Showing posts with label Global Housing Watch. Show all posts

Friday, August 5, 2022

Housing View – August 5, 2022

Conferences

On cross-country:

- Eurozone mortgage rate rises threaten house price growth. Borrowing expected to become more expensive in coming months as European Central Bank increases rates – FT

- The global housing boom is running out of steam. Where are prices going to fall most sharply? – The Economist

- Housing Boom and Headline Inflation: Insights from Machine Learning – IMF

- Era of soaring house prices is ending as central banks raise rates. Policies are tightening when major economies are either falling into recession or heading that way – The Guardian

- Will Increasing Housing Supply Reduce Urban Inequality? – International Regional Science Review

- Adapting to flood risk: Evidence from global cities – VoxEU

On the US:

- The Understated ‘Housing Shortage’ in the United States – Institute of Labor Economics

- The Upside-Down Housing Market. What Happens After Mortgage Rates Hit A 13-Year High? – Apricitas Economics

- Home Sellers Cut Prices as Housing Market Cools. How higher mortgage rates—and frustration—are changing the playbook for sellers – Wall Street Journal

- Why Rising Mortgage Rates Don’t Mean Falling Home Prices – Barron’s

- Should DC’s Empty Office Buildings Get Turned Into Apartments? It’s clear workers will never return in full force. Developers and local officials see an opportunity. – Washingtonian

- A College Town Takes On Exclusionary Zoning. Gainesville, Florida, could be on the verge of eliminating single-family housing requirements. – Bloomberg

- Median vs Repeat Sales Index House Prices – Calculated Risk

- What Is the Future of Public Housing in America’s Cities? – AEI

- Apartment Rents Begin Tapering Off After Record Growth. Rents are still rising at a historically fast pace but market shows signs of softening – Wall Street Journal

- What’s Ahead for the Housing Market – Goldman Sachs

- Buyers’ Expectations of Housing Availability Improve – NAHB

- A Town’s Housing Crisis Exposes a ‘House of Cards’. In the Idaho resort area of Sun Valley, there are so few housing options that many workers are resorting to garages, campers and tents. – New York Times

- Private Residential Spending Declines in June – NAHB

- The Mix of Home Buyers Is Changing, Leading to Improved Affordability – NAHB

- The Cross-Section of Housing Returns – Cleveland Fed

- New housing market data reveals a stunning shift as these 21 of the top 50 metro areas show price declines for June – AEI

- Banks Report Unchanged Home Lending Standards – NAHB

On China:

- ‘Financial monsters’: China’s bad banks complicate property crisis. Distressed asset management companies highlight the challenge Beijing faces in mobilising rescue options – FT

- Sweeping Mortgage Boycott Changes the Face of Dissent in China. Angry homebuyers have launched one of the most effective protests the country has ever seen. – Bloomberg

- China Home Sales Plunge in July, as Mortgage Revolt Deters Buyers. Sales fell on the year and from the previous month, ending a budding recovery – Wall Street Journal

- China’s Home Sales Slump Further During Mortgage Boycotts. Top 100 developers saw sales tumble almost 40% in July. Industry confidence remains at a low level, CRIC says – Bloomberg

- China Banks May Face $350 Billion in Losses From Property Crisis. Mortgage boycotts and slowing growth are rattling authorities. Pressure seen growing on China’s $56 trillion banking system – Bloomberg

- How China can overcome its property crisis – OMFIF

- Chinese banks can withstand mortgage boycott if property prices hold – S&P Global

On other countries:

- [Australia] From boom to gloom, Australia’s red hot property market hits reverse – Reuters

- [Australia] Will the house price collapse be different this time? A puzzling feature of the latest house price slump is that prices for top-end properties, which are usually most vulnerable to housing market corrections, are showing surprising resilience. – Financial Review

- [Austria] Austria Real Estate Market Analysis 2022 – Global Property Guide

- [Hong Kong] ‘Historic’ Hong Kong home prices: worst yet to come, with up to 30 per cent slump a possibility as market enters decline. – South China Morning Post

- [Hong Kong] Will sharp rises in interest rates diminish Hong Kong’s love affair with property? – South China Morning Post

- [New Zealand] New Zealand House Prices Sink Most Since Global Financial Crisis. CoreLogic data show biggest three-month decline since 2008. Buyer demand curbed by soaring mortgage interest rates – Bloomberg

- [Poland] Poland’s mortgage holiday for households threatens bank profits. Lenders warn moratorium will hit earnings and could result in legal action against government – FT

- [South Korea] S. Korea’s home prices to fall up to 2.8% with 100 bp rate hike – c.bank report – Reuters

- [United Kingdom] UK’s Mortgage Market Feels the Heat From Rising Rates. NatWest reports slower mortgage growth in second quarter. Lloyds predicts house prices will finally fall in coming year – Bloomberg

- [United Kingdom] The Guardian view on housing costs: a grave and growing injustice. Levelling up will be impossible as long as rents and house prices are allowed to keep on climbing – The Guardian

- [United Kingdom] Interest rates are rising – so why are mortgage rules being scrapped? Analysis: Bank ruling that borrowers don’t have to show they can afford steep repayment hikes raises questions over how to curb excessive borrowing – The Guardian

- [United Kingdom] Who took out mortgage payment holidays during the pandemic? – Bank of England

- [United Kingdom] UK house prices rise at 11% annual rate despite cost of living crisis. Strong labour market and limited housing stock push up prices as mortgage transactions cool – FT

Conferences

On cross-country:

- Eurozone mortgage rate rises threaten house price growth. Borrowing expected to become more expensive in coming months as European Central Bank increases rates – FT

- The global housing boom is running out of steam. Where are prices going to fall most sharply?

