Showing posts with label Global Housing Watch. Show all posts

Friday, July 4, 2014

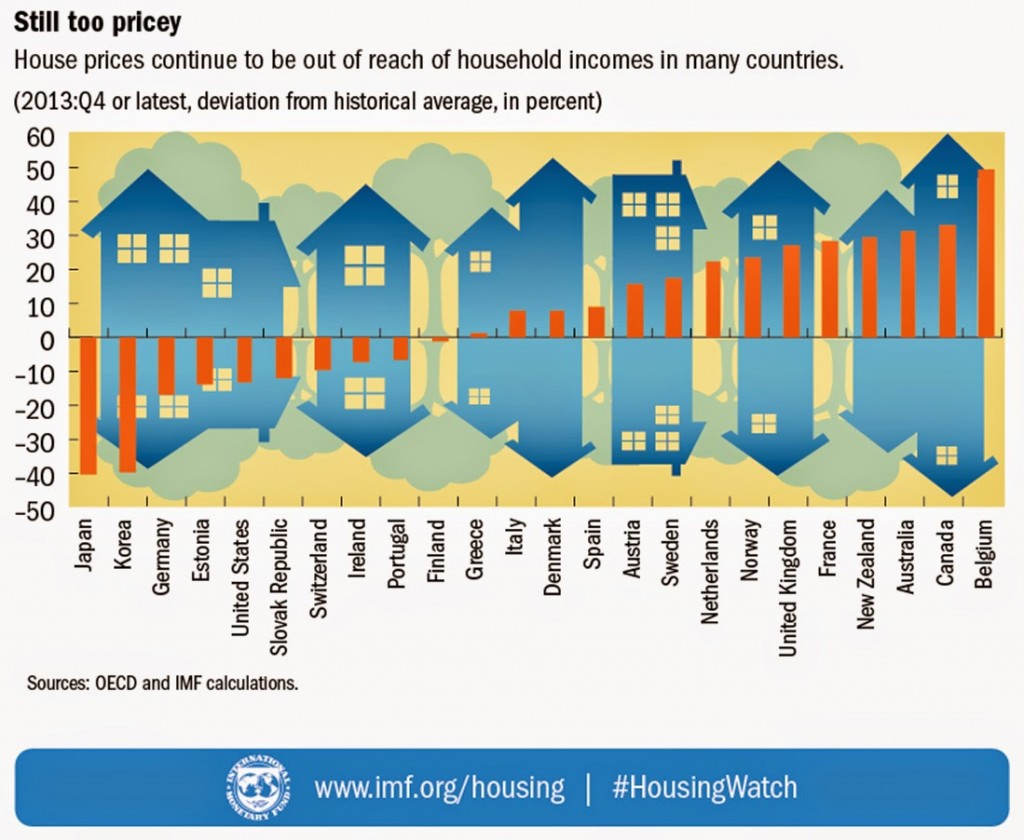

House Prices in France

“(…) the gradual correction of real estate prices which is underway–real prices are 9 percent below pre-crisis peak (…),” according to the IMF’s new economic report on France.

“(…) the gradual correction of real estate prices which is underway–real prices are 9 percent below pre-crisis peak (…),” according to the IMF’s new economic report on France.

Posted by at 12:22 AM

Labels: Global Housing Watch

Friday, June 27, 2014

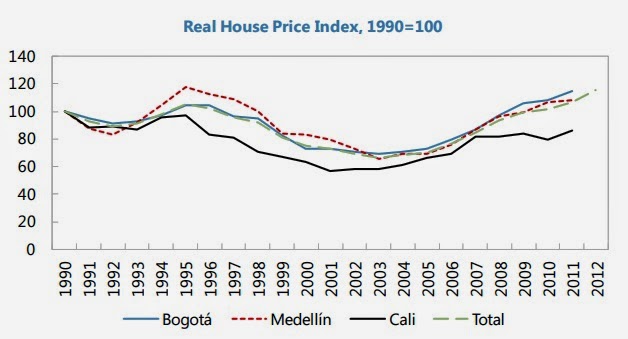

House Prices in Colombia

“Housing prices have increased substantially in recent years. House prices have nearly doubled in real terms over the last decade and are 20 percent above the peak in 1996, driven mainly by prices in the capital and two other cities. (…) Mortgages have increased more recently but credit risks appear to be largely under control,” according to a new IMF report on Colombia.

