Showing posts with label Global Housing Watch. Show all posts

Monday, February 6, 2017

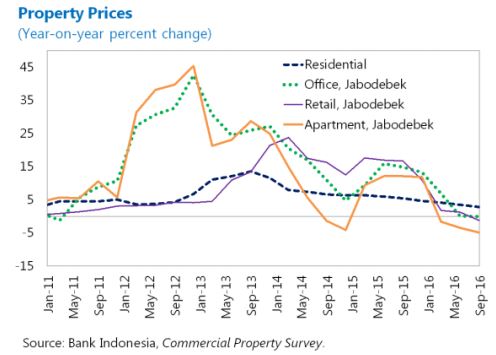

House Prices in Indonesia

“Property prices have been subdued, in tandem with slowing economic growth”, notes IMF’s report on Indonesia.

“Property prices have been subdued, in tandem with slowing economic growth”, notes IMF’s report on Indonesia.

Posted by at 4:10 PM

Labels: Global Housing Watch

Friday, February 3, 2017

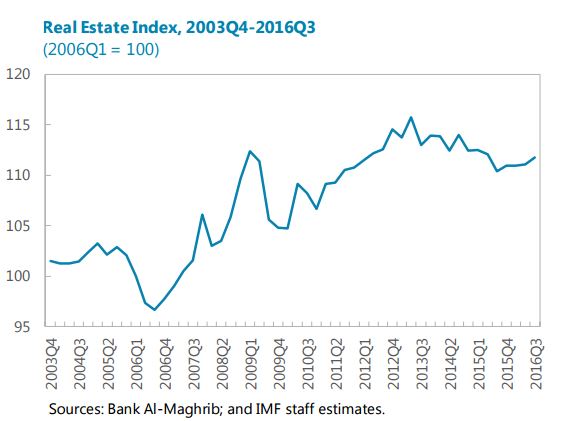

House Prices in Morocco

“Mortgage lending remains moderate (about 5 percent y-o-y) and there is no indication of a housing price bubble”, says IMF’s new report on Morocco.

“Mortgage lending remains moderate (about 5 percent y-o-y) and there is no indication of a housing price bubble”, says IMF’s new report on Morocco.

Posted by at 6:00 PM

Labels: Global Housing Watch

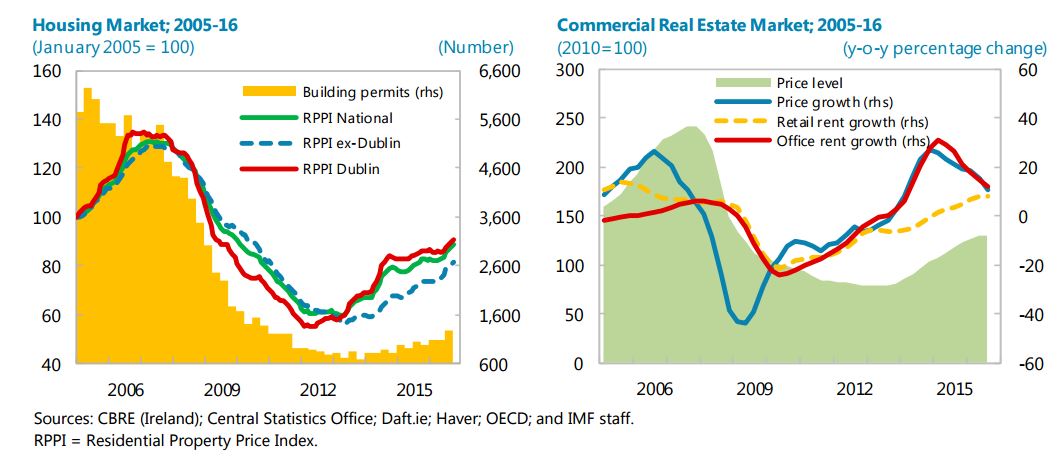

Housing Market in Ireland

The IMF’s report on Ireland says that:

“Property market conditions tightened further, mainly due to a limited supply response. Current conditions have supported robust demand recovery, but housing completions have picked up only moderately, continuing to fall well short of the underlying requirement in the economy. With the stock of properties listed for sale at a nine-year low, house price increases accelerated to 7.1 percent y/y in October 2016. The value of mortgage approvals surged by 43 percent as of November compared to a year earlier, albeit from a relatively low base and in the context of a continued contraction in the stock of outstanding mortgages. Tight housing market conditions have also led to a sharp rise in residential rents, which have now exceeded their pre-crisis peak. In response, the government introduced rental growth caps of 4 percent in Rent Pressure Zones (RPZ) starting in 2017. To ease supply constraints, the government introduced a multipronged Housing Action Plan in July to be implemented over 2017-21 (Annex II). Pressures in the commercial real estate (CRE) market remained strong, and prices increased further, particularly in the office segment. As demand is mostly funded by foreign investors and domestic equity, the exposure of the domestic banking system to the CRE market continued to decline. Despite these pressures, analysis at the time of the 2016 Article IV discussion suggested that current prices are broadly in line with fundamentals in both residential and commercial segments (…).”

On mitigating housing market imbalances, the report says that:

“Efforts to expand and expedite the delivery of housing and rental properties under the Housing Action Plan—a central focus of the current budget—are welcome, particularly those measures directed at mitigating supply constraints. On the contrary, the “Help-to-Buy” (HTB) scheme, set to run through 2019, raises some concerns. While temporary and relatively limited, the program provides only indirect support for supply and carries a relatively high threshold for mortgage value, suggesting scope for better targeting. At the same time, it risks exacerbating demand and pricing pressures. Plans for a phased increase in interest relief for buy-to-let landlords from the current 75 percent to 100 percent by 2021 raise similar concerns. An early review of these fiscal incentives would be warranted to ensure they are well-targeted to assist those most in need and to reduce risks of fueling demand and price pressures. To help address supply bottlenecks, consideration should be given to fasttracking the implementation of a locally levied vacant lot tax, currently expected in 2018, which aims to create incentives to increase land utilization. Administrative measures on rents, however, could dissuade construction and may prove ineffective as landlords could pass on additional costs to tenants through other fees.”

The IMF’s report on Ireland says that:

“Property market conditions tightened further, mainly due to a limited supply response. Current conditions have supported robust demand recovery, but housing completions have picked up only moderately, continuing to fall well short of the underlying requirement in the economy. With the stock of properties listed for sale at a nine-year low, house price increases accelerated to 7.1 percent y/y in October 2016. The value of mortgage approvals surged by 43 percent as of November compared to a year earlier,

Posted by at 6:00 PM

Labels: Global Housing Watch

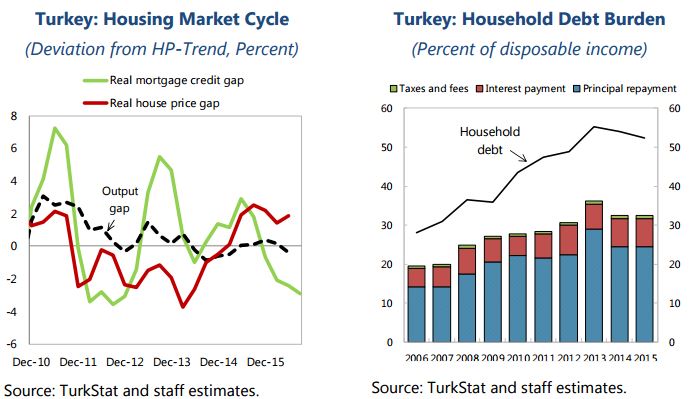

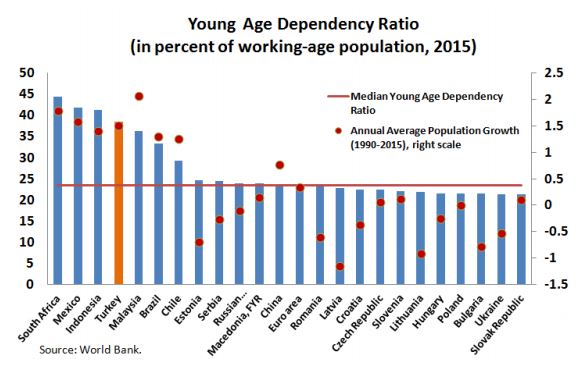

Housing Market in Turkey

Below is an extract from the IMF’s latest report on Turkey:

“Turkish house prices have been markedly increasing for several years. The prices for homes rose cumulatively by 110 percent in nominal and 35 percent in real terms between end-2010 and July 2016. Valuation appears stretched by a number of metrics, such as price-to-income and price-to-rent ratios. The burden of household debt has also increased.

