Showing posts with label Global Housing Watch. Show all posts

Monday, March 21, 2016

Financial Stability and Interest-Rate Policy

The paper notes that “At the current conjuncture Canada represents an interesting case: Monetary policy faces the dilemma of supporting a struggling economy by cutting interest rates and maintaining financial stability in a context of high household debt and ever growing housing prices.”

The paper’s “findings show that it is very unlikely that the benefits of having a meaningfully tighter policy (i.e., at least 25 basis points higher than otherwise) would outweigh its costs, in the current Canadian context. In fact, even though the interest rate increase reduces the growth of real household credit and house prices and the ratio of household debt to GDP, the reduction in the crisis probability is minor and peaks only after about 8 years. At the same time, costs are front loaded and magnified by the tighter economic conditions. The policy rate path which takes into account financial stability risks is, thus, only 6 basis points higher than otherwise (for 8 quarters)—which, quantitatively, is not a meaningful policy alternative. A policy rate that is 25 basis points higher than otherwise (for 8 quarters) is expected to be welfare improving only under a scenario where a crisis would impose severe costs on the economy and real credit is expected to grow (in absence of policy intervention) at or above 9 percent a year for the next 3 consecutive years.”

“Should monetary policy use its short-term policy rate to stabilize the growth in household credit and housing prices with the aim of promoting financial stability? (…) the answer is no— especially when the economy is slowing down”, according to a new IMF working paper by Andrea Pescatori and Stefan Laseen–Financial Stability and Interest-Rate Policy: A Quantitative Assessment of Costs and Benefits.

The paper notes that “At the current conjuncture Canada represents an interesting case: Monetary policy faces the dilemma of supporting a struggling economy by cutting interest rates and maintaining financial stability in a context of high household debt and ever growing housing prices.”

Posted by at 7:50 PM

Labels: Global Housing Watch

Wednesday, March 16, 2016

House Prices in Indonesia

“Property prices have been subdued, in tandem with slowing economic growth and weak business sentiment”, notes IMF’s report on Indonesia.

Posted by at 9:00 AM

Labels: Global Housing Watch

Friday, March 11, 2016

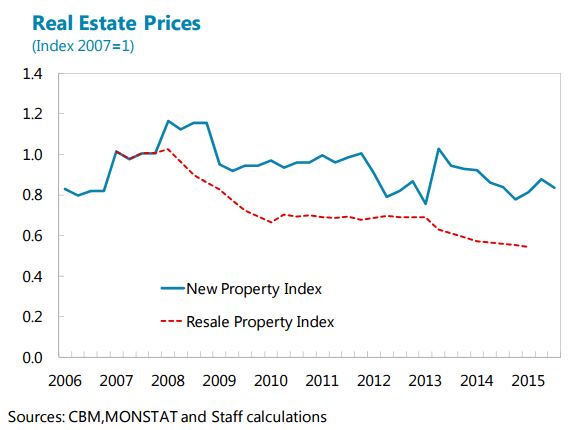

House Prices in Montenegro

“Property prices have continued to fall from their crisis peaks, in part because Russian buying has fallen”, notes the IMF’s report on Montenegro.

Posted by at 10:00 AM

Labels: Global Housing Watch

Wednesday, March 9, 2016

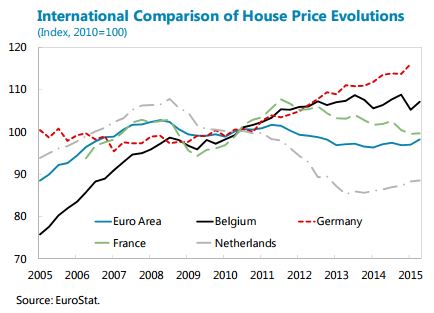

House Prices in Belgium

“After a long period of rapid growth, house prices have stabilized since 2013. A sharp reversal could have a significant impact on consumption, even if banks’ exposures could be managed (…). However, staff analysis does not suggest a major overvaluation, as past price trends were broadly in line with borrowing cost, demographic and income developments”, according to the IMF’s new report on Belgium.

Posted by at 10:00 AM

Labels: Global Housing Watch

Wednesday, March 2, 2016

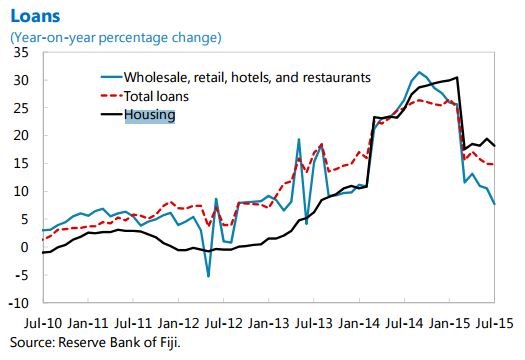

Housing Market in Fiji

“Given still strong credit growth and rapidly rising house prices, the RBF should adopt macroprudential measures to tame the credit and housing price momentum, including through the use of loan-to-value ratios”, says IMF report on Fiji.

Posted by at 10:00 AM

Labels: Global Housing Watch

Subscribe to: Posts