“Housing prices have increased substantially in recent years. House prices have nearly doubled in real terms over the last decade and are 20 percent above the peak in 1996, driven mainly by prices in the capital and two other cities. (…) Mortgages have increased more recently but credit risks appear to be largely under control,” according to a new IMF report on Colombia.

Posted by at 8:50 PM

Labels: Global Housing Watch

Thursday, June 26, 2014

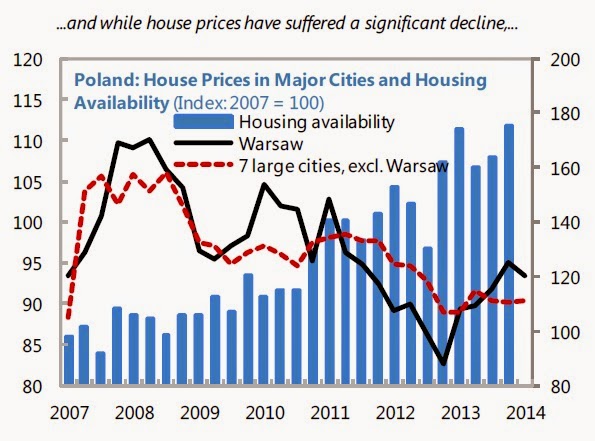

House Prices in Poland

Posted by at 6:30 PM

Labels: Global Housing Watch

Monday, June 16, 2014

Era of Benign Neglect of House Price Booms is Over

While the recent recovery in global housing markets is a welcome development, we need to guard against another unsustainable boom. says IMF’s Deputy Managing Director Min Zhu in a blog. He also gave the opening remarks at the Bundesbank/German Research Foundation/IMF Conference that took place recently.

While the recent recovery in global housing markets is a welcome development, we need to guard against another unsustainable boom. says IMF’s Deputy Managing Director Min Zhu in a blog. He also gave the opening remarks at the Bundesbank/German Research Foundation/IMF Conference that took place recently.

Posted by at 1:03 AM

Labels: Global Housing Watch

Monday, June 9, 2014

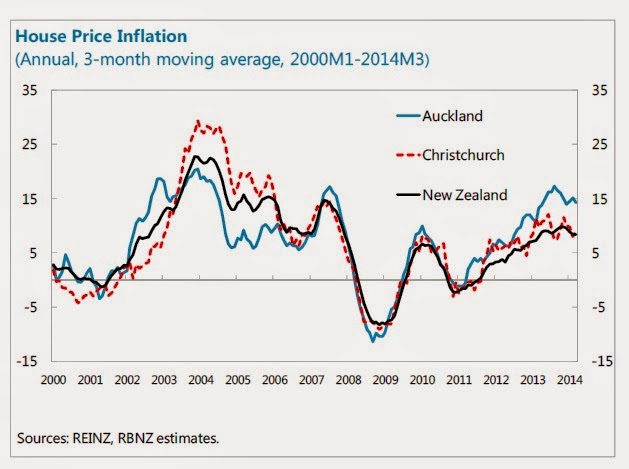

House Prices in New Zealand

“By historical and international comparisons and some measures of affordability New Zealand’s house prices appear elevated (…). This in part reflects a limited housing stock from low housing investment in recent years and geographical constraints preventing a rapid housing supply response. With house price inflation running high, there remains the risk that expectations-driven, self-reinforcing demand dynamics and price overshooting could take hold.

The government’s steps to help alleviate supply bottlenecks, measures to tighten standards for

mortgage lending (…), and an increase in mortgage rates should help ease price pressures. But a sudden price correction—possibly triggered by a shock to household incomes or borrowing costs—could reduce consumer confidence, impact overall economic activity,

and hurt banks’ balance sheets,” according to the IMF’s new economic report on New Zealand.

“By historical and international comparisons and some measures of affordability New Zealand’s house prices appear elevated (…). This in part reflects a limited housing stock from low housing investment in recent years and geographical constraints preventing a rapid housing supply response. With house price inflation running high, there remains the risk that expectations-driven, self-reinforcing demand dynamics and price overshooting could take hold.

The government’s steps to help alleviate supply bottlenecks, measures to tighten standards for

mortgage lending (…),

Posted by at 10:32 PM

Labels: Global Housing Watch

Subscribe to: Posts