Showing posts with label Global Housing Watch. Show all posts

Monday, September 30, 2013

Global House Prices: falling, recovering, or bubbling?

My colleague Hites Ahir, who has worked with me over the years on housing issues, is making this presentation at UDC today. What’s the answer to the question posed in this title? See his presentation below to find out.

My colleague Hites Ahir, who has worked with me over the years on housing issues, is making this presentation at UDC today. What’s the answer to the question posed in this title? See his presentation below to find out.

Posted by at 1:56 PM

Labels: Global Housing Watch

Sunday, September 15, 2013

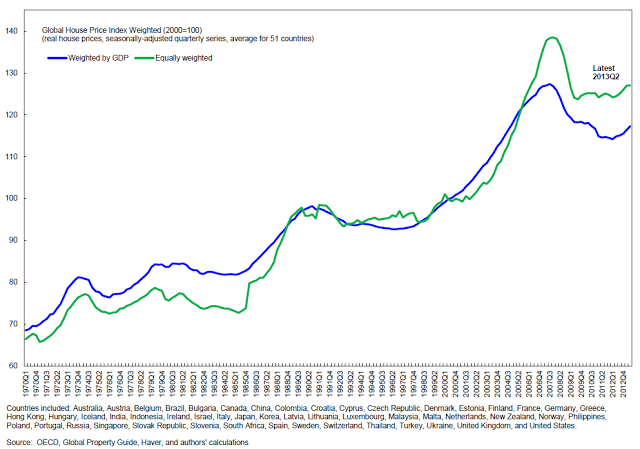

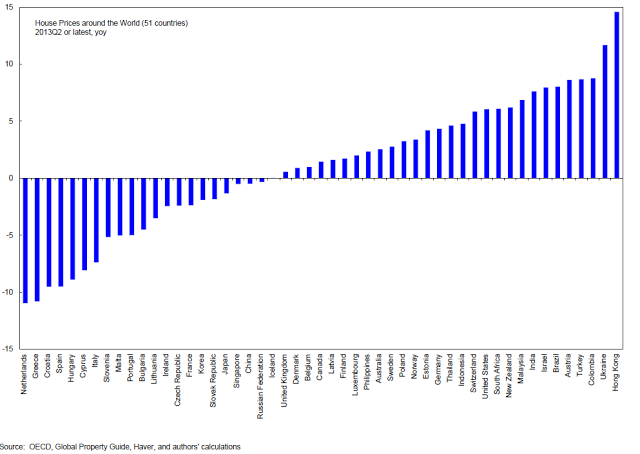

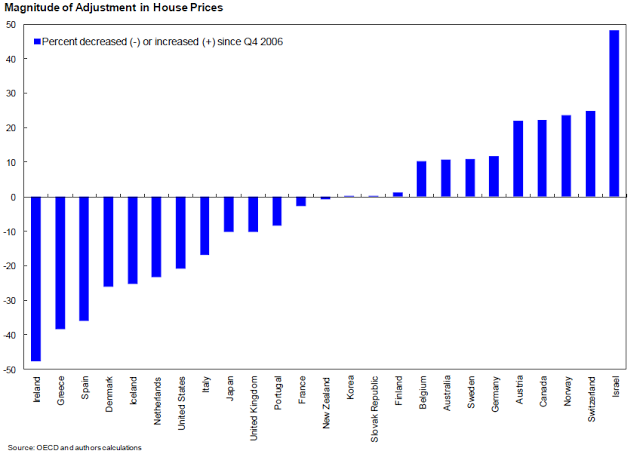

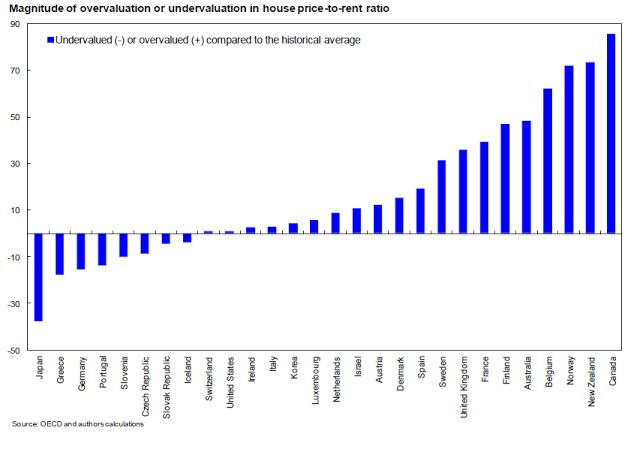

Global House Price Watch

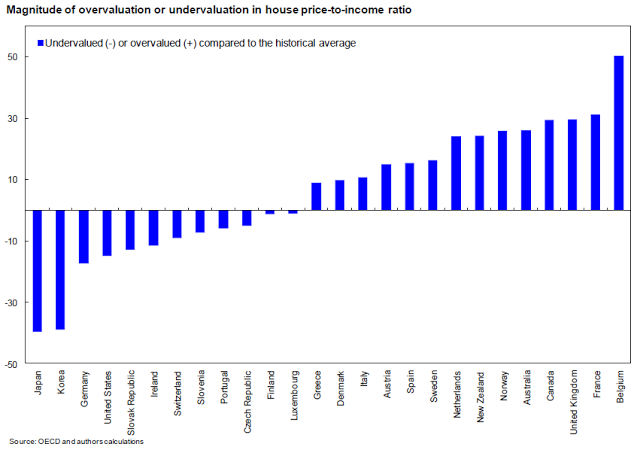

2. … with house prices rising in 30 countries out of 51 included in the index

3. Among OECD countries, increases and declines are more evenly balanced

4. In most OECD countries house price-to-rent ratios remain above their historical averages …

5. … as do house price-to-income ratios

Here’s the full report.

1. Index of global house prices keeps inching up …

2. … with house prices rising in 30 countries out of 51 included in the index

3. Among OECD countries, increases and declines are more evenly balanced

4. In most OECD countries house price-to-rent ratios remain above their historical averages …

