Showing posts with label Global Housing Watch. Show all posts

Thursday, April 5, 2018

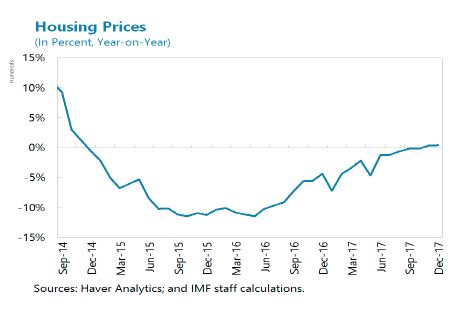

House Prices in Mongolia

The IMF’s latest report on Mongolia says that “(…) housing prices stabilized after years of deflation, in line with stronger economic activity and household lending.”

The IMF’s latest report on Mongolia says that “(…) housing prices stabilized after years of deflation, in line with stronger economic activity and household lending.”

Posted by at 10:40 AM

Labels: Global Housing Watch

Wednesday, April 4, 2018

Housing Market in Luxembourg: Assessment and Policy Recommendations

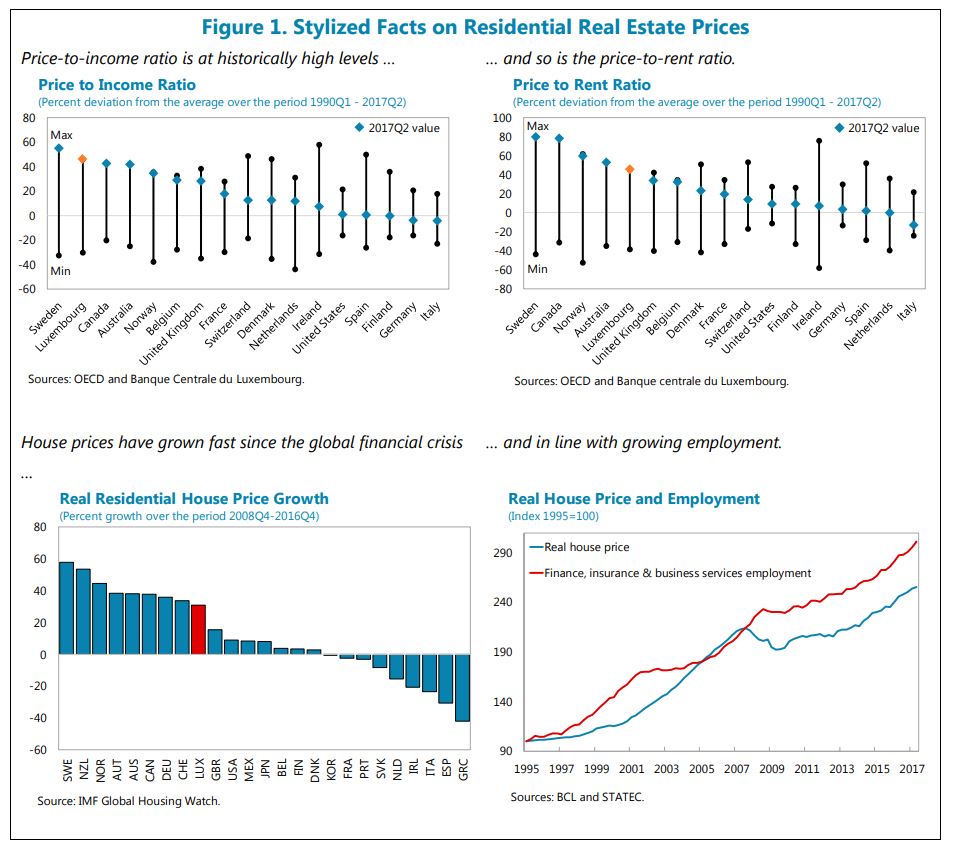

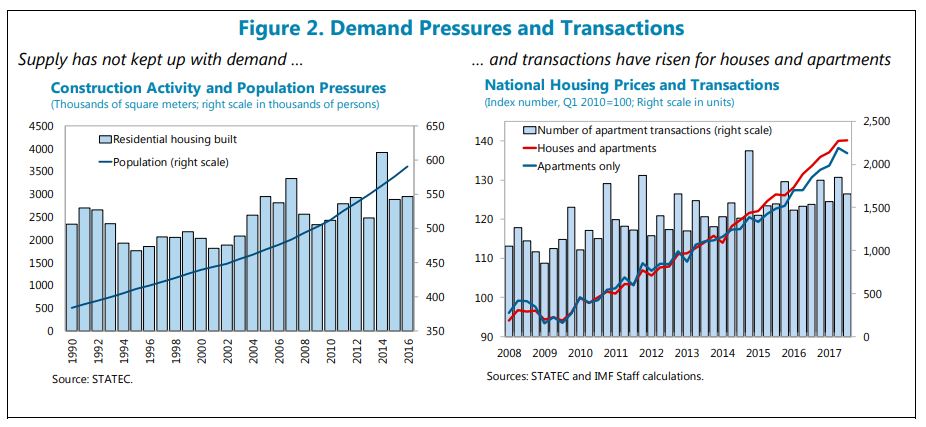

From the IMF’s latest report on Luxembourg:

“Demand for housing has exceeded supply for many years. While house prices are in line with fundamentals, they have risen faster than disposable income for years, largely because of structural supply constraints in the context of strong demand, in part reflecting net demographic growth. The dynamics of house prices is also somewhat affected by cyclical factors such as the cost of construction and to some extent the low interest rate environment. Rigid zoning and administrative rules together with land hoarding prevent sufficient construction, while tax incentives and subsidies fuel demand. Reduced affordability has driven up household indebtedness, in particular among younger households.

Risks in the real estate market should continue to be closely monitored, and further actions taken as needed. Recent measures have appropriately built capital buffers in the banking system while discouraging riskier lending. However, household debt is relatively high and limits to debt-service-to-income ratios should be set if house prices continue to outpace disposable incomes. Going forward, the normalization of interest rates could add to the debt service of some households (who borrowed at variable rates) while banks’ margins on their stock of fixed rate mortgages would shrink.

Containing house price pressures and alleviating bottlenecks of housing require a strong effort to expand the stock of housing:

