Showing posts with label Global Housing Watch. Show all posts

Tuesday, July 26, 2016

Issi Romem on BuildZoom and the U.S. Housing Market

From Global Housing Watch Newsletter: July 2016

Issi Romem is the Chief Economist at BuildZoom—a start-up in San Francisco. For this issue of the Global Housing Watch newsletter, he talked to Hites Ahir about BuildZoom and what it offers, whether the expansion of American cities has slowed down, and what BuildZoom’s data tell us about the current state and the short term outlook for the U.S. housing market.

Hites Ahir: Tell us a bit about your background and what sparked your interest in housing markets.

Issi Romem: In pursuit of my life long passion for observing and understanding cities, I earned a PhD in economics at the University of California at Berkeley. Economics offers a particular lens with which to analyze cities and contains several fields that relate to them. I chose to focus on labor and housing markets. As the Chief Economist at BuildZoom, I leverage my role to continue studying cities in alignment with the company’s needs.

Hites Ahir: Tell us about BuildZoom and your role in the company?

Issi Romem: BuildZoom actively helps people find good, reliable and communicative contractors, and helps see the projects through to completion. In order to inform the matching of people and contractors, BuildZoom collects data on contractor licensing as well as a growing national repository of building permit data. BuildZoom makes the data easy and free for the public to view on the web, which is particularly valuable because – unlike customer recommendations or photos – a paper trail of building permits shows a contractor’s professional experience in a way that cannot be falsified.

My role at BuildZoom includes the production of data-driven content for the website, as well as oversight of data science and the company’s data collection efforts. The data-driven content includes the production of economic indices of remodeling and new construction activity, as well as one-off economic analyses. It also includes trawling new building permits for newsworthy information, such as projects undertaken by companies that are particularly interesting to the public.

Hites Ahir: In the United States, there are a lot of companies that provide data and analysis on the U.S. housing market. So what is unique about BuildZoom?

Issi Romem: BuildZoom’s data sheds light on all types of new construction and remodeling activity. Remodeling, in particular, is an otherwise hidden aspect of the nation’s real estate stock, on which there are very few sources of information. Moreover, as some of the greatest metro areas in the nation restrict their supply of new housing, more and more of the action in these cities’ real estate markets involves the renovation and/or repurposing of the existing stock of structures, into which BuildZoom’s data sheds light.

