Showing posts with label Global Housing Watch. Show all posts

Wednesday, February 7, 2018

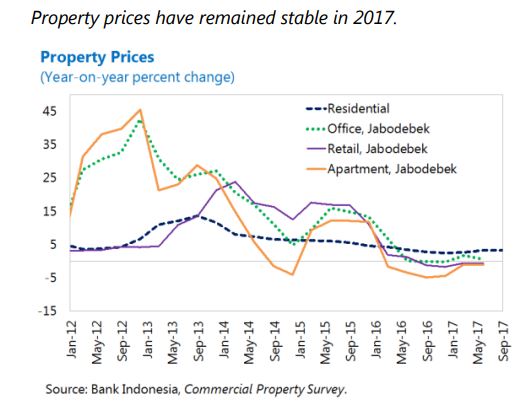

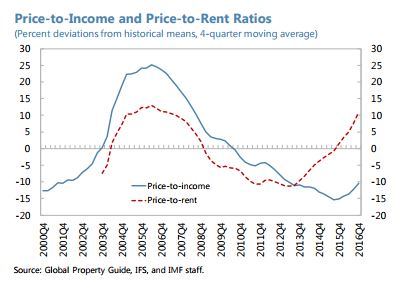

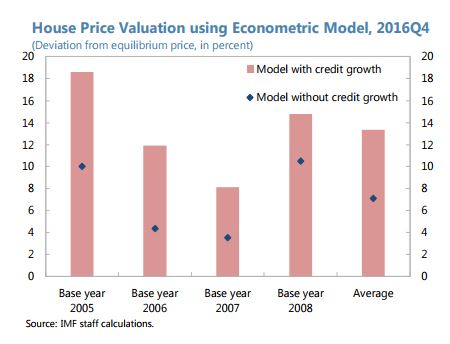

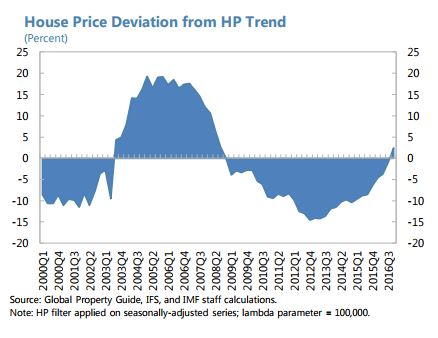

House Prices in Indonesia

From the IMF’s latest report on Indonesia:

Posted by at 10:23 AM

Labels: Global Housing Watch

Friday, February 2, 2018

Country Experiences With Macroprudential Policies

Below is a list of papers put together by the Bank for International Settlements. The list shows the experience of emerging market economies with designing macroprudential frameworks and implementing macroprudential instruments.

- [Brazil] Macroprudential policy in Brazil

- [Chile] Macroeconomic and financial volatility and macroprudential policies in Chile

- [Colombia] The macroprudential policy framework in Colombia

- [Czech Republic] Should monetary policy pay attention to house prices? The Czech National Bank’s approach

- [Hong Kong] Hong Kong’s property market and macroprudential measures

- [Hungary] Regionally-differentiated debt cap rules: a Hungarian perspective

- [India] Macroprudential frameworks, implementation, and relationship with other policies

- [Indonesia] Indonesia: the macroprudential framework and the central bank’s policy mix

- [Israel] Assessing the impact of macroprudential tools: the case of Israel

- [Korea] Macroprudential frameworks, implementation and relationship with other policies in Korea

- [Malaysia] Macroprudential frameworks: Implementation, and relationship with other policies – Malaysia

- [Peru] Implementation of macroprudential policy in Peru

- [Philippines] Macroprudential frameworks, implementation, and communication strategies – The Philippines

- [Russia] The macroprudential policy framework in Russia

- [Singapore] Macroprudential policies: A Singapore case study

- [Thailand] Macroprudential framework – the case of Thailand

- [Turkey] Financial stability and macroprudential policy in Turkey

Below is a list of papers put together by the Bank for International Settlements. The list shows the experience of emerging market economies with designing macroprudential frameworks and implementing macroprudential instruments.

