and prices are tumbling, providing a glimpse of what may unfold elsewhere. – Bloomberg

- Higher interest rates to test buoyant housing markets. Markets where property prices surged during the pandemic are now among the most exposed to a crash – FT

- Housing Boom Fades World-Wide as Interest Rates Climb. Prices are falling in some places, raising the risk of market routs and adding to central banks’ challenges – Wall Street Journal

- Economy Week Ahead: Housing Market and Central Bank Policy in Focus. Expected economic news includes decisions by the European Central Bank and the Bank of Japan – Wall Street Journal

- How to overcome challenges the housing world is facing now – Washington Post

On the US:

- Housing Starts in US Decline to Lowest Level Since September. Groundbreaking dropped 2% to 1.56 million pace in June. Single-family construction, permits fell to two-year lows – Bloomberg

- U.S. Home Sales Fell Again in June, Economists Estimate. The housing market and construction have cooled as higher interest rates start to bite – Wall Street Journal

- Home Building Slipped in June for Second Straight Month. Housing starts fall 2% as buyer demand softens under weight of higher interest rates – Wall Street Journal

- The Housing Market Is Correcting—So Why Are Home Prices Still Soaring? – Realtor

- Housing’s Contribution to Economic Development – Reframing the Narrative – USC Lusk Center for Real Estate With – The Way Forward Housing Coalition

- Housing Demand and Remote Work – San Francisco Fed

- Foreign Buyers Return to US Housing Market After Three-Year Drought. After three straight years of declining sales, buyers from other countries purchased $59 billion worth of US homes – Bloomberg

- Single-Family Starts Fall to Two-Year Low on Higher Construction Costs and Interest Rates – NAHB

- Slowdown in Single-Family Permits in May 2022 – NAHB

- Dynastic Home Equity – San Francisco Fed

- Federal Housing Policies Make It Easier to Get a Loan but Not Be a Homeowner – Cato Institute

- Remodeling Gains to Slide Lower Through Mid-Year 2023 – Harvard Joint Center for Housing Studies

- Dreams adrift: pandemic relocations deepen Hawaii’s housing crisis. As key workers abandon hopes of home ownership and desert the archipelago, its economy and laid-back lifestyle are under threat – FT

- The Housing Shortage Isn’t Just a Coastal Crisis Anymore. An increasingly national problem has consequences for the quality of American family life, the economy and the future of housing politics. – New York Times

- Home Prices Grew at Near-Record High in Second Quarter. FNM-HPI Measured Home Price Growth at Annualized Rate of 19.4 Percent in Q2 2022 – Fannie Mae

On China

- Chinese city Zhengzhou sets up bailout fund as mortgage boycott spreads. The homebuyer revolt over stalled projects is aggravating a property sector crisis – FT

- People Are Refusing to Pay Their Mortgages in China. The Protest Could Spill Into the Wider Economy – Time

- China’s Mortgage Boycott Capital Plans Property Bailout Fund. Henan’s capital Zhengzhou faces the most mortgage protests. The bailout fund will help stressed projects in Zhengzhou – Bloomberg

- China’s mortgage boycott spurs shakeout among strapped developers – Reuters

- China property: refusing to pay mortgages is a powerful political weapon. Unrest could mark a bad start to president Xi Jinping’s third term – FT

- China banks told to bail out property developers as mortgage boycotts threaten economy. Intervention comes as thousands of homebuyers refuse to make mortgage repayments in deepening property sector crisis – The Guardian

- China Seeks to Quell Mortgage Revolt Among Frustrated Home Buyers. Analysts estimate home buyers could walk away from as much as $150 billion to $370 billion in home loans – Wall Street Journal

- China Weighs Mortgage Grace Period to Appease Angry Homebuyers. Officials consider temporary waivers after payment boycott. Property crisis has fueled concerns about social stability – Bloomberg

- China urges banks to extend loans for real estate projects amid mortgage boycott – Reuters

- Chinese regulators rush to tame investor panic over mortgage boycotts. Homebuyers stop paying loans on more than 200 unfinished property projects – FT

- More Chinese Homebuyers Refuse to Pay Mortgage Loans Amid Contagion Fears. Bank stocks fell on concern property crisis is spreading. Projects facing mortgage snubs more than tripled since Monday – Bloomberg

- China Convenes Banks on Mortgage Boycott Roiling Markets. Officials asked for information on impact of housing loan snub. More buyers refuse to pay loans on unfinished home projects – Bloomberg

- Homebuyers in Multiple Cities Go on Mortgage Strike Over Delayed Projects – Caixin Global

- Is China stumbling into its own mortgage crisis? – Washington Post

- China Home Prices Fall for 10th Month as Crisis Deepens. Market facing new stress with homebuyer mortgage boycott. Government relief efforts have yet to revive property sector – Bloomberg

On other countries:

- [Canada] Canada Home Prices Slide Most Since at Least 2005 on Rates. Price decline accelerates to 1.9% in June; Toronto suburbs hit. Bank of Canada has increased borrowing costs aggressively – Bloomberg

- [Canada] Canadian home prices continue to plunge in June as higher rates pinch – Reuters

- [Canada] Homeowner Politics and Housing Supply – University of British Columbia

- [Canada] The housing market trend no one’s talking about is improving affordability for young buyers – The Globe and Mail

- [Canada] Toronto Offers Glimpse of Housing Pain as Renovations Slow Down. As rates rise, homeowners are cutting back on improvements. Housing market, with renos, made up 8.5% of GDP in pandemic – Bloomberg

- [Egypt] Egypt’s erratic house price movements – Global Property Guide

- [Mexico] Mexico’s housing market cooling – Global Property Guide

- [Romania] Sharp turnaround for Romania’s housing market – Global Property Guide