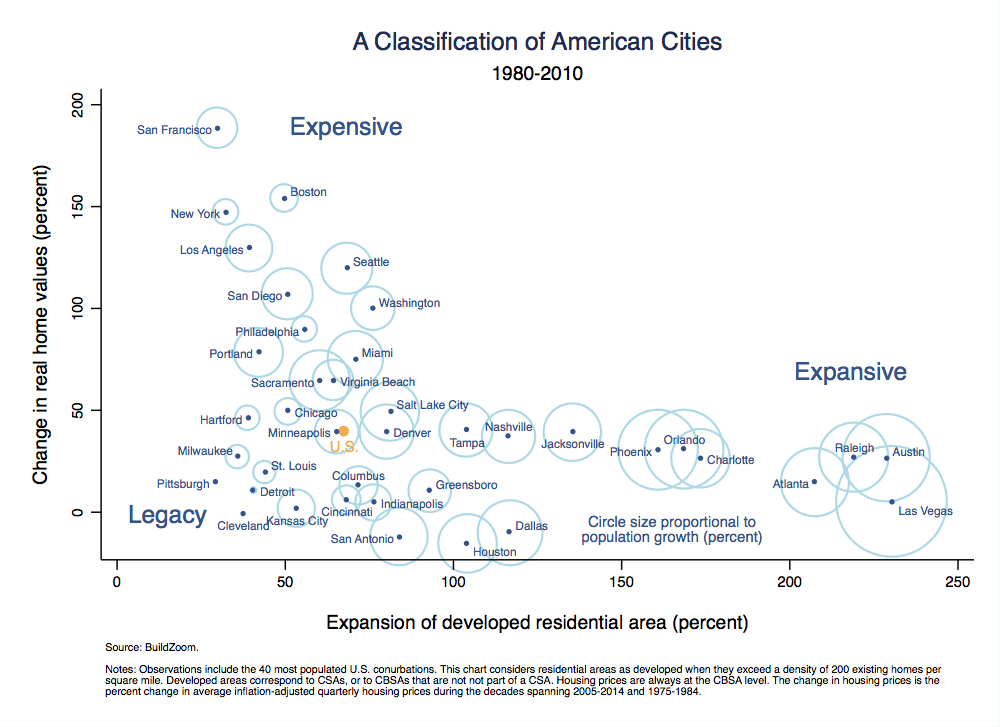

Hites Ahir: You recently wrote on whether the expansion of American cities has slowed down. What is the verdict?

Issi Romem: The expansion of American Cities as a whole has not slowed down. It has kept progressing at a more or less steady pace each decade since World War II. However, there are important differences between cities. One group of cities, consisting mostly of large coastal cities, have indeed slowed down their expansion, and in so doing have channeled their economic strength away from population growth and into housing price growth. I refer to these as expensive cities. Another group of cities, mostly in the south, have continued to expand with gusto, and as a result have experienced tremendous population growth while maintaining housing prices at affordable levels. I refer to these as the expansive cities, with an a. Finally, a third group of cities mostly in the rust belt had thriving economies in the past, but have lost much of their economic base, and experienced neither housing price growth nor population growth. I refer to this last group as legacy cities. See the full report here.

Hites Ahir: Based on BuildZoom’s building permits and remodeling data, what can you tells us about the current state of the U.S. housing market?

Issi Romem: The index tells us that, during the last decade’s boom and bust cycle, residential remodeling peaked and plummeted in sync with residential new construction. However, it also tells us that during the bust, new residential construction suffered much more than residential remodeling, and that residential remodeling is currently much closer to its pre-bust level than new construction. During downturns, new construction essentially grinds to a halt, but remodeling combines procyclical elements, like renovations preceding or following a home sale, with elements that are acyclical, like maintenance. The latter keep fluctuations in remodeling less pronounced than those of new construction.

Hites Ahir: What is your view on the short term outlook for the U.S. housing market?

Issi Romem: Predicting where the housing market is going in the short term is tricky business. I suspect that a downward correction in housing prices is possible, but far from certain, and that if it occurs it will be very minor compared to the previous decade’s bust, and will be concentrated in the expensive coastal cities. If and until such a correction occurs, we are likely to see particularly robust housing price increases in places that receive the greatest influx of homeowners migrating out of the expensive coastal cities. Portland (Oregon), Seattle and Denver, for example, draw particularly large inflows of former residents priced out of California. Such places are also susceptible to experiencing a price correction if the influx of homeowners migrating out of the expensive coastal cities were to ease, following a price correction there.

From Global Housing Watch Newsletter: July 2016

Issi Romem is the Chief Economist at BuildZoom—a start-up in San Francisco. For this issue of the Global Housing Watch newsletter, he talked to Hites Ahir about BuildZoom and what it offers, whether the expansion of American cities has slowed down, and what BuildZoom’s data tell us about the current state and the short term outlook for the U.S.

Posted by at 5:00 AM

Labels: Global Housing Watch

Thursday, July 21, 2016

Karl E. Case: Remembering A Top Housing Market Guru

by: Hites Ahir

Karl E. Case is considered one of the top gurus on housing markets and a pioneer in studying their link to the broader economy. Case was a Professor of Economics Emeritus at Wellesley College, where he taught for 34 years. Afterwards he worked as a Senior Fellow at the Joint Center for Housing Studies at Harvard University. He died on July 15. He was 69.