- Excessive red tape in bringing additional land to construction should be pruned, and incentives strengthened. The initiatives of Baulücken for new construction are a step in the right direction;

- Local zoning decisions should be better coordinated with a national spatial development plan and cooperation among municipalities should be encouraged;

- Existing tools to mobilize vacant land and unoccupied dwellings could be strengthened. This includes implementing taxation on vacant lots. In this respect, the initiative of Baulandvertrag goes in the right direction;

- In the PDAT and the municipal implementation, assigning “mixed construction” land in priority to residential real estate would widen the share of land eligible for housing development;

- Tax biases at the municipality level against residential real estate should be reduced further. The reform of the distribution of municipal business taxes among municipalities is a step in the right direction as it reduces incentives favoring commercial over residential real estate zoning decisions. Going forward, policies should increase the share of the ICC redistributed in the equalization fund;

- Increasing property taxes and revising cadastral values would help municipalities increase own resources.

The share of social and affordable housing in total housing could be increased:

- To encourage social housing in the rental segment, public developers in the social sector (FSH, SNCHM, and municipalities) should be gradually steered only towards the development and management of social rentals. This would help clarify management roles and separate more clearly the rental activity from the construction-for-sale business.”

From the IMF’s latest report on Luxembourg:

“Demand for housing has exceeded supply for many years. While house prices are in line with fundamentals, they have risen faster than disposable income for years, largely because of structural supply constraints in the context of strong demand, in part reflecting net demographic growth. The dynamics of house prices is also somewhat affected by cyclical factors such as the cost of construction and to some extent the low interest rate environment.