Posted by at 8:02 AM

Labels: Global Housing Watch

Thursday, August 4, 2022

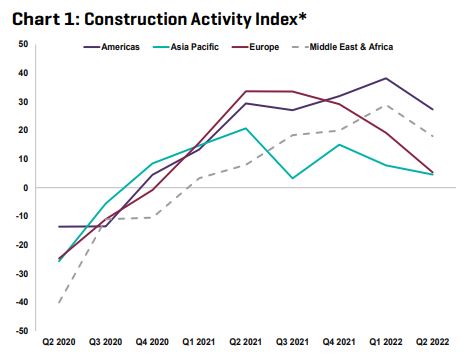

Macro headwinds increasingly weighing on the outlook for construction in parts of the world

From RICS:

” – Construction Activity Index stalls in Europe and APAC, but remains a little more resilient elsewhere

– Overwhelming majority of respondents still report material costs and shortages to be impediments

– Global workloads still anticipated to rise across all sectors, albeit expectations are being scaled back”

From RICS:

” – Construction Activity Index stalls in Europe and APAC, but remains a little more resilient elsewhere

– Overwhelming majority of respondents still report material costs and shortages to be impediments

– Global workloads still anticipated to rise across all sectors, albeit expectations are being scaled back”

Posted by at 8:13 AM

Labels: Global Housing Watch

Monday, August 1, 2022

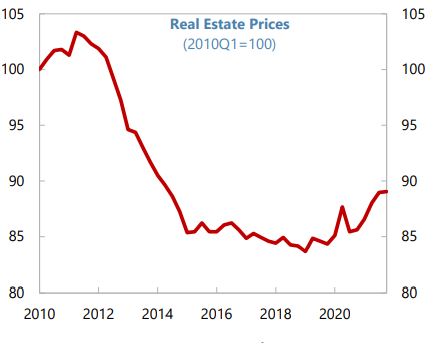

House Prices in Italy

Posted by at 8:34 AM

Labels: Global Housing Watch

Housing Boom and Headline Inflation: Insights from Machine Learning

From a new IMF working paper by Yang Liu, Di Yang, and Yunhui Zhao:

“Inflation has been rising during the pandemic against supply chain disruptions and a multi-year boom in global owner-occupied house prices. We present some stylized facts pointing to house prices as a leading indicator of headline inflation in the U.S. and eight other major economies with fast-rising house prices. We then apply machine learning methods to forecast inflation in two housing components (rent and owner-occupied housing cost) of the headline inflation and draw tentative inferences about inflationary impact. Our results suggest that for most of these countries, the housing components could have a relatively large and sustained contribution to headline inflation, as inflation is just starting to reflect the higher house prices. Methodologically, for the vast majority of countries we analyze, machine-learning models outperform the VAR model, suggesting some potential value for incorporating such models into inflation forecasting.”

From a new IMF working paper by Yang Liu, Di Yang, and Yunhui Zhao:

“Inflation has been rising during the pandemic against supply chain disruptions and a multi-year boom in global owner-occupied house prices. We present some stylized facts pointing to house prices as a leading indicator of headline inflation in the U.S. and eight other major economies with fast-rising house prices. We then apply machine learning methods to forecast inflation in two housing components (rent and owner-occupied housing cost) of the headline inflation and draw tentative inferences about inflationary impact.

Posted by at 8:18 AM

Labels: Global Housing Watch

Adapting to flood risk: Evidence from global cities

From a VoxEU post by Sahil Gandhi, Matthew Kahn, Rajat Kochhar, Somik Lall, and Vaidehi Tandel:

“Climate change is increasing the frequency and intensity of disasters, but the ability to cope varies widely across the globe. This column examines how city death tolls and economic activity are affected by flooding. Richer places with the resources and infrastructure to cope with disasters tend to be more resilient. Compared to cities in low-income countries, those in high-income countries suffered fewer deaths per disaster, adapted over the years to better mitigate the effects of flooding, and recovered faster from economic damage.

The major floods in India and Australia in 2022 have once again drawn attention to the destructive capacity of disasters. Climate change is likely to increase the frequency and intensity of these shocks. At the same time, the ability to cope with disasters will vary widely across places and over time. The living conditions of households in India are very different from those in Australia. In India, a large proportion of urban households live in slums on hillslopes or other unsafe areas. The impact of similar disasters would be different for the two countries. Given that a majority of people around the world now live in cities, it is important to measure the vulnerability and adaptive capacity of such productive areas to disasters.

Cities in developing countries suffer more

Research on the impact of extreme weather predicts that the developing world, especially the poor and vulnerable populations, will be disproportionately affected (Mendelsohn et al. 2000, Mendelsohn et al. 2006, Tol 2009).

In our new paper (Gandhi et al. 2022), we use data on floods for 9,468 cities in 175 countries to examine the differential impact of floods on cities in high- and low-income countries. We combine monthly night light (VIIRS) data for these cities from 2012 to 2018 with a global dataset of geocoded disasters. Figure 1 shows that after a flood event, night lights fall and then recover. Floods disrupt life in cities through temporary power failures, disruption of essential services, damage to property, and temporary closure of offices and factories. These are reflected in the lights seen at night (Kocornik-Mina et al. 2016).”

Continue reading here.

From a VoxEU post by Sahil Gandhi, Matthew Kahn, Rajat Kochhar, Somik Lall, and Vaidehi Tandel:

“Climate change is increasing the frequency and intensity of disasters, but the ability to cope varies widely across the globe. This column examines how city death tolls and economic activity are affected by flooding. Richer places with the resources and infrastructure to cope with disasters tend to be more resilient. Compared to cities in low-income countries,

Posted by at 8:14 AM

Labels: Global Housing Watch

Subscribe to: Posts