Posted by at 10:02 AM

Labels: Global Housing Watch

Housing View – February 2, 2018

On cross-country:

- Friend or Foe? Cross-Border Linkages, Contagious Banking Crises, and “Coordinated” Macroprudential Policies – IMF

- Quarterly Review of European Mortgage Markets – European Mortgage Federation

- More Mortgages, More Homes? The Effect of Housing Financialization on Homeownership in Historical Perspective – Sage Journals

On the US:

- Mayors Take the Fight for Affordable Housing to Capitol Hill – Citylab, Seattle Times

- Eliminating the mortgage tax deduction could boost homeownership – Marginal Revolution

- National Mortgage Risk Index (NMRI) and Other Risk Measures – American Enterprise Institute

- Rent Control: A Reckoning – Citylab

- My 10-Year Odyssey Through America’s Housing Crisis – Wall Street Journal

- Real House Prices and Price-to-Rent Ratio in November – Calculated Risk

- Can Small Housing Units Help Meet the Need for Affordable Housing in New York City? – NYU Furman Center

- Infrastructure Plans Should Invest in Affordable Housing – Center on Budget and Policy Priorities

On other countries:

- [Canada] Canada’s housing markets remain highly vulnerable overall – Canada Mortgage and Housing Corporation

- [Canada] 5 Predictions for Canada’s Housing Market in 2018 – Dundurn

- [Denmark] Housing Market Analysis for the Capital Region of Denmark: Housing Shortage, Urban Development Potentials, and Strategies – Copenhagen Economics

- [Ireland] Tight property supply constrains Dublin’s Brexit appeal – Financial Times

- [Malta] Housing Market in Malta – IMF

- [Netherlands] Spatial Planning and Segmentation of the Land Market: The Case of the Netherlands – Land Economics

- [Netherlands] Strong correlation between consumption and house prices in the Netherlands – De Nederlandsche Bank

- [New Zealand] Housing Quarterly Report – New Zealand Government

- [United Kingdom] Housing Market Renewal revisited: a defence of place based policy in austere times – Sheffield Hallam University

- [United Kingdom] Sleep tight: can the ‘tiny homes’ movement redefine holidays? – Financial Times

- [United Kingdom] London developers face growing activism over affordable housing – Financial Times

- [United Arab Emirates] Dubai: Survival of the Fittest – REIDIN

- [United Arab Emirates] UAE Residential Market Overview – December Results – REIDIN

Photo by Aliis Sinisalu

On cross-country:

- Friend or Foe? Cross-Border Linkages, Contagious Banking Crises, and “Coordinated” Macroprudential Policies – IMF

- Quarterly Review of European Mortgage Markets – European Mortgage Federation

- More Mortgages, More Homes? The Effect of Housing Financialization on Homeownership in Historical Perspective – Sage Journals

On the US:

- Mayors Take the Fight for Affordable Housing to Capitol Hill – Citylab,

Posted by at 5:00 AM

Labels: Global Housing Watch

Tuesday, January 30, 2018

Housing Market in Malta

From the latest IMF’s report on Malta:

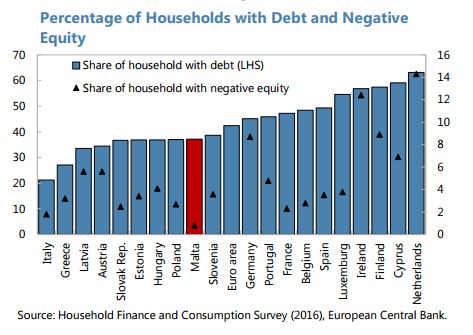

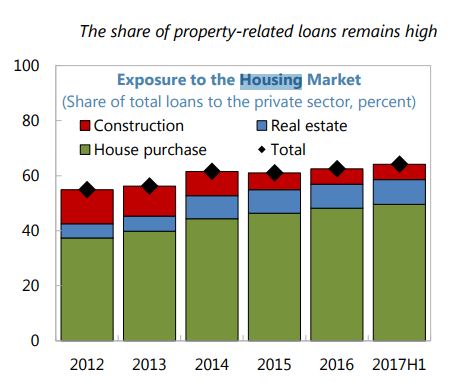

“Strong momentum in the housing market may increase financial stability risks. Household balance sheets are generally sound with a low default rate and financial wealth exceeding peer levels. However, given the high exposure of core domestic banks to property-related loans, a sharp drop in house prices or increases in interest rates may lead to a negative spiral of low lending and investment and adverse macro-financial repercussions. Future unwinding of real estate investments by successful IIP applicants may also put downward pressure on housing prices. While staff does not see immediate financial stability risks, persistent strength in mortgage lending and sustained demand for properties without a corresponding increase in household income could lead to significant imbalances. Staff’s analysis—although subject to uncertainty—indicates that housing prices have entered a modest overvaluation territory by several metrics (…). Moreover, about 80 percent of the respondents to a recent central bank’s survey viewed residential properties as overpriced in 2016.