The index that’s named after him

At 9:00 AM on the last Tuesday of every month, an index that measures house prices of single-family houses in 20 major markets in the United States is released. This release is closely watched by experts across the nation and in other countries as well. It also makes it into headline news on a regular basis. In February 2008, the release of the index “made a particularly big splash [in the news]. It showed that prices fell 8.9 percent in 2007, the largest decline in the index’s 20-year history” (Metro West Magazine). This is the S&P Case-Shiller Home Price Indices and it is named after Karl E. Case and Robert Shiller—a Professor of Economics at Yale University—together they developed the now famous index.

On the importance of the index, “In all of economics, I can’t think of five data construction efforts in the last quarter-century that were larger contributions than the Case-Shiller index”, says Larry Summers—a former Harvard University president and U.S. Treasury during the Clinton Administration (Boston Globe). In a separate post, Stan Humphries—Chief Analytics Officer and Chief Economist at Zillow Group—says that “Zillow was born out of a groundswell movement among consumers, researchers and policymakers for more data around everything housing in America. And in no small part, that movement itself owes its beginnings to Chip Case’s work at Wellesley College and the groundbreaking home price index that bears his name.” Karl E. Case was also known as “Chip” among his friends.

So what sparked Case’s interest in housing markets and in creating the house price index? “Case became interested in housing prices in 1985, when real-estate values in Massachusetts — fueled by a high-tech boom — skyrocketed and climbed as much as 40 percent in the span of a year” (Boston Globe). But “Case didn’t know much about bubbles. At the time, he was working on an introductory economics textbook with a friend at Yale, Ray C. Fair. So he asked Fair to recommend an expert in bubbles. Fair responded: Mr. Bubble is across the hall. And that’s where the man whose name was destined to be linked with Case’s came in: Robert J. Shiller. (…) Shiller taught Case about finance and bubbles, and Case taught Shiller about real estate” (Metro West Magazine). The rest is history.

The Great Recession comes

In looking for what Case was saying in the run-up to the Great Recession, you would probably come across many articles. Among them, two are joint commentary in the Wall Street Journal with Shiller. Both commentaries provided a stark warning of the upcoming correction in the housing market.

The first commentary of August 2004 says: “We have a problem: a bubble in the housing market in many locations. In a lot of these places the bubble will eventually deflate. The economic consequences will depend on how the deflation occurs.”

The second commentary of August 2006 says: “Unfortunately, there is significant risk of a very bad period, with slow sales, slim commissions, falling prices, rising default and foreclosures, serious trouble in financial markets, and a possible recession sooner than most of us expected. Deterioration in that intangible housing market psychology is the most uncertain factor in the outlook today. Listen hard and watch out.”

After the Great Recession, at a 2014 conference in honor of Shiller, Case presented a poem. The poem is titled: Reflection on the Housing Market: Seven Years After the Fall (Wall Street Journal). Here are few lines from the poem:

It didn’t matter what rate you paid

Or what you made in a year

For a while liquidity led to stupidity

“Just sign and see the cashier”

High LTV’s and Option ARMs

Negative Am’s and more

2-28’s with teaser rates

And ridiculous Fico scores

Beyond the index and the Great Recession

Besides the work that led to developing the index, Case also made important contribution to the real estate market field. In Housing Markets and the Economy: Risk, Regulation and Policy, Edward L. Glaeser—a Professor of Economics at Harvard University and the late John M. Quigley—a former Professor of Economics at UC Berkely, provide an excellent summary of Case’s most influential contributions.

“A major investigation of The Efficiency of the Market for Single-Family Homes, (…), demonstrated how slowly equilibrium in the housing market was achieved. (…) [This] remains the single most influential paper Case has produced”, Glaeser and Quigley writes.

Moreover, “The magnitude and importance of house price fluctuations in affecting consumer welfare led to his important paper explicating the relevance of Index-Based Futures and Options Markets in Real Estate for housing and the real estate market (…). This paper is not among Case’s most widely cited academic works, but it did lead to the practical development of institutions to mediate risk in the housing market. Consumers and investors now trade options on Case-Shiller Home Price Indices for a dozen cities on the Chicago Mercantile Exchange”, notes Glaeser and Quigley.

