Showing posts with label Global Housing Watch. Show all posts

Monday, September 14, 2015

Macroprudential Policies in the Philippines

The IMF’s report on the Philippines points out the macroprudential policies that have been implemented. The report says: “In light of the acceleration in credit growth in 2014 and risks of domestic asset price booms, the BSP [Central Bank of Philippines] conducted stress tests on banks’ real estate loan exposures and required corrective actions, enhanced monitoring of banks’ exposures to all types of real estate, and provided guidance on real estate mortgage loans, setting their maximum loan value at 60 percent of the appraised value. These measures have helped to restrain credit growth to the real estate sector. Single borrower limits (set at 25 percent of core capital) should be strictly enforced with the additional 25 percent allowance for exposures to PPPs allowed to lapse.”

The IMF’s report on the Philippines points out the macroprudential policies that have been implemented. The report says: “In light of the acceleration in credit growth in 2014 and risks of domestic asset price booms, the BSP [Central Bank of Philippines] conducted stress tests on banks’ real estate loan exposures and required corrective actions, enhanced monitoring of banks’ exposures to all types of real estate, and provided guidance on real estate mortgage loans,

Posted by at 9:00 AM

Labels: Global Housing Watch

Friday, August 21, 2015

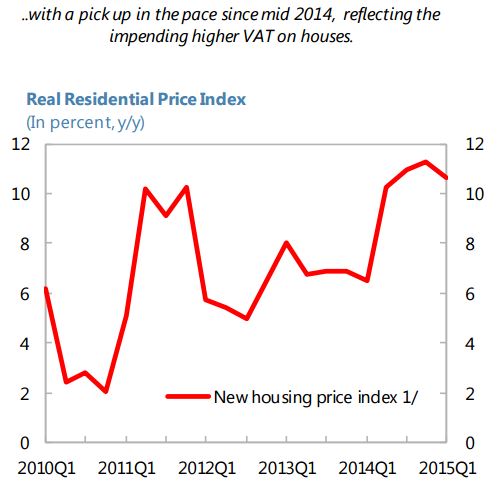

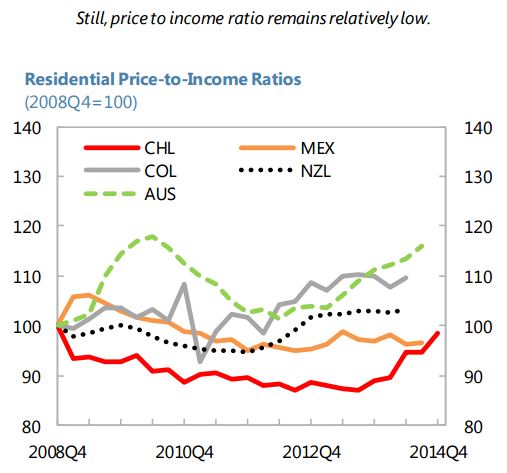

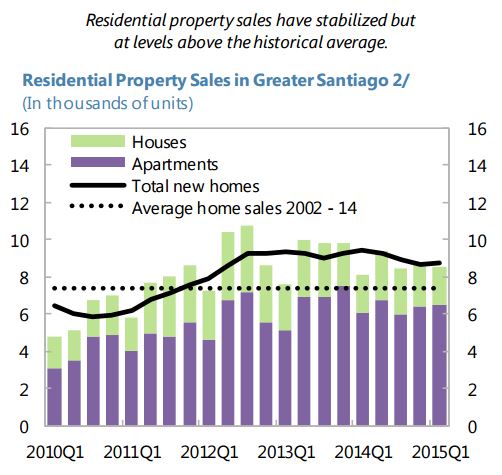

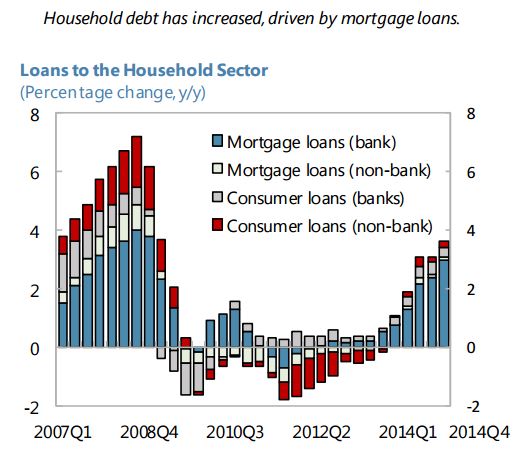

Chile’s Housing Market

Posted by at 9:00 AM

Labels: Global Housing Watch

Wednesday, August 19, 2015

Spain’s Housing Market

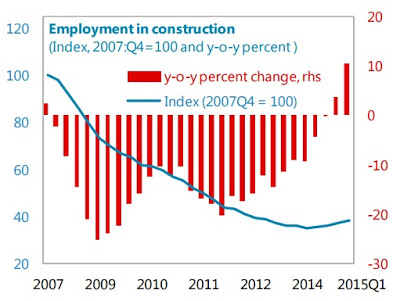

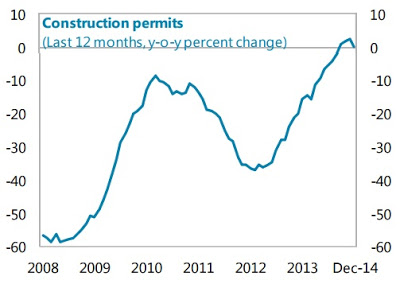

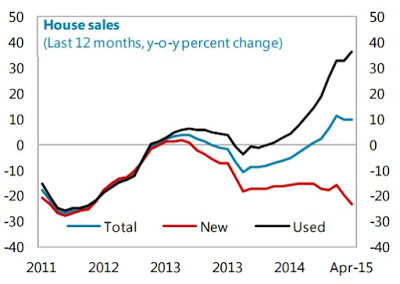

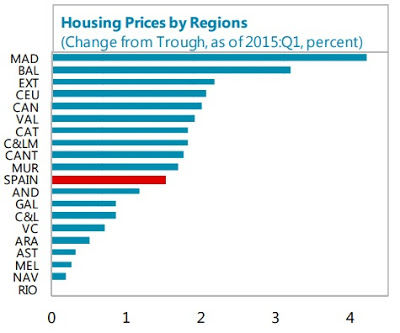

The Spanish housing sector appears to have bottomed out, says the IMF’s new report on Spain. The report notes that the construction activity has started to recover, mostly driven by the non-residential sector. Moreover, construction permits have stopped falling and house sales are picking up. And housing prices started to increase slightly, albeit unevenly across regions.

Below are six charts that show the developments in the housing market in Spain.

Posted by at 9:00 AM

Labels: Global Housing Watch

Monday, August 17, 2015

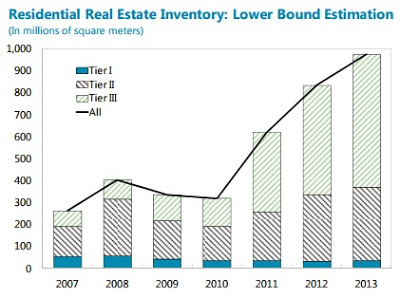