Steps to pre-empt a potential buildup of risks in the housing market are therefore warranted, including by:

- Deploying targeted macro-prudential limits for mortgages (e.g. limits on loan-to-value and debt service-to-income ratios) to enhance the resilience of bank and household balance sheets to a possible sharp reversal in market conditions. Closing the remaining data gaps on borrower characteristics would help calibrating these measures effectively.

- Ensuring that fiscal incentives do not amplify the housing cycle by aligning the tax rate on rental income with the tax rates on other sources of income. Introducing periodic reviews of the scope and parameters of the IIP, including the minimum real estate investment or leasing values, could help curb housing demand and may improve fiscal revenues’ predictability.

- Repairing corporate balance sheets in the construction sector to increase housing supply.

Accelerated delivery of social housing would mitigate the impact of rising housing prices on the poor. The government has taken measures to increase the availability of social housing units to low-income groups, including by incentivizing private investment through tax exemptions, and provision of financial incentives for the restoration of old properties to be loaned for social housing. Ensuring that eligibility criteria for rent subsidies and social home loans are prudently assessed and means-tested is important.

The authorities regarded property prices as broadly in line with fundamentals, but acknowledged strong demand pressures. They indicated that inflows of foreign workers and tourists are the key demand drivers in the housing market, with acute impact on rents. The reduced tax rate on rental income and the IIP were not viewed as major demand-side factors. The authorities emphasized that risks related to bank exposure to the property market are mitigated by the small fraction of buy-to-rent loans, the diversification of credit risk among many small borrowers, and conservative lending practices, including prudent haircuts on collateral values. However, they agreed that closing further data gaps is necessary, as they are evaluating possible macroprudential policies to mitigate financial stability risks. They intend to publish a White Paper with a view to strengthen the legal framework in the rental market, including through registration of rental contracts. They highlighted that several measures in the 2018 Budget will increase the availability of social housing.”

From the latest IMF’s report on Malta:

“Strong momentum in the housing market may increase financial stability risks. Household balance sheets are generally sound with a low default rate and financial wealth exceeding peer levels. However, given the high exposure of core domestic banks to property-related loans, a sharp drop in house prices or increases in interest rates may lead to a negative spiral of low lending and investment and adverse macro-financial repercussions.

Posted by at 10:35 AM

Labels: Global Housing Watch

Friday, January 26, 2018

Housing View – January 26, 2018

On cross-country:

- 14th Annual Demographia International Housing Affordability Survey: 2018 – Demographia

- Global House Prices Will Rise, but Ideal Conditions to End – FITCH

On the US:

- Redefault Risk in the Aftermath of the Mortgage Crisis: Why Did Modifications Improve More Than Self-Cures? – Federal Reserve Bank of Philadelphia

- Perspectives: Practitioners Weigh in on Drivers of Rising Housing Construction Costs in San Francisco – Terner Center

On other countries:

- [Australia] The changing institutions of private rental housing: an international review – AHURI

- [Belgium] Belgian house prices continue to rise, despite falling demand and weak economy – Global Property Guide

- [Bulgaria] Bulgaria’s house prices rising rapidly, due to strong economic growth – Global Property Guide

- [India] Rent Control in Mumbai – Marginal Revolution

- [Ireland] Update on the progress of the Central Bank of Ireland’s Tracker Mortgage Examination – Central Bank of Ireland

- [Latvia] Latvia’s housing market remains robust – Global Property Guide

- [New Zealand] Quantifying the costs of land use regulation: Evidence from New Zealand – University of Canterbury

- [Portugal] Great value and good yields in Portugal, where house prices continue to rise – Global Property Guide

- [United Kingdom] Empty homes, longer commutes: The unintended consequences of more restrictive local planning – Journal of Public Economics

- [United Kingdom] UK Housing: Something Concrete to Dwell On – Roubini Global Economics

Photo by Aliis Sinisalu

On cross-country:

- 14th Annual Demographia International Housing Affordability Survey: 2018 – Demographia

- Global House Prices Will Rise, but Ideal Conditions to End – FITCH

On the US:

- Redefault Risk in the Aftermath of the Mortgage Crisis: Why Did Modifications Improve More Than Self-Cures? – Federal Reserve Bank of Philadelphia

- Perspectives: Practitioners Weigh in on Drivers of Rising Housing Construction Costs in San Francisco – Terner Center

Posted by at 5:00 AM

Labels: Global Housing Watch

Subscribe to: Posts