Posted by at 4:33 PM

Labels: Global Housing Watch

Friday, March 30, 2018

Housing View – March 30, 2018

On cross-country:

- Mapping the literature of ‘policy transfer’ and housing – UK Collaborative Centre for Housing Evidence

- Mapping the literature on housing taxation in the UK and other OECD countries – UK Collaborative Centre for Housing Evidence

On the US:

- Mortgage Design in an Equilibrium Model of the Housing Market – NBER

- What to Expect From the Housing Market This Spring – New York Times

- California’s Housing Prices Need to Come Down – Citylab

On other countries:

- [Canada] Toronto’s Tale of Two Markets Is Hot Condos and Cold Houses – Bloomberg

- [China] China looks to Reits to ease housing woes – Financial Times

- [China] Does Housing Unaffordability Crowd Out Elites in Chinese Superstar Cities? – Shanghai University of Finance and Economics

- [Germany] Berlin loosens law for short-term home rentals – Reuters

- [Japan] Land ho, a sign of life in Japan – Financial Times

- [Netherlands] Revolutionary housing project brings Dutch youth together with refugees – UNHCR

- [Netherlands] Airbnb rentals in Netherlands are worsening the housing crisis – Global Property Guide

- [United Kingdom] High housing costs deter workers moving to London – Financial Times

- [United Kingdom] Brexit and the City: Tracking the fortunes of London’s financial districts – Reuters

- [United Kingdom] Brexit and the City – the real estate agent’s view – Reuters

Photo by Aliis Sinisalu

On cross-country:

- Mapping the literature of ‘policy transfer’ and housing – UK Collaborative Centre for Housing Evidence

- Mapping the literature on housing taxation in the UK and other OECD countries – UK Collaborative Centre for Housing Evidence

On the US:

- Mortgage Design in an Equilibrium Model of the Housing Market – NBER

- What to Expect From the Housing Market This Spring – New York Times

- California’s Housing Prices Need to Come Down – Citylab

Posted by at 5:00 AM

Labels: Global Housing Watch

Friday, March 23, 2018

Housing View – March 23, 2018

On cross-country:

- The Pursuit of Financial Stability and Tasks for Monetary, Regulatory, and Macro-Prudential Policies – IMF

- True Affordability: Critiquing the International Housing Affordability Survey – Victoria Transport Policy Institute

On the US:

- Affordable housing: Supply side innovation? – Rutgers Center for Real Estate

- Land-Use Regulations, Property Values, and Rents: Decomposing the Effects of the California Coastal Act – Federal Reserve Bank of Philadelphia

- For Low-Income Renters, the Affordable Housing Gap Persists – Citylab

- How Mortgage Companies Might Finally Be Held Accountable – The Nation

- Segregation Forever? Richard Rothstein speaks at the U.S. Department of Housing and Urban Development – Economic Policy Institute

- Mortgage Debt and Shadow Banks – De Nederlandsche Bank

- Housing as a hub for health, community services, and upward mobility – Brookings

- The Seven Sizzling Housing Markets – John Burns Real Estate Consulting

- The Next Housing Crisis: A Historic Shortage of New Homes – Wall Street Journal

- Spring may not be so hot for U.S. housing markets – Global Property Guide

- A housing recovery without homeowners – Federal Reserve Bank of St. Louis

- California Housing Problems Are Spilling Across Its Borders – New York Times

- Trump’s Tariffs Will Make Housing More Unaffordable – Reason

- Valuing urban land: Comparing the use of teardown and vacant land sales – Regional Science and Urban Economics

- Suburban Housing Costs Are Stretching Families to the Brink – Slate

- Commuting, Labor, and Housing Market Effects of Mass Transportation: Welfare and Identification – Federal Reserve Bank of Philadelphia

- How Do Funding and Review Processes Shape the Design of Affordable Housing? – Harvard Joint Center for Housing Studies

On other countries:

- [Canada] The Propagation of Regional Shocks in Housing Markets: Evidence from Oil Price Shocks in Canada – Bank of Canada