Also, “In tandem with his studies of housing dynamics, Case has conducted a series of empirical analyses linking local public finance to housing outcomes, especially school expenditures and school quality. His most widely cited paper in local public finance, Property Tax Limits, Local Fiscal Behavior, and Property Values”, according to Glaeser and Quigley.

“Mr. Wellesley”

Even though Case was famous for the S&P Case-Shiller Home Price Indices, he prided himself on his teaching (NPR). A student of Case “recalls spending the third class of her Urban Economics course at Wellesley on a bus touring the Boston area, with Case at a mike explaining the history and challenges of different neighborhoods. For a first-hand lesson in real estate, Case sent students out into the market to go through the motions of buying a house” (Metro West Magazine).

Moreover, “Former students remembered Mr. Case as an exceptionally devoted mentor and ambassador for the liberal arts college who helped recruit student athletes and with his wife, Susan, hosted international students upon their introduction to Wellesley” (Wall Street Journal). They “hosted 37 international students during his time at Wellesley, offering them a home-away-from-home while they attended the college” (Boston Globe).

In a 2007 symposium to honor Case at Harvard University, Elena Ranguelova—a Bulgarian-born economist—“recalled one Christmas when she house sat for the Cases while they visited relatives in Ohio. Before they left, she mentioned to Case that she had a bad toothache. He made an appointment for her to see his family dentist. When she learned that she had to have four wisdom teeth pulled at a cost of $1,200, she asked the student aid society for a loan. But the society told her its funds were exhausted. Hearing this, Case told Ranguelova that he could arrange for the society to find the money. And, sure enough, the dental bill was paid. Some time later, Ranguelova was at a wine-tasting party at the Cases’ house. (Did I mention that he has a wine cellar with bottles more than a half century old?) (…) Suddenly, he was telling a story of how he paid for my [Ranguelova’s] wisdom teeth. Until that moment, she had assumed that she still owed the aid society. Case had let the secret slip” (Metro West Magazine). Talk to Wellesley volleyball coach Dorothy Webb, who calls him “the best fan of athletics I can imagine for any college” (Metro West Magazine).

From flunking a class to receiving an invitation to give a keynote talk

In an interview with NPR (2011), Case is asked: “You’ve had a lot of kudos over the years. Is there anything that sort of stands out as the personally important moment for you?” Case answers: “Last week, we had the 11th hour of the 11th day of the 11th month. I took my first graduate school exam at Harvard at the 11th hour of the 11th day of the 11th month in 1971. And it was taught by a guy named Ed Leamer. I basically flunked that first exam. And I got in the car with my wife and we decided to go look at prep schools because I wasn’t going to make it through economics. Ed Leamer called me up about five years ago. He’s now a dean out at UCLA. And he invited me to come out and give a keynote talk at a conference he was running. And I said, Ed, this is terrific. You flunked me in my first graduate school exam. He, of course, didn’t remember.”

by: Hites Ahir

Karl E. Case is considered one of the top gurus on housing markets and a pioneer in studying their link to the broader economy. Case was a Professor of Economics Emeritus at Wellesley College, where he taught for 34 years. Afterwards he worked as a Senior Fellow at the Joint Center for Housing Studies at Harvard University. He died on July 15. He was 69.

Posted by at 7:26 AM

Labels: Global Housing Watch

Wednesday, July 20, 2016

Evictions and Housing: Why Should We Care?

by: Hites Ahir

Evicted: Poverty and Profit in the American City by Matthew Desmond—is a “brilliant book about housing and the lives of eight families in Milwaukee”, the Guardian writes. From 2008 to 2009, he lives in a trailer park in Milwaukee to study and document the lives of people who spend more than half of their income on rent. The two years of fieldwork generates more than 5,000 pages single-spaced notes (San Francisco Chronicle). He even employs a fact checker to verify every detail (Wall Street Journal).