5.

Posted by at 10:23 PM

Labels: Global Housing Watch

Tuesday, September 10, 2013

House Prices in Austria

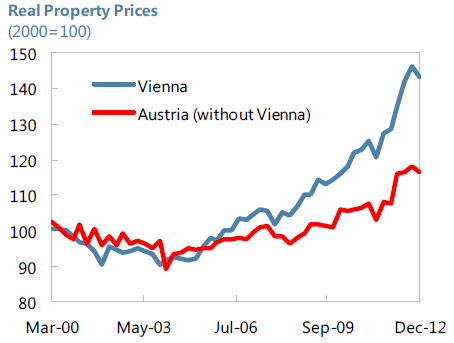

“The housing market has experienced strong price growth but from low levels. In nominal terms at end-2012, house prices rose 14.9 percent y-o-y in Vienna compared with 11.5 percent y-o-y for Austria overall. In real terms and from a medium-term perspective, the price increase appears more modest: a cumulative 40 percent over 10 years in Vienna and about 5 percent in the rest of Austria. Housing market activity seems to be driven largely by non-resident buyers and domestic investors seeking an alternative to low fixed-income returns, though continued immigration also likely supported demand for housing in urban areas. Mortgage credit has exhibited slow growth, suggesting the prevalence of equity buyers,” according to the IMF’s annual report on Austria.

“The housing market has experienced strong price growth but from low levels. In nominal terms at end-2012, house prices rose 14.9 percent y-o-y in Vienna compared with 11.5 percent y-o-y for Austria overall. In real terms and from a medium-term perspective, the price increase appears more modest: a cumulative 40 percent over 10 years in Vienna and about 5 percent in the rest of Austria. Housing market activity seems to be driven largely by non-resident buyers and domestic investors seeking an alternative to low fixed-income returns,

