Showing posts with label Global Housing Watch. Show all posts

Friday, February 10, 2012

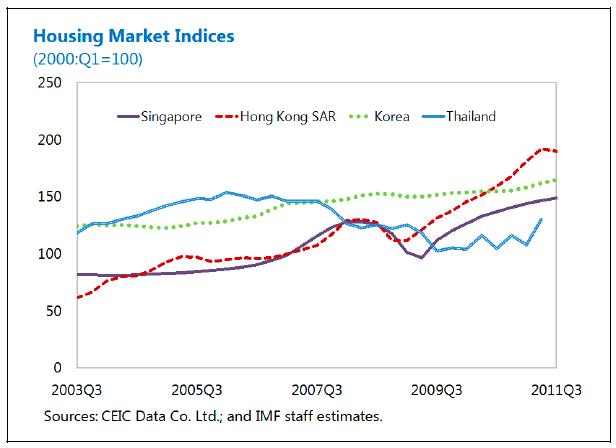

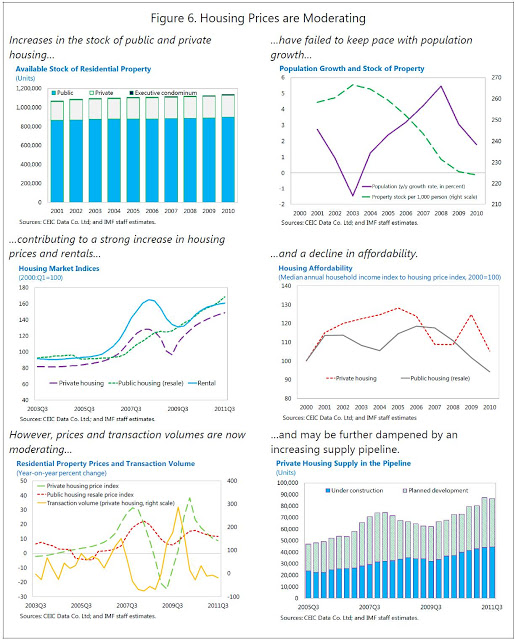

House Prices in Singapore

“Following a steep decline in 2008−09, private residential property prices rebounded strongly and are now above the previous peak. Public housing resale prices, which were more resilient during the crisis, are also growing rapidly, and this has allowed many owners to sell and upgrade into private housing, contributing to price pressures in that market. House prices have outpaced median household incomes, leading to a decline in home affordability, which has become a prominent social issue.

Property prices have been propelled by:

- A resurgent economy, which has buoyed incomes.

- Low interest rates. Real mortgage rates have been very low or negative for the past two years, leading to high housing credit growth rates.

- Supply constraints. Housing supply has not kept pace with population growth, which has been driven up by strong immigration.

- Demand by nonresidents. A booming economy and prospects of currency appreciation, along with Singapore’s strong investment climate, have lured foreign interest in the housing market.

Between September 2009 and January 2011, the authorities adopted four rounds of measures to contain demand, including the introduction (and subsequent tightening) of seller stamp duties, and lowering of LTV caps on private property loans. In a fifth round in December 2011, they introduced an additional buyer’s stamp duty, aimed at curbing investment demand, particularly from foreigners and corporate. The authorities have also undertaken measures to increase the supply of public and private housing

Staff analysis suggests that the measures undertaken by the authorities through January 2011 have helped contain prices and transaction volumes in the housing market, both of which are now moderating. Along with slower domestic growth, an uncertain outlook, and a significant supply pipeline of public and private housing projects (although residential construction activity is slowing), the housing market was already likely to cool further. The latest measures in December 2011 took markets by surprise and shifted the balance of risks further downward. Because these measures are residency˗based and focus on the housing market, they also carry some risk of pushing foreign demand over to commercial and industrial property markets (which are also experiencing price increases) or to other countries.”

The IMF report notes:

“Following a steep decline in 2008−09, private residential property prices rebounded strongly and are now above the previous peak. Public housing resale prices, which were more resilient during the crisis, are also growing rapidly, and this has allowed many owners to sell and upgrade into private housing, contributing to price pressures in that market. House prices have outpaced median household incomes, leading to a decline in home affordability, which has become a prominent social issue.