Desmond is currently the John L. Loeb Associate Professor of the Social Sciences at Harvard University and Co-Director of the Justice and Poverty Project. In 2015, Desmond was awarded a MacArthur “Genius” grant. What follows is a review of the reviews of Desmond’s new book.

Evictions: How big? How serious?

One of the main findings of the book is that “eviction is a much more frequent event than has been thought and has long-term consequences for the health and stability of families (…) from 2009 to 2011, 13% of Milwaukee renters had been evicted (…). Further, renters thus evicted moved to neighborhoods that were on average 5.4 percentage points poorer and 1.8 percentage points more crime-ridden than the neighborhoods in which renters who moved more voluntarily ended up. These findings lend considerable support to the claim that eviction causes poverty.” (Wall Street Journal).

Another review from the New York Times says: “How can you hang on to a job, send your child to school, or build roots in a community if you are constantly changing homes, each one more dilapidated and dangerously located than the next?” The Guardian notes that “an eviction on your record makes the next apartment harder to get.” And “What is clear is that this is a problem that affects a lot of people, with one in five renters spending half or more of their income on housing and over one in five black women having been evicted”, writes the Independent.

There is also a quote from the book that appears in almost all of the reviews. It says: “If incarceration had come to define the lives of men from impoverished black neighborhoods (…) eviction was shaping the lives of women. Poor black men were locked up. Poor black women were locked out.”

Low-income rental housing market: Is it affordable? Is it profitable?

The Independent notes that “Post-war US housing policy has shifted from building and maintaining housing projects for the poor, towards providing limited “vouchers” that can be used with any rental provider.”

However, the problem of limited “vouchers” is that “sixty-seven percent of poor renting families received no federal assistance for housing at all in 2013 (…). The very people least capable of spending 70 to 80 percent of their incomes on rent are exactly the ones forced to do so (…) With vacancy rates for cheap housing in the single digits, the moment is ripe for exploitation. It’s a landlord’s market” (New York Times). “And all of this comes [on top of] gentrification and surging housing costs at a time of stagnant wages” (Boston Globe).

The New York Review of Books points out that “The government says that rent and utilities are affordable if they consume no more than 30 percent of a household’s income. Analyzing census data, Desmond finds that the majority of poor households pay over 50 percent of their income for shelter and more than a quarter pay over 70 percent. Among the tenants in housing court, a third spend at least 80 percent. Evicted’s families double up with strangers, sell food stamps, and pirate electricity but inevitably fall behind.”

Moreover, “You might not think that there is a lot of money to be extracted from a dilapidated trailer park or a black neighbourhood of “sagging duplexes, fading murals, 24-hour daycares”. But you would be wrong”, according to the Guardian. In the book, on one end there is one of the characters—Lamar—a single father and whose legs had to be amputated due to frostbite—makes $628 dollars a month, of which $550 dollars goes to rent, leaving $2.19 a day for the family. Similarly, Arleen—a single mom—spends 95 percent of $628 dollars monthly welfare check on rent for an apartment without appliances (Huffington Post).

On the other end, there is “The landlord who evicts Lamar, Larraine and so many others is rich enough to vacation in the Caribbean while her tenants shiver in Milwaukee. The owner of the trailer park takes in over $400,000 a year” (New York Times). Also, “There is a moment where Sherrena [a landlord in Evicted] is buying a duplex for $8,000, putting a bit of money into it, and recouping her total costs in a year. That’s the kind of return that attracts some folks” (Slate). However, even in the context of contrasting fortunes, the Wall Street Journal asks: “if the profit were less, would those accommodations remain available?”

Policy suggestions?

