Showing posts with label Global Housing Watch. Show all posts

Tuesday, December 20, 2011

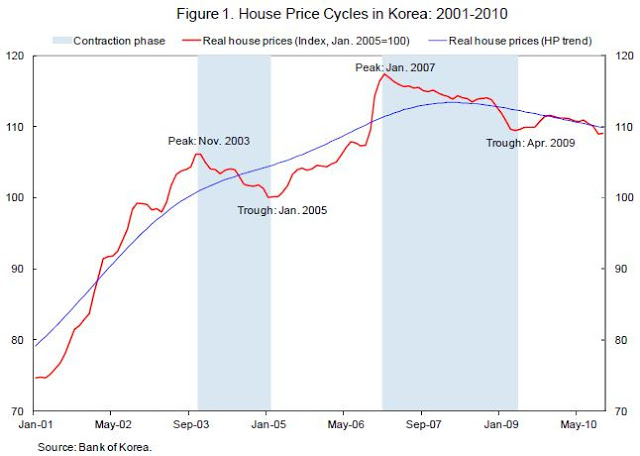

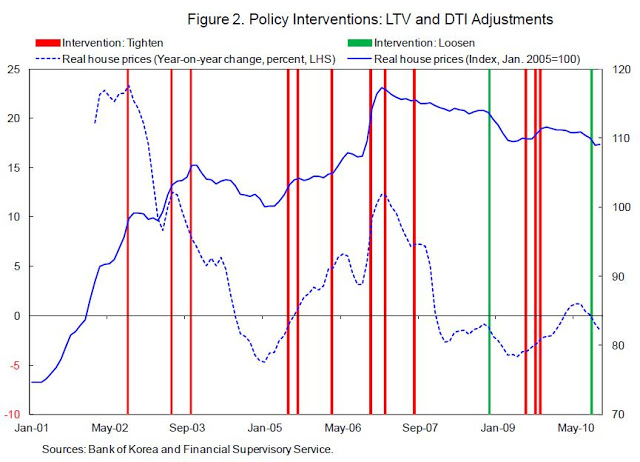

Housing Market in Korea

An interesting paper by my IMF colleagues Deniz Igan and Heedon Kang looks at how limits on loan-to-value ratios and debt-to-income ratios affect the housing market in Korea.

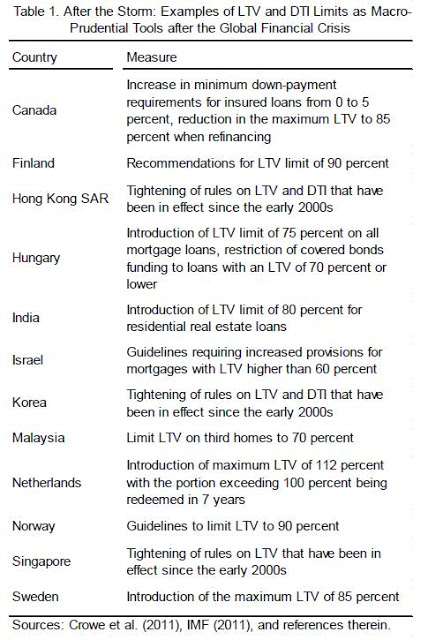

“Prior to the crisis, when it came to dealing with asset price booms, the widely-accepted tenet was one of ‘benign neglect’, namely, to wait for the bust and pick up the pieces (Bernanke and Gertler, 2001). Yet, the crisis and its formidable costs shifted the balance to the opposite camp favoring pre-emptive policy actions that could stop bubbles or, at least, could contain the damage to the financial sector and the broader economy when the bust comes. In other words, many policymakers now think that it is better to act than wait on the sidelines because the cost of inaction may greatly exceed the potential negative side effects of policy intervention. (…) In the quest to better design the policy toolkit to deal with real estate booms and busts, macroprudential tools such as maximum limits on loan-to-value ratios (LTV) and debt-to-income ratios (DTI) are heavily advocated. This has led several countries to recently adopt such limits or measures that would discourage high-LTV/DTI loans.”

Korea is one of a dozen countries that have adopted such limits.

“we know little about the impact of these measures that have become popular with many regulators after the crisis. Theoretically, limits on LTV and DTI can kill two birds with one stone: they can curb the feedback loop between mortgage credit availability and house price appreciation, and, by restraining household leverage, they can help reduce the incidence and loss given default of residential mortgage loan delinquencies.”

The paper asks two questions

“First, what happens when LTV/DTI limits are adjusted in response to developments perceived to be risky? Second, can we quantify the impact of LTV and DTI limits on housing and mortgage activity?”