Posted by at 10:02 PM

Labels: Global Housing Watch

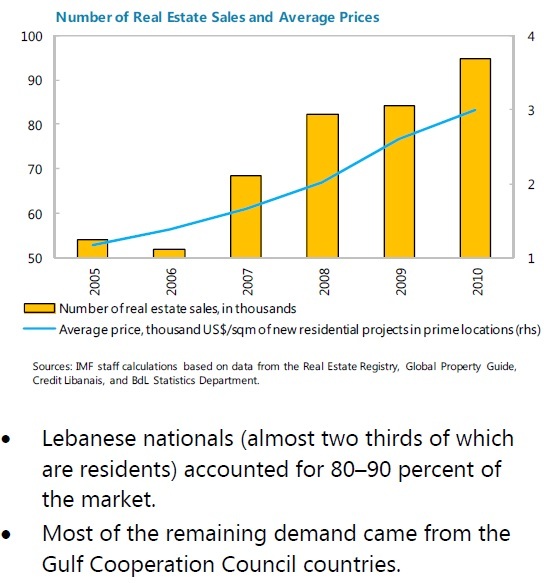

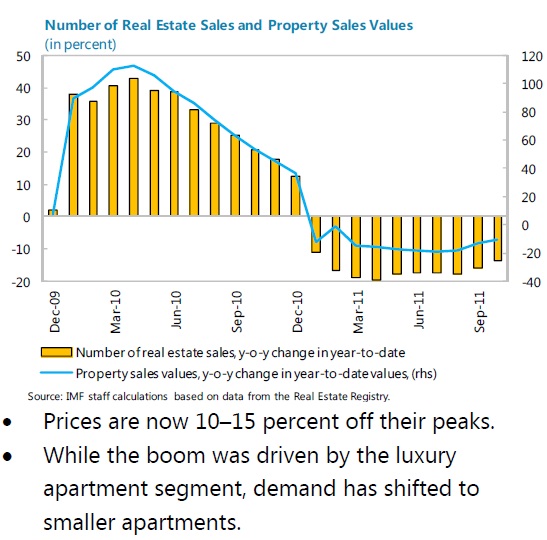

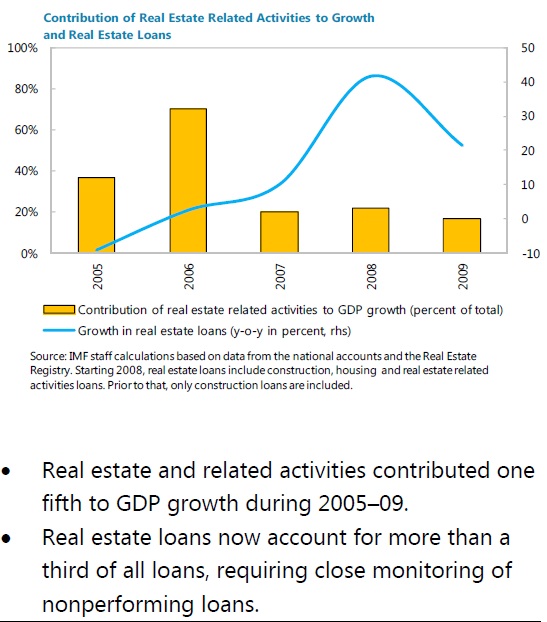

House Prices in Lebanon

The IMF notes: “Real estate boomed during 2006-09, but the market started to correct in mid-2010. The correction is adversely affecting the economy, but could bring prices more in line with the region.”

The IMF notes: “Real estate boomed during 2006-09, but the market started to correct in mid-2010. The correction is adversely affecting the economy, but could bring prices more in line with the region.”

Posted by at 12:19 AM

Labels: Global Housing Watch

Thursday, February 2, 2012

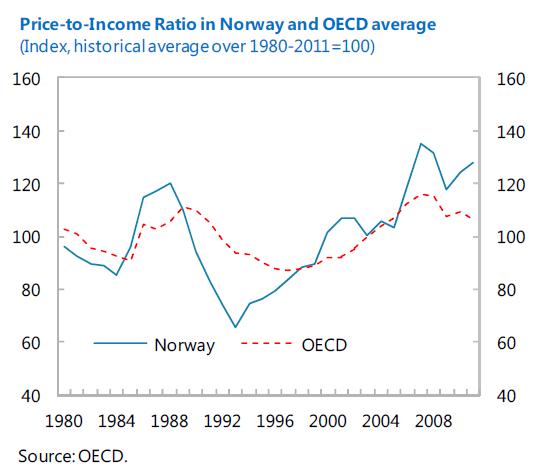

House Prices in Norway

IMF staff report says:

- Over the last two years Norway has seen one of the most rapid paces of real house price appreciation in the OECD.

- Housing valuations continue to appear on the high side. Standard metrics, such as price-to-rent and price-to-income ratios, indicate a risk of overvaluation.

- The ratio of house prices to rents has risen sharply during the boom and is now nearly 70 percent above its historical average—the highest such deviation in any OECD country.

- The house price-to-income ratio has also been rising. This ratio is now 28 percent above its historical average—higher than the peak reached before the last major house price bust in Norway two decades ago.

- While fundamentals explain part of the boom, signs also point to risks of overvaluation. On balance, model based estimates from the IMF’s Early Warning Exercise (EWE), which take into account the key determinants of house prices, suggest that Norwegian residential property prices may be misaligned by 15-20 percent. However, there is admittedly a high amount of uncertainty around this estimate in both directions.

