Tuesday, January 30, 2018

Housing Market in Malta

From the latest IMF’s report on Malta:

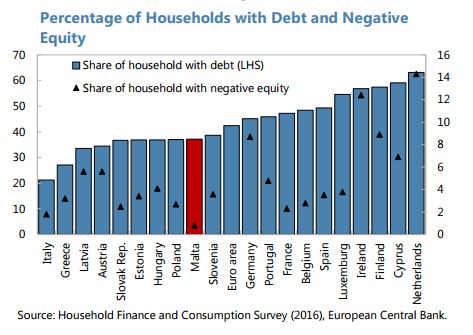

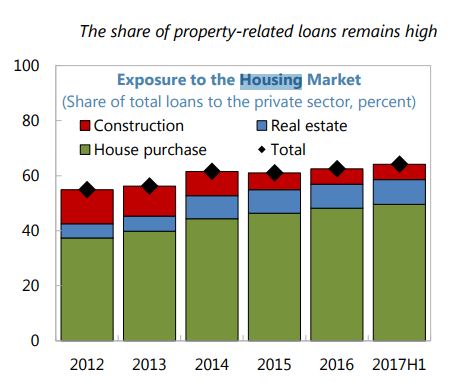

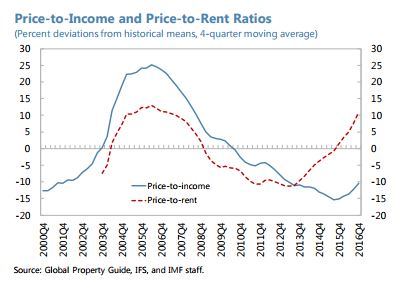

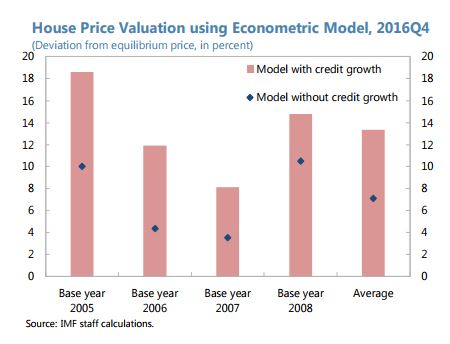

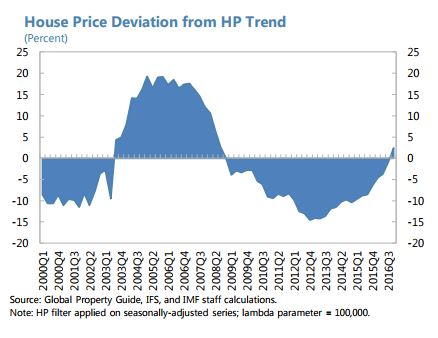

“Strong momentum in the housing market may increase financial stability risks. Household balance sheets are generally sound with a low default rate and financial wealth exceeding peer levels. However, given the high exposure of core domestic banks to property-related loans, a sharp drop in house prices or increases in interest rates may lead to a negative spiral of low lending and investment and adverse macro-financial repercussions. Future unwinding of real estate investments by successful IIP applicants may also put downward pressure on housing prices. While staff does not see immediate financial stability risks, persistent strength in mortgage lending and sustained demand for properties without a corresponding increase in household income could lead to significant imbalances. Staff’s analysis—although subject to uncertainty—indicates that housing prices have entered a modest overvaluation territory by several metrics (…). Moreover, about 80 percent of the respondents to a recent central bank’s survey viewed residential properties as overpriced in 2016.

Steps to pre-empt a potential buildup of risks in the housing market are therefore warranted, including by:

- Deploying targeted macro-prudential limits for mortgages (e.g. limits on loan-to-value and debt service-to-income ratios) to enhance the resilience of bank and household balance sheets to a possible sharp reversal in market conditions. Closing the remaining data gaps on borrower characteristics would help calibrating these measures effectively.

- Ensuring that fiscal incentives do not amplify the housing cycle by aligning the tax rate on rental income with the tax rates on other sources of income. Introducing periodic reviews of the scope and parameters of the IIP, including the minimum real estate investment or leasing values, could help curb housing demand and may improve fiscal revenues’ predictability.

- Repairing corporate balance sheets in the construction sector to increase housing supply.

Accelerated delivery of social housing would mitigate the impact of rising housing prices on the poor. The government has taken measures to increase the availability of social housing units to low-income groups, including by incentivizing private investment through tax exemptions, and provision of financial incentives for the restoration of old properties to be loaned for social housing. Ensuring that eligibility criteria for rent subsidies and social home loans are prudently assessed and means-tested is important.

The authorities regarded property prices as broadly in line with fundamentals, but acknowledged strong demand pressures. They indicated that inflows of foreign workers and tourists are the key demand drivers in the housing market, with acute impact on rents. The reduced tax rate on rental income and the IIP were not viewed as major demand-side factors. The authorities emphasized that risks related to bank exposure to the property market are mitigated by the small fraction of buy-to-rent loans, the diversification of credit risk among many small borrowers, and conservative lending practices, including prudent haircuts on collateral values. However, they agreed that closing further data gaps is necessary, as they are evaluating possible macroprudential policies to mitigate financial stability risks. They intend to publish a White Paper with a view to strengthen the legal framework in the rental market, including through registration of rental contracts. They highlighted that several measures in the 2018 Budget will increase the availability of social housing.”

Posted by at 10:35 AM

Labels: Global Housing Watch

Subscribe to: Posts