Showing posts with label Global Housing Watch. Show all posts

Thursday, August 2, 2012

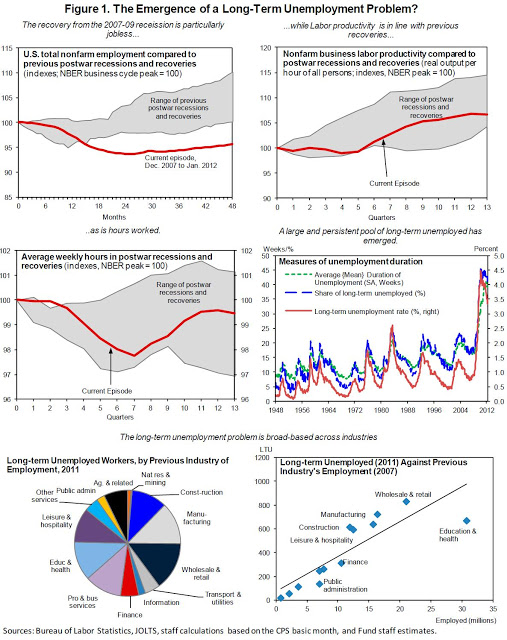

House Prices in the US

The authorities noted that the series of measures taken since last year to support the housing market were starting to bear fruit. These measures include in particular an expansion of the Home Affordable Refinancing Program (HARP) for loans owned or guaranteed by the GSEs, and a strengthening of the Home Affordable Modification Plan (HAMP), including loosened eligibility criteria through the elimination of debt service-to-income cutoffs, and the tripling of incentives for investors to carry out principal reductions under HAMP’s Principal Reduction Alternative (PRA) (Box 5). Recent data suggests that the October 2011expansion of HARP seems to have led to a significant increase in HARP refinancing. The share of loans that have benefited from a principal reduction under the modification program (Home Affordable Modification program of HAMP) has also been on the rise, and early signs show that the tripling of the incentives for principal reductions is receiving interest from investors, and is likely to spur further principal reductions in the future. The recent State Attorneys General Settlement with the major banks, which resolved claims about improper foreclosures and abuses in servicing the loans, could lead in the medium run to a non-trivial reduction in foreclosures, including through up to $34 billion of principal reduction. Early signs indicate that the settlement has led banks to delay foreclosures and also to increasingly substitute them with “short sales” of underwater properties, which are less costly and count toward the banks’ commitment for principal reduction under the settlement. The authorities highlighted that greater reliance on short sales, as opposed to foreclosures, could support the housing market going forward.

The mission welcomed this progress, but also noted that more aggressive policy action may be warranted to accelerate the resolution of the housing crisis. As noted in the Fed’s November 2011 white paper, housing markets do not self-correct efficiently and, absent forceful policies to support the market, prices could fall below their equilibrium levels due to feedback loops from prices to demand and supply. If house prices are anticipated to decline, potential buyers could stay out of the market even if interest rates are low. Moreover, a decline in prices reduces housing equity, triggering further defaults and foreclosures. Foreclosures, in turn, put renewed downward pressure on prices, not only by adding to the supply of houses for sale, but also because they lead to a destruction of value and impose “deadweight” losses on the economy, hurting consumer wealth and credit availability.

The IMF’s 2012 annual report on the US economy says that “house prices have shown some firming recently, with a surprising increase in Q1 2012.” It also highlights that

The authorities noted that the series of measures taken since last year to support the housing market were starting to bear fruit. These measures include in particular an expansion of the Home Affordable Refinancing Program (HARP) for loans owned or guaranteed by the GSEs, and a strengthening of the Home Affordable Modification Plan (HAMP),

Posted by at 3:33 PM

Labels: Global Housing Watch

Tuesday, July 3, 2012

How Vulnerable Is Sweden’s Housing Market?