What are their conclusions? Igan and Kang find that

“transaction activity drops significantly in the three-month period following the tightening of LTV/DTI regulations. Price appreciation slows down a bit later, in a six-month window rather than the three-month window. Moreover, price dynamics appear to be reined in more after LTV tightening rather than DTI tightening. [The authors provide evidence for what the] channel for the impact of the policy actions may be: expected house price increases in the future become lower after policy intervention and this is more prevalent among older households while plans to purchase of a home are more likely to be postponed by those who already own a property, i.e., potential speculators, but not by those who do not own a property, i.e., potential first-time home buyers. These findings suggest that tighter limits on loan eligibility criteria, especially on LTV, curb expectations and speculative incentives. Policy implications of our analysis are encouraging. In housing markets, expectations are key as they often facilitate the settling in of bubble dynamics. If, as suggested by the evidence presented here, limits on LTV curb expectations and discourage potential speculators, they can be effective tools to tame real estate booms and contain the associated risks.”

An interesting paper by my IMF colleagues Deniz Igan and Heedon Kang looks at how limits on loan-to-value ratios and debt-to-income ratios affect the housing market in Korea.

Igan and Kang write

“Prior to the crisis, when it came to dealing with asset price booms, the widely-accepted tenet was one of ‘benign neglect’, namely, to wait for the bust and pick up the pieces (Bernanke and Gertler, 2001).

Posted by at 10:08 PM

Labels: Global Housing Watch

Monday, December 12, 2011

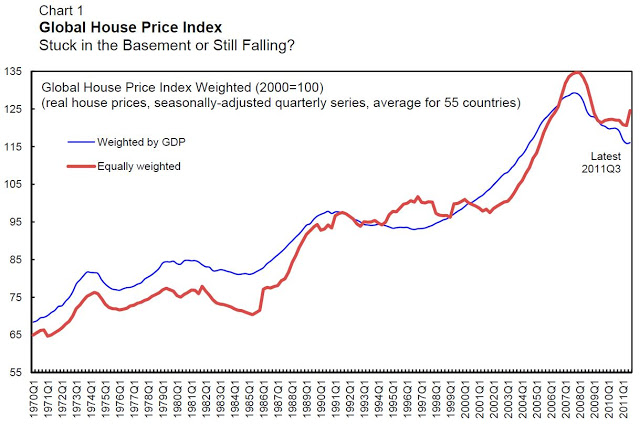

GLOBAL HOUSE PRICE MONITOR

Do house prices have more room to fall?

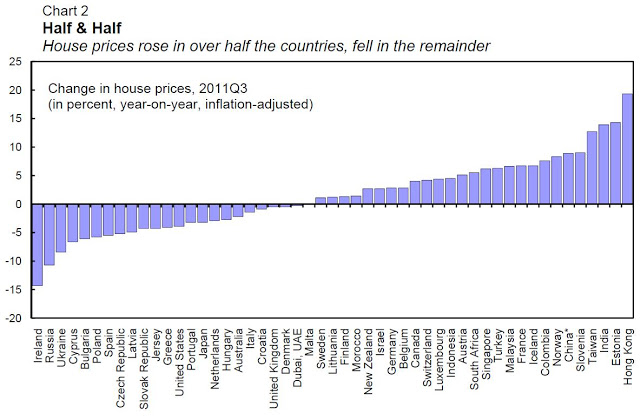

Globally, house prices remain in the doldrums, according to just-released data for 2011:Q3. After a decade of boom, the global house price index peaked in 2007:Q4 and since then has been falling or at best stuck in the basement.

Looking behind the global index, however, reveals the inequality across countries. It’s not quite the 99% vs. the 1%, but more like 50-50: house prices have fallen over the past year in about half the countries and risen in the other half.

More Room to Fall?

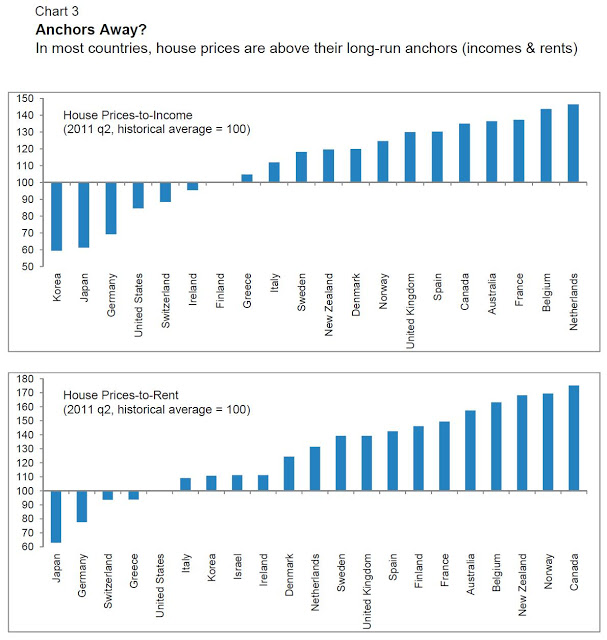

Many factors drive house prices (see: Housing Prices: More Room to Fall? and IMF Research Bulletin article: Seven questions about house price cycles) making it difficult to predict their future course. Two indicators that economists use to predict the direction of change in house prices are the ratio of house prices to income and the ratio of house prices to rents. If these two ratios are above their historical averages, economic theory suggests that declines in house prices may still be in the offing.