Posted by at 4:01 PM

Labels: Global Housing Watch

Thursday, September 5, 2013

House Prices in the Nordics

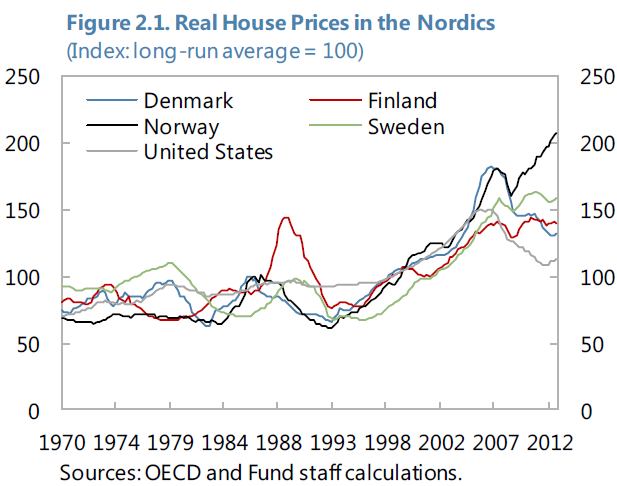

“House prices in the Nordic-4 [Denmark, Finland, Norway, and Sweden] rose in tandem from the mid-1990s until the recent peaks in 2007 but diverged afterwards. House prices increased by more than 120 percent on average in the Nordic countries between 1995 and 2007 (see Figure 2.1). Since 2007 peaks, house price co-movements seem to have dissipated. The real house price in Norway increased by more than 10 percent relative to the 2007 peak level, while house prices fell by close to 30 percent in Denmark. In Finland and Sweden, house prices have remained broadly constant around 2007 levels,” according to an IMF report on the Nordic Region.

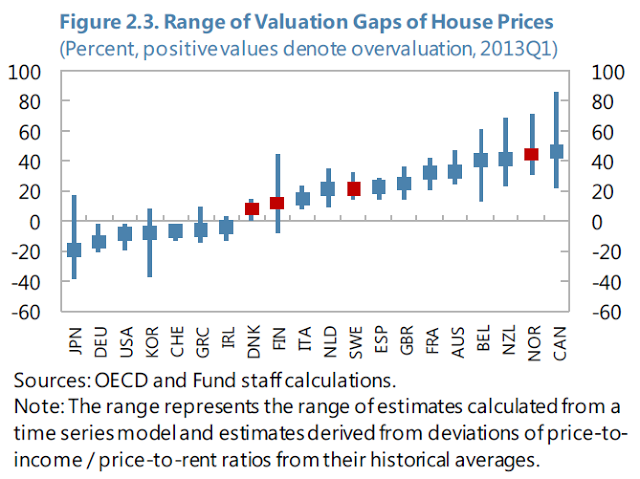

“The estimates suggest house prices are overvalued in the Nordic-4, but the extent of overvaluation varies (see Figure 2.3). The chart shows both the range and the mean of house price gaps based on the three different measures discussed above [(i) a time-series model; (ii) deviations from a long-run price-to-income ratio; and (iii) deviations from a long-run price-to-rent ratio]. The average estimate of the valuation gap for Norway is just over 40 percent while the estimated valuation gap is less than 10 percent in Denmark. Average estimates for Finland and Sweden suggest that house prices are moderately overvalued, by 12 and 22 percent, respectively.”

“House prices in the Nordic-4 [Denmark, Finland, Norway, and Sweden] rose in tandem from the mid-1990s until the recent peaks in 2007 but diverged afterwards. House prices increased by more than 120 percent on average in the Nordic countries between 1995 and 2007 (see Figure 2.1). Since 2007 peaks, house price co-movements seem to have dissipated. The real house price in Norway increased by more than 10 percent relative to the 2007 peak level, while house prices fell by close to 30 percent in Denmark. In Finland and Sweden,

Posted by at 7:40 PM

Labels: Global Housing Watch

House Prices in Norway

“House prices continue to rise in Norway. There was only a brief correction at the time of the global financial crisis. Real house prices increased by nearly 30 percent from its lowest level in 2008. Standard affordability indicators are also worsening. Price-to-income and price-to-rent ratios increased by 14 percent and 23 percent, respectively, from their lowest levels in 2008. Several factors have been identified to explain the upward trend of house prices, including robust income growth and high population growth due to immigration (see Box 2.1). While these factors may partly explain recent house price developments, there are also risks associated with a house price reversal, and household would be vulnerable to house price corrections given the high levels of household debt,” according to a new report by the IMF.

“House prices continue to rise in Norway. There was only a brief correction at the time of the global financial crisis. Real house prices increased by nearly 30 percent from its lowest level in 2008. Standard affordability indicators are also worsening. Price-to-income and price-to-rent ratios increased by 14 percent and 23 percent, respectively, from their lowest levels in 2008. Several factors have been identified to explain the upward trend of house prices, including robust income growth and high population growth due to immigration (see Box 2.1).

Posted by at 7:39 PM

Labels: Global Housing Watch

Subscribe to: Posts