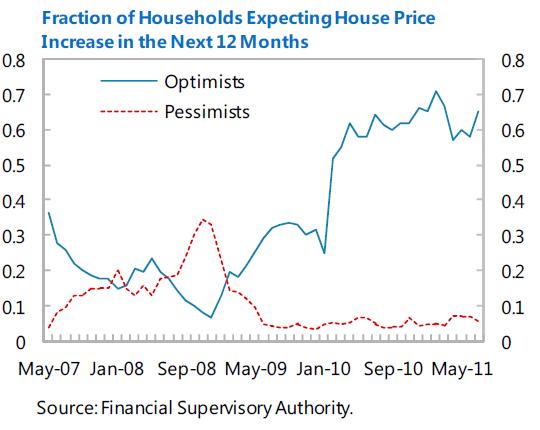

- Expectations of increasing prices may lead agents to buy for speculative motives. An increasing number of households believe that property prices will continue to appreciate. (…) Today, 70 percent of the survey respondents expect price to increase over the next 12 months.

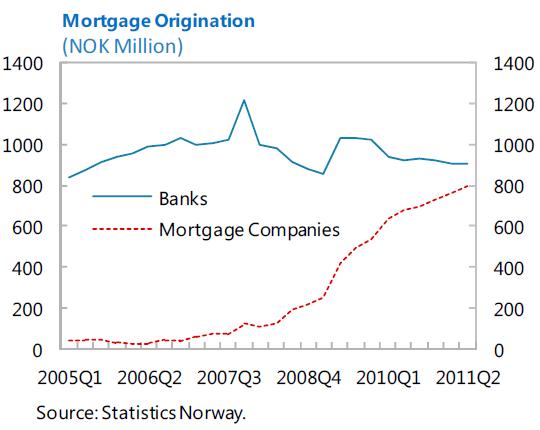

- Another candidate for explaining the boom is loose credit conditions. (…) the share of mortgages with loan-to-value (LTV) ratios over 90 percent has been high since data were first collected in the late 1990s, after the boom was already underway. However, it is somewhat worrisome that the share of mortgages with LTVs over 90 percent has increased since 2010, despite the issuance of FSA guidelines recommending against allowing LTVs to exceed this level, other than in exceptional circumstances.

- About 95 percent of mortgages loans are adjustable-rate and interest payments are front-loaded, low interest rates have made mortgages cheaper and homes significantly more affordable.

- Total household mortgage debt as a fraction of disposable income has increased to 195 percent by end-2010.

- The volume of secured loans issued by mortgage companies has picked up considerably since 2008. In 2011, loans from mortgage companies represented nearly 50 percent of new mortgages.

- Owner-occupied housing receives quite generous tax treatment in Norway.

- A house price bust would likely be associated with depressed economic activity and increased financial sector stress, especially given high levels of mortgage debt.

- The estimates suggest that a 10 per cent drop in real house prices in Norway is associated with roughly 1 percentage point lower GDP growth than otherwise. (…) A correction of 30 percent in house prices—as occurred during the crisis in the 90s—would exert a non-negligible effect to the real economy.

IMF staff report says:

- Over the last two years Norway has seen one of the most rapid paces of real house price appreciation in the OECD.

- Housing valuations continue to appear on the high side. Standard metrics, such as price-to-rent and price-to-income ratios, indicate a risk of overvaluation.

- The ratio of house prices to rents has risen sharply during the boom and is now nearly 70 percent above its historical average—the highest such deviation in any OECD country.

Posted by at 3:36 PM

Labels: Global Housing Watch

Saturday, December 24, 2011

More Housing Woes on the Horizon?

As the United States continues to grapple with the fallout of its housing bubble and blow-up, recent research from the International Monetary Fund uncovers some startling statistics about other countries that could be headed toward their own U.S.-style housing crises.

While home prices have fallen in about half of the countries the IMF tracks, they’ve risen in the other half. Those trends coupled with data used to gauge the affordability of housing and whether homes are valued correctly seems to indicate prices have significant room to fall.

In other words, home values in many countries are inflating much like the run-up the U.S. saw in the early 2000s and could be headed for a correction.

Continue reading here.

Meg Handley of U.S. News writes

As the United States continues to grapple with the fallout of its housing bubble and blow-up, recent research from the International Monetary Fund uncovers some startling statistics about other countries that could be headed toward their own U.S.-style housing crises.

While home prices have fallen in about half of the countries the IMF tracks, they’ve risen in the other half.