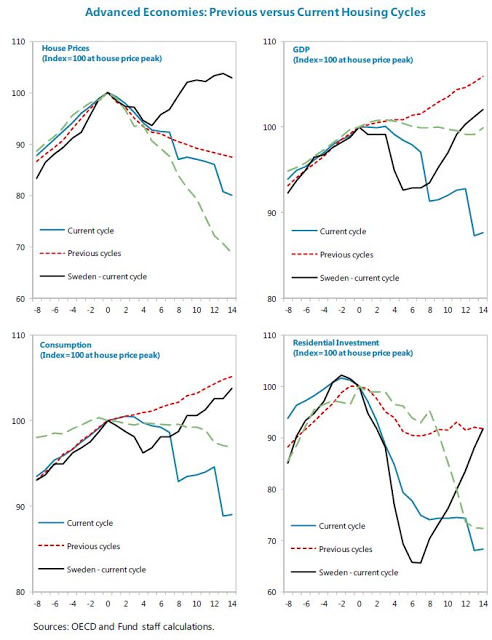

According to the latest IMF’s annual report on Sweden, the residential real estate cycle may have reached its long-predicted peak in Sweden. Housing starts halved over 2011 while the real prices dropped substantially in the second half of 2011 (-3.5 percent cumulatively) and remained flat in 2012 Q1 (q-o-q). The surge in late 2010 and early 2011, following the decline through 2008, appears to have been due to buyers taking advantage of the low interest rate environment and to the abolition of the real estate tax in 2008 in favor of a municipal tax set at the lower of SEK 6,825 (around 969 euros) or 0.75 percent of the property’s assessed value. Indeed, in the two years to 2011 Q2, residential investment (+37 percent) took off again, contrary to more muted developments during the previous recovery, offsetting the sharp drop in new homebuilding experienced during the global crisis.

Going forward, several factors may indicate further downward pressure on house prices. First, price-to-income and price-to-rent ratios remain 1.1 and 1.4 standard deviations respectively above historical averages. Second, staff’s model-based estimates from the Early Warning Exercise (EWE) and Vulnerability Exercise for Advanced Countries (VEA) suggest an overvaluation around 11–12 percent, exceeding the 10 percent threshold. (The EWE real estate model combines these three indicators to create a heat map for house price valuation.) Moreover, the predicted path of house prices based on WEO income projections suggests a decline of almost 5-6 percent through 2017.

These indicators put Sweden among the advanced countries where a house price correction is most likely to take place. Yet, the point estimate for the house price disequilibrium (the difference between actual prices and estimated equilibrium or long-run prices) is not large by historical standards, and Sweden ranks only 9th among 22 advanced economies in the VEA sample in terms of potential overvaluation. Furthermore, other components of residential real estate vulnerability (namely, potential impact on GDP, household balance sheets, and mortgage market characteristics) remain moderate or low in Sweden, compared to other advanced economies. That said, with most mortgages being “rollover” mortgages with terms of at most five years, any future interest rate increases could put additional strains on already highly indebted households.

According to the latest IMF’s annual report on Sweden, the residential real estate cycle may have reached its long-predicted peak in Sweden. Housing starts halved over 2011 while the real prices dropped substantially in the second half of 2011 (-3.5 percent cumulatively) and remained flat in 2012 Q1 (q-o-q). The surge in late 2010 and early 2011, following the decline through 2008, appears to have been due to buyers taking advantage of the low interest rate environment and to the abolition of the real estate tax in 2008 in favor of a municipal tax set at the lower of SEK 6,825 (around 969 euros) or 0.75 percent of the property’s assessed value.