Demographic and socio-economic factors underpin the strong demand for housing. A young and rapidly growing population combined with a high and rising rate of urbanization drive demand for residential housing. In addition, the number of households has increased with a decline in average household size. Household preferences have also shifted toward newer and larger houses, with stronger construction codes.

Special sales campaigns and government stimulus have buoyed house sales since July 2016. The government launched a campaign for subsidized sales of 60,000 houses with mortgages offered at below-market lending rates and higher LTV ratios than the regulatory ceiling, in addition to applying moral suasion on banks to lower mortgage rates. Following the adoption of these measures, total house sales rose by 2 percent year-on-year in August. Since then, the LTV ceiling was raised from 75 to 80 percent.”

Also see a separate IMF report on Understanding Turkish Residential Real Estate Dynamics.

Below is an extract from the IMF’s latest report on Turkey:

“Turkish house prices have been markedly increasing for several years. The prices for homes rose cumulatively by 110 percent in nominal and 35 percent in real terms between end-2010 and July 2016. Valuation appears stretched by a number of metrics, such as price-to-income and price-to-rent ratios. The burden of household debt has also increased.

Posted by at 4:47 PM

Labels: Global Housing Watch

Thursday, February 2, 2017

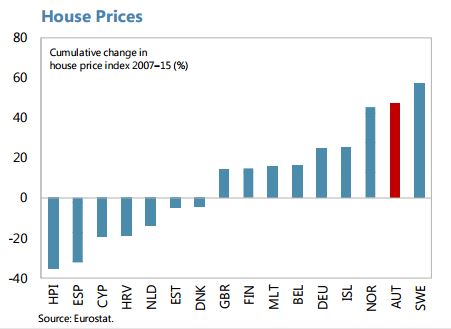

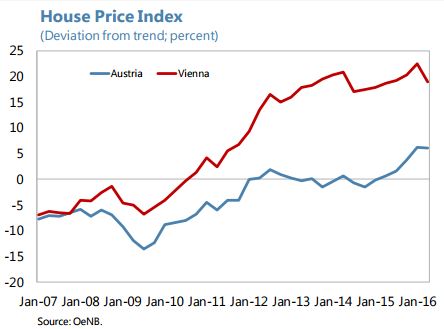

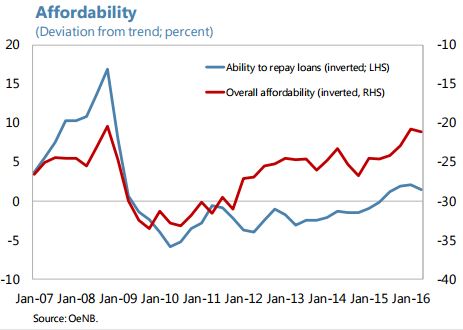

House Prices in Austria

The IMF’s latest economic report on Austria points out that:

“House price growth has been strong in recent years by international comparisons. The cumulative increase in the house price index over 2007–2015 was nearly 40 percent. To a large extent, this increase was driven by price dynamics in Vienna. The OeNB residential price index indicator, which assesses whether prices move in line with fundamental factors, points to an overvaluation of property prices of about 22 percent for Vienna, while prices in the rest of the country appear broadly in line with fundamentals. Price increases in Vienna have moderated lately, while picking up in the rest of the country (…). Low interest rates over recent years have loosened credit constraints and increased households’ borrowing capacity, putting upward pressure on housing demand. That said, prices have been kept high by supply side constraints and other idiosyncratic factors, especially in Vienna. Reviewing and relaxing local planning systems and regulations to facilitate the supply response to price movement can help contain the price rises close to the long run trend. Are the rising prices a problem? Financial stability risks seem contained. (…) Nonetheless, the authorities need to have the legal authority to expand the macroprudential toolkit with real estate-specific instruments when needed, to limit any potential risks to banks’ portfolios if real estate price bubbles were to emerge.”

The IMF’s latest economic report on Austria points out that:

“House price growth has been strong in recent years by international comparisons. The cumulative increase in the house price index over 2007–2015 was nearly 40 percent. To a large extent, this increase was driven by price dynamics in Vienna. The OeNB residential price index indicator, which assesses whether prices move in line with fundamental factors, points to an overvaluation of property prices of about 22 percent for Vienna,

Posted by at 1:19 PM

Labels: Global Housing Watch

Subscribe to: Posts