- [Iceland] Short-term renting of residential apartments Effects of Airbnb in the Icelandic housing market – Central Bank of Iceland

- [Switzerland] Swiss central bank warns of ‘correction’ in real estate – Financial Times

- [United Kingdom] Rethinking London’s ‘ripple effect’ on house prices: other UK regions transmit shocks too – London School of Economics

- [United Kingdom] Home Ownership Aspirations Survey – Cluttons

Photo by Aliis Sinisalu

On cross-country:

- The Pursuit of Financial Stability and Tasks for Monetary, Regulatory, and Macro-Prudential Policies – IMF

- True Affordability: Critiquing the International Housing Affordability Survey – Victoria Transport Policy Institute

On the US:

- Affordable housing: Supply side innovation? – Rutgers Center for Real Estate

- Land-Use Regulations, Property Values, and Rents: Decomposing the Effects of the California Coastal Act – Federal Reserve Bank of Philadelphia

- For Low-Income Renters,

Posted by at 5:00 AM

Labels: Global Housing Watch

Tuesday, March 20, 2018

A housing recovery without homeowners

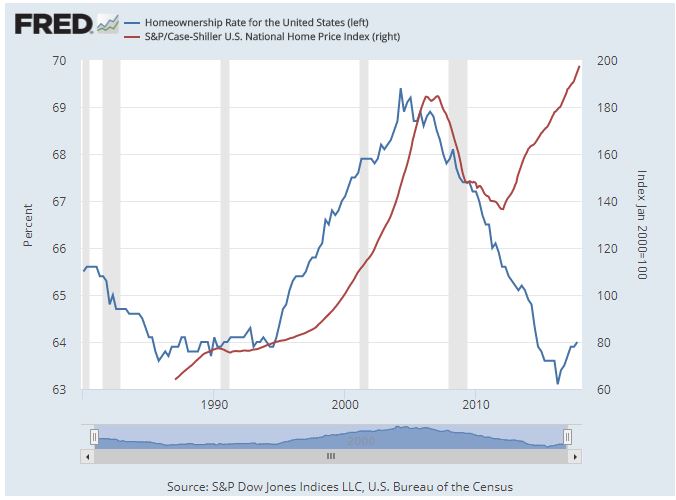

From Federal Reserve Bank of St. Louis:

“Historically, the cost of buying a house has been positively correlated with the percent of households that own their home. During 1996 to 2006 in the United States, both the price of houses and the homeownership rate increased. This increasing trend ended abruptly with the global financial crisis, which saw house prices plunge and drove homeownership rates to historically low levels. If homeownership became less attractive in the wake of the financial crisis, we might expect both prices and homeownership to decrease. Similarly, if the current increase in house prices were driven by people buying homes to live in, we might expect the homeownership rate to increase along with prices. However, recent evidence shows that house prices and homeownership are diverging.

The graph shows that, in the wake of the financial crisis, house prices declined by over 25 percent, from an index value of around 180 to around 135. The homeownership rate also dropped from a high of over 69 percent to just over 63 percent, its lowest level since 1980. Unlike in the past, the homeownership rate continued to fall even after house prices began to recover.

Several factors could be driving the decoupling of house prices and the homeownership rate. From the housing supply side, there is a trend toward decreased construction of starter and mid-size housing units. Developers have increased the construction of large single-family homes at the expense of other segments in the market. This limited supply, particularly for starter homes, could result in increased prices for those homes and fewer new homeowners.”

Continue reading here.

From Federal Reserve Bank of St. Louis:

“Historically, the cost of buying a house has been positively correlated with the percent of households that own their home. During 1996 to 2006 in the United States, both the price of houses and the homeownership rate increased. This increasing trend ended abruptly with the global financial crisis, which saw house prices plunge and drove homeownership rates to historically low levels.

Posted by at 5:00 AM

Labels: Global Housing Watch

Subscribe to: Posts