Posted by at 2:24 PM

Labels: Global Housing Watch

Friday, May 18, 2012

House Prices in United Arab Emirates

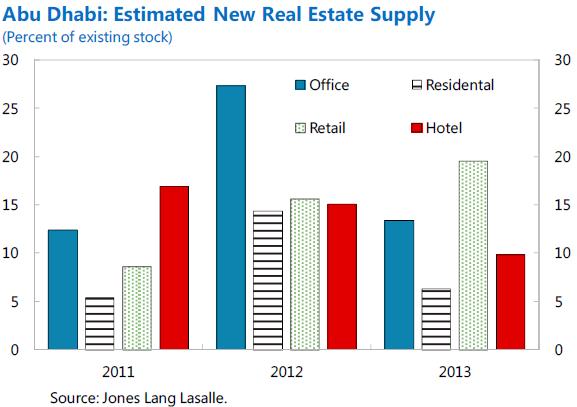

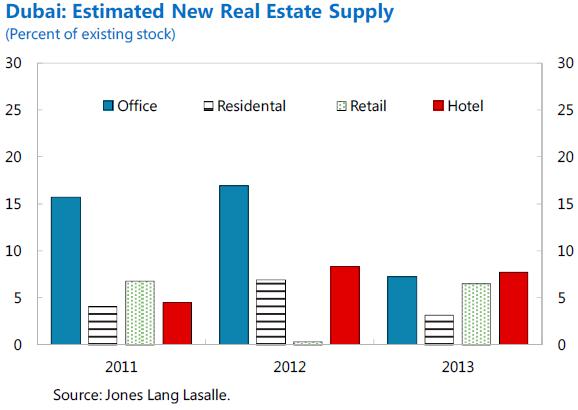

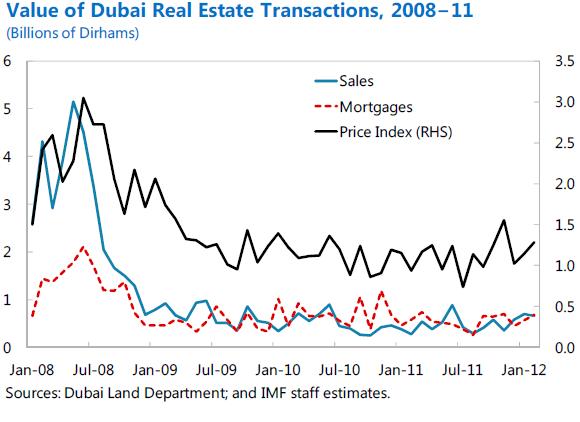

A new IMF report says that “the large property overhang continues to be a drag on the economy. Since mid-2008, real estate prices have fallen by more than 60 percent in Dubai, and to a lesser extent in Abu Dhabi. The large supply overhang and the completion of additional projects in the coming years render an early and broad-based recovery of the sector unlikely.” Read the full report here.

A new IMF report says that “the large property overhang continues to be a drag on the economy. Since mid-2008, real estate prices have fallen by more than 60 percent in Dubai, and to a lesser extent in Abu Dhabi. The large supply overhang and the completion of additional projects in the coming years render an early and broad-based recovery of the sector unlikely.” Read the full report here.

Posted by at 1:37 PM

Labels: Global Housing Watch

Wednesday, March 7, 2012

House Prices in Philippines

Posted by at 9:27 PM

Labels: Global Housing Watch

Friday, March 2, 2012

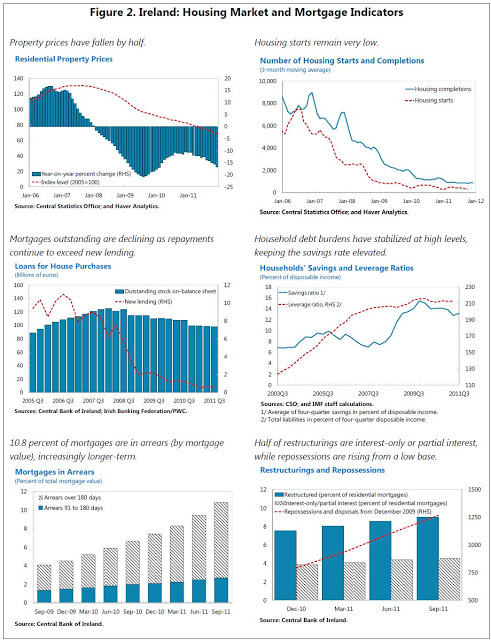

House Prices in Ireland

The IMF report notes:

“House price declines accelerated in the second half of 2011, while mortgage arrears continued to rise (Figure 2). Nonetheless the rate of decline in house prices at 13.2 percent y/y in 2011, remained within the stress scenario for the bank recapitalization, which allowed for a house price decline of 17.4 percent in 2011, and a further fall of 18.8 percent in 2012. With house prices down 47.4 percent from their peak in 2007, indicators of house valuation are returning to historical norms. The value share of owner-occupied residential mortgages in arrears rose to 10.8 percent in Q3 2011. About 10.7 percent of this loan book value has undergone restructuring, mostly reducing payments to interest-only, but about half of the restructured loans are still in arrears.”

The IMF report notes:

“House price declines accelerated in the second half of 2011, while mortgage arrears continued to rise (Figure 2). Nonetheless the rate of decline in house prices at 13.2 percent y/y in 2011, remained within the stress scenario for the bank recapitalization, which allowed for a house price decline of 17.4 percent in 2011, and a further fall of 18.8 percent in 2012. With house prices down 47.4 percent from their peak in 2007,

Posted by at 5:58 PM

Labels: Global Housing Watch

Subscribe to: Posts