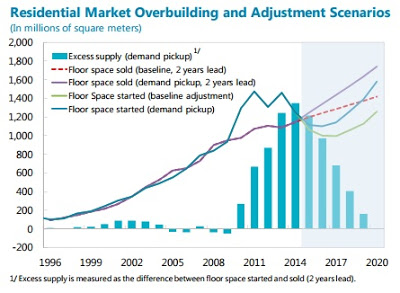

China: How Big Is the Risk of a Real Estate Slowdown and Does It Matter?

How big is the risk of a real estate slowdown? The report says:

“All indicators point to weakness in China’s housing market. Housing prices have been moderating both at the national level and across all city tiers, with the weakest performance among the smaller cities. (…) Housing inventory ratio—floor space unsold to floor space sold—shows a buildup since 2013, suggesting oversupply. Even though there is uncertainty regarding the level (National Bureau of Statistics (NBS) data show inventory of four months, while data from local housing bureaus suggest higher than two years), the direction of the buildup is clear. Inventory is especially high in Tier 3 and Tier 4 cities.”

Does it matter? The report says:

“Continued adjustment in floor space starts is warranted to let demand catch up with supply. (…) The adjustment will have significant impact on GDP growth. Given the estimated relationship between growth in floor space starts and in real estate gross fixed capital formation (GFCF), real estate GFCF could slow to -2 to -4 percent in 2015 from about 3 percent in 2014. As real estate GFCF accounts for about 9 percent of GDP, this would imply a drop of GDP growth by about ½ percentage point in the baseline scenario. This abstracts from the indirect effect arising from real estate linkages to upstream and downstream sectors. Some of these sectors suffer from oversupply, and a slowdown in construction activity could bring losses, exposing vulnerabilities and posing risks (…).”

“China’s housing market has softened visibly since 2014, reflecting oversupply in most cities. More adjustment is likely”, says the IMF’s latest report.

How big is the risk of a real estate slowdown? The report says:

“All indicators point to weakness in China’s housing market. Housing prices have been moderating both at the national level and across all city tiers, with the weakest performance among the smaller cities. (…) Housing inventory ratio—floor space unsold to floor space sold—shows a buildup since 2013,

Posted by at 9:00 AM

Labels: Global Housing Watch

Wednesday, August 12, 2015

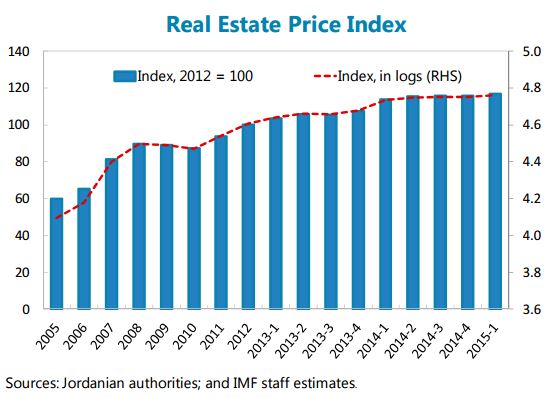

House Prices in Jordan

“Mortgages slowed down in tandem with real estate prices; exposure of banks to real estate credit risk has remained limited”, notes the latest IMF report on Jordan.

Posted by at 9:00 AM

Labels: Global Housing Watch

Subscribe to: Posts