“We have to recognize how essential housing is to driving down poverty and recognize that we can’t fix poverty without fixing housing” (Slate). So on policy suggestions, Desmond “solutions are simple: grant tenants the right to legal counsel in housing court, and create a universal voucher system for families below a certain income level, modeled after programs already in place in countries like Great Britain and the Netherlands” (San Francisco Chronicle). Desmond proposals also include restriction on the rents landlords can charge.

What is the estimated cost of annual housing assistance for the poor? “Tax relief on housing costs for American homeowners amounts to $171bn a year. Annual housing assistance for the poor is less than a quarter of that. Mortgage interest, tax relief and capital gains exclusions cost the US three times more than the entire cost of universal housing provision, according to the Guardian.

Why should we care?

“The Harvard center found that low-income households with severe rent burdens spent 38 percent less on food than similar households with affordable shelter, 55 percent less on health care, and 60 percent less on transportation (…) Evicted isn’t a depressing book. It is also a stirring reminder that the US accepts as ordinary a depth of poverty that is extraordinary and cruel. At its heart is a simple message: No moral code or ethical principle, no piece of scripture or holy teaching, can be summoned to defend what we have allowed our country to become” (New York Review of Books).

by: Hites Ahir

Evicted: Poverty and Profit in the American City by Matthew Desmond—is a “brilliant book about housing and the lives of eight families in Milwaukee”, the Guardian writes. From 2008 to 2009, he lives in a trailer park in Milwaukee to study and document the lives of people who spend more than half of their income on rent. The two years of fieldwork generates more than 5,000 pages single-spaced notes (San Francisco Chronicle).

Posted by at 7:03 AM

Labels: Global Housing Watch

Tuesday, July 19, 2016

House Prices in Peru

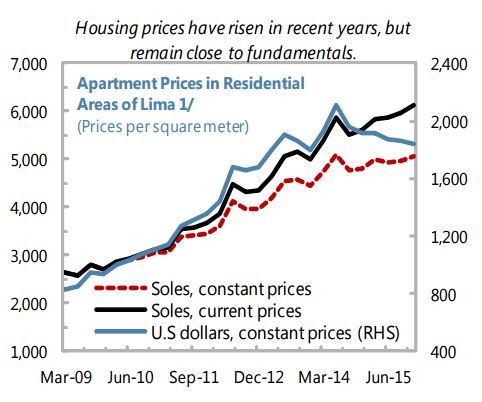

“Housing prices, as reflected by the median apartment prices in Lima, appear high although the price increases since the second half of 2014 have been more subdued than in the previous four years (the average annual growth of apartment prices (in constant soles) from 2011 to first half of 2014 was 14 percent). This may not accurately reflect the segmentation in the market, where there is an oversupply of high-end condominiums in certain residential areas in Lima while low-income housing is in short supply”, says IMF’s report on Peru.

“Housing prices, as reflected by the median apartment prices in Lima, appear high although the price increases since the second half of 2014 have been more subdued than in the previous four years (the average annual growth of apartment prices (in constant soles) from 2011 to first half of 2014 was 14 percent). This may not accurately reflect the segmentation in the market, where there is an oversupply of high-end condominiums in certain residential areas in Lima while low-income housing is in short supply”,