- [Singapore] Singapore Home Sales Fall to Lowest Since May 2020 on Costs. Purchases fell to 488 new units in June, versus 1,355 in May. Central banks are hiking up interest rate to curb inflation – Bloomberg

- [Singapore] Singapore Central Bank Sees Stable Residential Property Market – Bloomberg

- [United Kingdom] The Bank of England’s bizarre mortgage decision. With interest rates rising, now is not the time to scrap the test of affordability for home loans – FT

- [United Kingdom] UK house prices rising, despite slowing demand – Global Property Guide

- [Vietnam] Vietnam’s housing market gaining momentum – Global Property Guide

On cross-country:

- World’s Frothiest Housing Market Cools in Global Warning Signal. New Zealand’s home sales and prices are tumbling, providing a glimpse of what may unfold elsewhere. – Bloomberg

- Higher interest rates to test buoyant housing markets. Markets where property prices surged during the pandemic are now among the most exposed to a crash – FT

- Housing Boom Fades World-Wide as Interest Rates Climb.

Posted by at 7:59 AM

Labels: Global Housing Watch

Wednesday, July 20, 2022

Housing Market in Germany

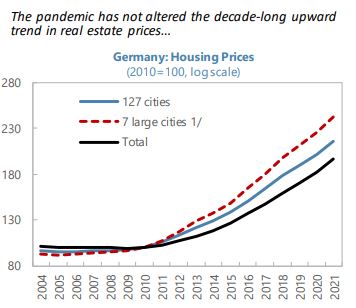

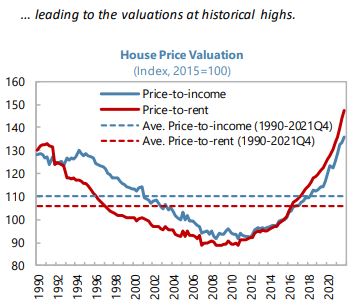

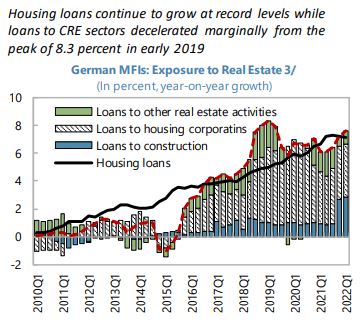

From the IMF’s latest report on Germany:

“The authorities have appropriately tightened macroprudential policy in the face of house price risks, but further actions are needed. Rapid rises in housing prices (12.4 percent between 2021Q4 and 2020Q4) have led to residential real estate valuations above fundamental levels for Germany overall, and even greater misalignment in larger cities. Nationwide, price-to-rent and price-to-income indicators suggested deviations from the long-run average of about 37 and 21 percent, respectively at end-2021, while estimates of an econometric model suggest overvaluations of 10–15 percent at 2021Q3. Meanwhile, a city-level panel model suggests greater overvaluation in the largest cities. Mortgage origination has also been strong and lending standards appear somewhat loose in certain segments. For example, according to different private sector data sources, between 7 and 20 percent of mortgage loans exceed the underlying property value (e.g., Text Figure 11). With these vulnerabilities in mind, the authorities appropriately raised the counter-cyclical capital buffer to 0.75 percent, from zero previously, and introduced a sectoral systemic risk buffer of two percent on loans secured by domestic residential real estate to apply from February 1, 2023. The authorities have also cautioned banks against taking excessive risks in mortgage lending. However, legal concerns and a lack of comprehensive data on lending standards remain obstacles to the activation of borrower-based measures, like the imposition of limits on loan-to-value ratios on new lending. As noted in the FSAP, precautionary use of borrower-based measures is warranted, and the authorities should remove obstacles to their activation by modifying the law on borrower-based measures, while in the interim strengthening guidance on lending standards (for example, encouraging banks to adhere to loan-to-value ratio limits through issuing a Guidance Note to banks). The authorities are also urged to accelerate the closure of data gaps and add income-based measures into the macroprudential toolkit.

Authorities’ Views

While generally sharing staff’s assessment of financial sector health and recommendations, the authorities assessed that risks in the housing market do not warrant the activation of borrower-based measures at this juncture. The authorities appreciated the FSAP’s stress tests of bank solvency and liquidity and found the results to be in line with their expectations. They are aware of U.S. dollar liquidity risks at some LSIs but judge that these are already sufficiently managed in the supervisory process. They emphasized the risk-sharing that takes place between savings and cooperative banks and their regional wholesale bank partners. The authorities highlighted the appropriateness of the macroprudential policy package announced by BaFin in January 2022. They noted that important data gaps on lending standards will be closed in 2023 and legislative proposals are being drafted to add income-based instruments to the toolkit. Furthermore, the Bundesbank has set up a project dedicated to monitoring the effects of the macroprudential policy package—inter alia its effects on lending standards. Existing private sector data on LTV and DSTI ratios currently provide mixed signals. On financial safety nets, the authorities considered that maintaining the existing multiple deposit guarantee schemes appropriately reflects the three-pillar structure of the German banking system.

From the IMF’s latest report on Germany:

“The authorities have appropriately tightened macroprudential policy in the face of house price risks, but further actions are needed. Rapid rises in housing prices (12.4 percent between 2021Q4 and 2020Q4) have led to residential real estate valuations above fundamental levels for Germany overall, and even greater misalignment in larger cities. Nationwide, price-to-rent and price-to-income indicators suggested deviations from the long-run average of about 37 and 21 percent,

Posted by at 1:16 PM

Labels: Global Housing Watch

Subscribe to: Posts