Posted by at 12:38 AM

Labels: Global Housing Watch

Thursday, December 22, 2011

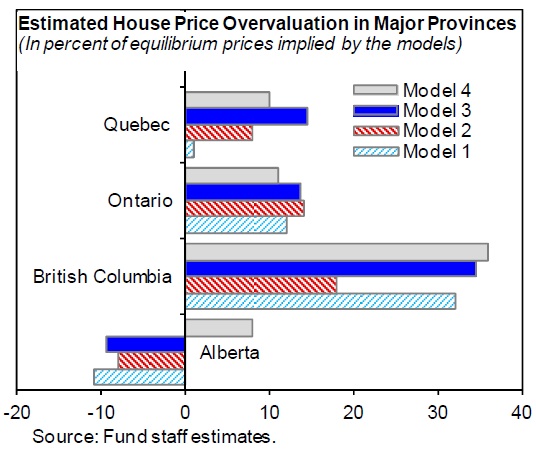

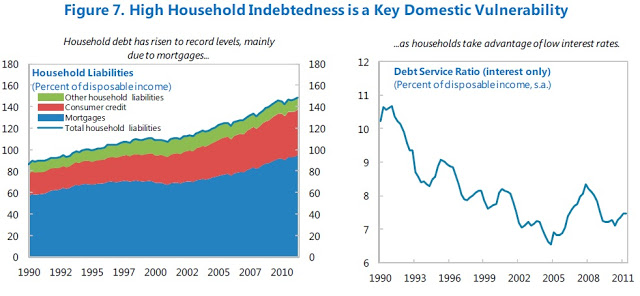

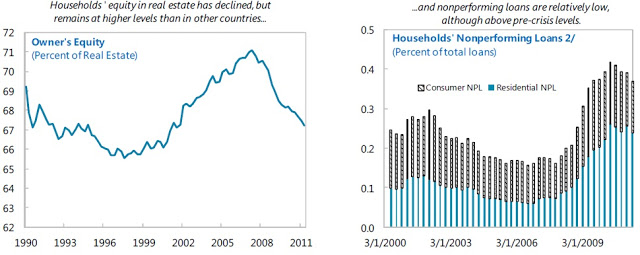

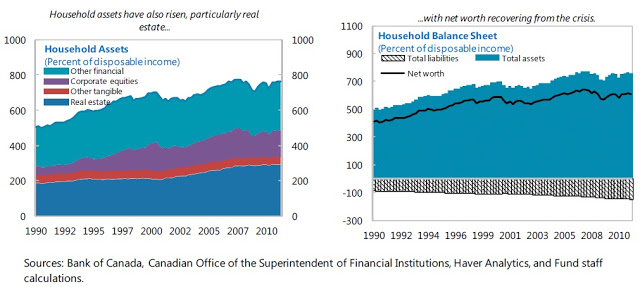

House Prices in Canada

What’s likely to happen to house prices in Canada? Are house prices more out of whack with fundamentals in British Columbia than in Ontario or Alberta? And what would the consequences be for the economy if house prices fell?

The IMF’s economic outlook for Canada has an extensive discussion of prospects for the Canadian housing market. IMF staff noted that “the [house] price-to-rent and [house] price-to-income ratios are 29 percent and 20 percent above their averages for the last decade, respectively”. My earlier post compares Canadian ratios to those in the U.S. and Europe.

IMF staff said that “while there are structural factors that can explain increases in such ratios, their elevated level and other empirical evidence suggest that house prices may be higher than justified by underlying fundamentals, at least in some provinces—staff estimates indicate an average price overvaluation of around 10 percent, with significant regional differences.”

A companion paper estimates “house prices in 2011 to be above the levels consistent with the current levels of fundamentals in British Columbia, with some signs of overvaluation also in Ontario, and to a lesser degree, in Quebec. By contrast, the estimated models suggest house prices to be mildly undervalued in Alberta.” Averaging these estimates (with weights based on provincial GDP levels), the paper suggests “that house prices in Canada are on average ten percent above the level consistent with current fundamentals.”

The companion paper also studied “the impact of a potential correction in house prices on consumption through household wealth effects.” The paper’s authors concluded that the “empirical estimates suggest that a ten percent decline in house prices would lead to a 1¼ percent decline in private consumption.”

The full report can be found here. In it, IMF staff noted that “to ensure the long-term stability of housing markets” the Canadian government has “increased public awareness of the risks and … tightened mortgage insurance standards several times since 2008.”

What’s likely to happen to house prices in Canada? Are house prices more out of whack with fundamentals in British Columbia than in Ontario or Alberta? And what would the consequences be for the economy if house prices fell?

The IMF’s economic outlook for Canada has an extensive discussion of prospects for the Canadian housing market. IMF staff noted that “the [house] price-to-rent and [house] price-to-income ratios are 29 percent and 20 percent above their averages for the last decade,

Posted by at 10:32 PM

Labels: Global Housing Watch

Subscribe to: Posts