Posted by at 5:00 AM

Labels: Global Housing Watch

Friday, July 15, 2016

Housing Market in Poland

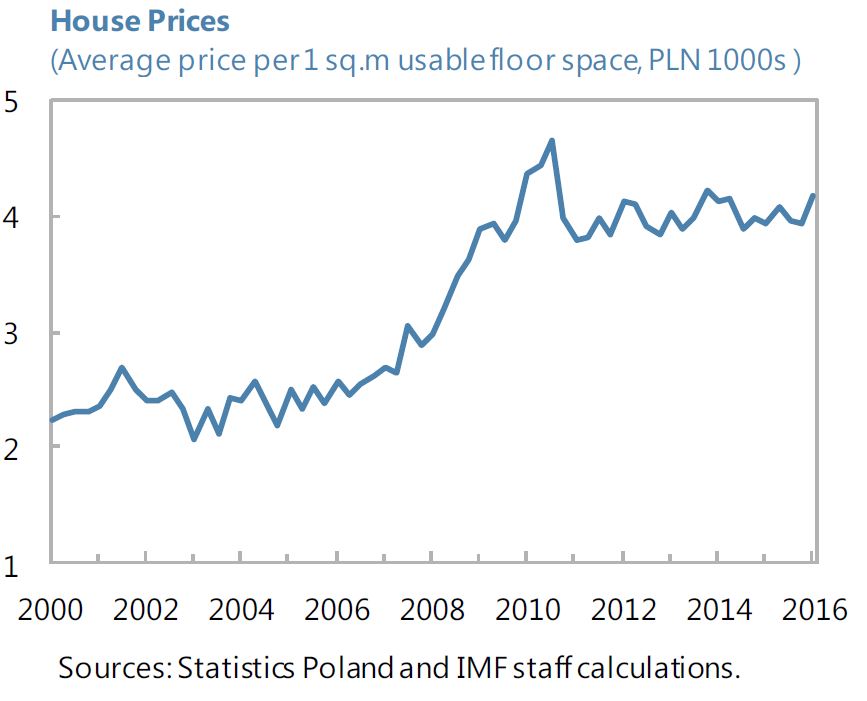

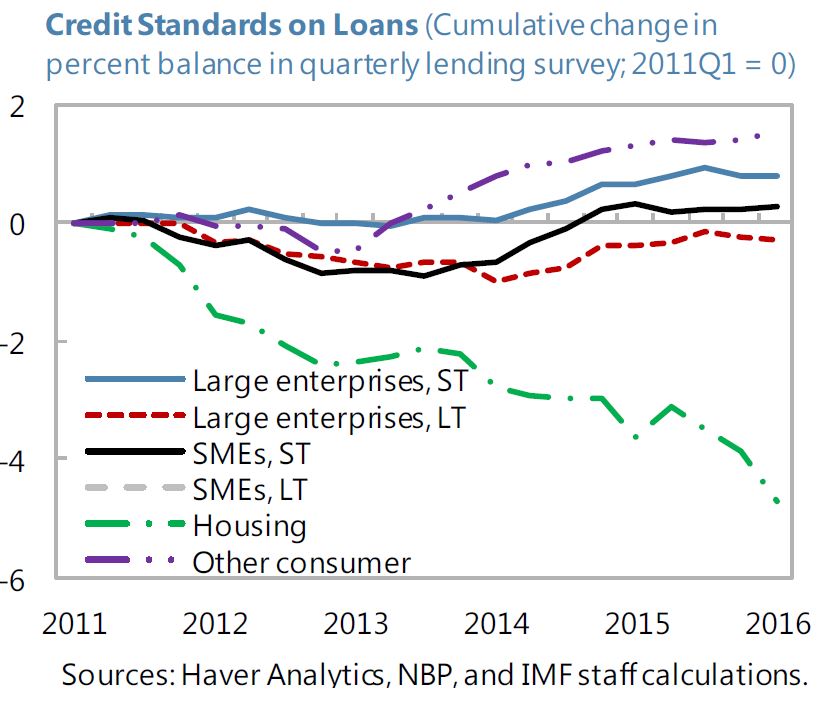

“Credit standards on loans have remained broadly unchanged in recent quarters, with the exception of housing loans, where standards tightened on the back of new prudential recommendations and reduced appetite among some banks for expanding the housing loan portfolio”, says IMF new report on Poland.

“Credit standards on loans have remained broadly unchanged in recent quarters, with the exception of housing loans, where standards tightened on the back of new prudential recommendations and reduced appetite among some banks for expanding the housing loan portfolio”, says IMF new report on Poland.

Posted by at 5:00 AM

Labels: Global Housing Watch

Subscribe to: Posts