How do these indicators look with the latest data on house prices? For all but a handful of countries, these ratios remain above, and in many cases well above, their historical averages, signaling that there may be room to fall.

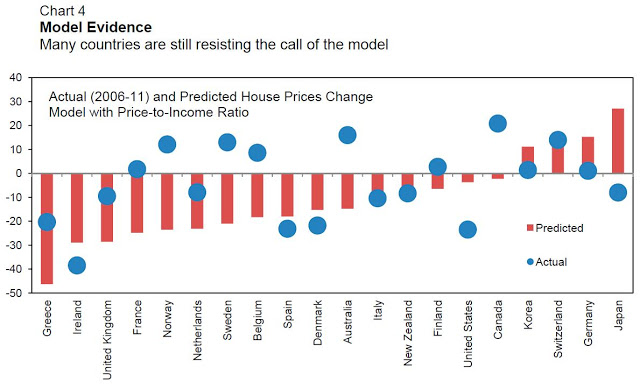

An econometric model of the determinants of house prices, used in the World Economic Outlook (see: House Prices: Corrections and Consequences, and updated here and here ), paints a somewhat different picture. The model explains house price growth based on several short-run momentum factors, such as growth in incomes, asset prices and population, and long-run factors, such as the house price to income ratio. The difference between house prices and those predicted on the basis on these ‘fundamental’ factors gives an indication of whether there is room to fall. The results from this exercise show that in many countries the declines in house prices over the past five years (the ‘actual’) are close to, or even exceed, what was predicted by the model. But for many countries, house prices are still resisting the predictions of the model.

‘This Country is Different’

The indicators presented above are very broad brush. At any time, there are myriad country-specific factors that influence house prices. IMF staff reports for countries often delve into these factors in much detail. Readers interested in developments in house prices in particular countries would be well served by consulting these documents. Links to some recent reports that have featured house price developments are given below.

|

Country

|

Link to report

|

Pages

|

Date

|

|

Australia

|

8

|

Oct-11

|

|

|

Canada

|

30, 36

|

Dec-10

|

|

|

Canada

|

3 to 16

|

Dec-10

|

|

|

China

|

9 to 10

|

Jul-11

|

|

|

Denmark

|

3, 9

|

Dec-10

|

|

|

France

|

24 to 26, 30

|

Jul-11

|

|

|

Korea

|

7, 25

|

Aug-11

|

|

|

Netherlands

|

1, 18, 27

|

Jun-11

|

|

|

Netherlands

|

47 to 55

|

Jun-11

|

|

|

Spain

|

9

|

Jul-11

|

|

|

Sweden

|

9 to 10

|

Jul-11

|

|

|

Switzerland

|

8

|

May-11

|

|

|

United Kingdom

|

8, 10, 30

|

Aug-11

|

|

|

United States

|

19 to 22, 47

|

Jul-11

|

|

|

United States

|

4 to 13

|

Jul-11

|

Also, see two powerpoint presentations on A look at housing prices around the world and Policy Options to Deal With Real Estate Booms.

Do house prices have more room to fall?

Globally, house prices remain in the doldrums, according to just-released data for 2011:Q3. After a decade of boom, the global house price index peaked in 2007:Q4 and since then has been falling or at best stuck in the basement.

Looking behind the global index, however, reveals the inequality across countries. It’s not quite the 99% vs.

Posted by at 4:41 PM

Labels: Global Housing Watch

Sunday, December 12, 2010

China: Property Bubble in the Making?

Ashvin Ahuja, an economist with the IMF, has made a study of property prices in China. Follow the link to compare China’s housing market with others around the globe.

Ashvin Ahuja, an economist with the IMF, has made a study of property prices in China. Follow the link to compare China’s housing market with others around the globe.

Hong Kong

Posted by at 4:06 AM

Labels: Global Housing Watch

Friday, October 15, 2010

Bouncing Between Floors? Globally, House Prices are Up and Down

Real estate markets have been a source of strength during past economic recoveries, but this time is different. Read the story and see the presentation.

Posted by at 2:38 PM

Labels: Global Housing Watch

Wednesday, October 6, 2010

More Room to Fall? Prospects for Housing Markets

The IMF just released its world economic outlook, including this update on the generally dismal prospects for real estate markets across the globe.

Real estate markets have been a source of strength during past recoveries, but this time is different. In many major economies around the globe, house prices continue to fall or are only gradually stabilizing. In a few countries, including the United States, there are concerns of a “double dip” in the housing market. Read the full article…

Posted by at 5:30 PM

Labels: Global Housing Watch

Subscribe to: Posts